Anda mungkin juga menyukai

- Why Are Ratios UsefulDokumen11 halamanWhy Are Ratios UsefulKriza Sevilla Matro100% (3)

- Bindura Nickel 2021Dokumen108 halamanBindura Nickel 2021Arnold MoyoBelum ada peringkat

- Monitoring A BusinessDokumen15 halamanMonitoring A BusinessDenis LordanBelum ada peringkat

- Senior High SchoolDokumen9 halamanSenior High SchoolCharlyn CastroBelum ada peringkat

- Engineering Economics Lect 5Dokumen38 halamanEngineering Economics Lect 5Furqan ChaudhryBelum ada peringkat

- Analysis of Xyz Limited' Company: Liquidity RatiosDokumen7 halamanAnalysis of Xyz Limited' Company: Liquidity RatiosdharmapuriarunBelum ada peringkat

- Finanacial Restructuring 2Dokumen48 halamanFinanacial Restructuring 2Jim Mathilakathu100% (2)

- Current Ratio Analysis of Jai Bhagwati Textile MillsDokumen6 halamanCurrent Ratio Analysis of Jai Bhagwati Textile Millsabhishek27panwalaBelum ada peringkat

- Kodak - Financial AnalysisDokumen5 halamanKodak - Financial Analysismcruz18Belum ada peringkat

- Financial ManagementDokumen6 halamanFinancial ManagementNavinYattiBelum ada peringkat

- Chapter 26 - Analysis of Accounts (EDITED)Dokumen17 halamanChapter 26 - Analysis of Accounts (EDITED)Amour PartekaBelum ada peringkat

- Certain Period, or That They Are Not Getting Payments For Invoices in Fast Enough. A SharpDokumen6 halamanCertain Period, or That They Are Not Getting Payments For Invoices in Fast Enough. A Sharpmalik waseemBelum ada peringkat

- Gemini Electronic Case StudyDokumen9 halamanGemini Electronic Case Studydirshal0% (2)

- Terminal Paper - Financial ManagementDokumen6 halamanTerminal Paper - Financial ManagementhgcisoBelum ada peringkat

- Financial Analysis For Sapphire Fibres LimitedDokumen6 halamanFinancial Analysis For Sapphire Fibres LimitedRashmeen NaeemBelum ada peringkat

- Ratio Analysis of NCLDokumen12 halamanRatio Analysis of NCLAsad KhanBelum ada peringkat

- Two Financial RatiosDokumen9 halamanTwo Financial RatiosWONG ZI QINGBelum ada peringkat

- Evaluate US Tire's Financial Health and Future OutlookDokumen3 halamanEvaluate US Tire's Financial Health and Future OutlookAnna KravcukaBelum ada peringkat

- LONG TERM DEBT RATIOSDokumen4 halamanLONG TERM DEBT RATIOSDiv KabraBelum ada peringkat

- Topical Ratio Analysis For PradaDokumen4 halamanTopical Ratio Analysis For PradaRadBelum ada peringkat

- How the expansion affected D'Leon's sales, profits, working capital and moreDokumen3 halamanHow the expansion affected D'Leon's sales, profits, working capital and moreShaula Tan SombilonBelum ada peringkat

- Ratio and DupontDokumen72 halamanRatio and DupontMohit RathourBelum ada peringkat

- Ratio Analysis: Mari Perolum Company LimitiedDokumen5 halamanRatio Analysis: Mari Perolum Company LimitiedNuman AhmedBelum ada peringkat

- Financial Analysis: Presented by - : Harshit AsawaDokumen10 halamanFinancial Analysis: Presented by - : Harshit Asawaharshit asawaBelum ada peringkat

- Ratio Analysis ExplainedDokumen16 halamanRatio Analysis ExplainedChris LaiBelum ada peringkat

- Analysis of Accounts: NB: The Higher The Percentage, The More Successful The Managers Are in EarningDokumen7 halamanAnalysis of Accounts: NB: The Higher The Percentage, The More Successful The Managers Are in EarningmannBelum ada peringkat

- Auditors Report and Financial Analysis of ITCDokumen28 halamanAuditors Report and Financial Analysis of ITCNeeraj BhartiBelum ada peringkat

- Analysis of Financial Statements: Why Are Ratios Useful?Dokumen26 halamanAnalysis of Financial Statements: Why Are Ratios Useful?MostakBelum ada peringkat

- Chapter 14 - Financial Statement AnalysisDokumen40 halamanChapter 14 - Financial Statement Analysisphamngocmai1912Belum ada peringkat

- Financial Restructuring and Corporate Failure RatiosDokumen48 halamanFinancial Restructuring and Corporate Failure Ratioscalling_nBelum ada peringkat

- Financial Analysis of Martin Manufacturing Company Highlights Key Liquidity, Activity and Profitability RatiosDokumen15 halamanFinancial Analysis of Martin Manufacturing Company Highlights Key Liquidity, Activity and Profitability RatiosdjmondieBelum ada peringkat

- Aqsa Iram FA13 BAF 002Dokumen13 halamanAqsa Iram FA13 BAF 002Aqsa ChBelum ada peringkat

- Liquidity RatiosDokumen39 halamanLiquidity RatiosDaryn GacesBelum ada peringkat

- Module 1 Homework AssignmentDokumen3 halamanModule 1 Homework Assignmentlgarman01Belum ada peringkat

- LESSON 26 - ANALYSIS OF PUBLISHED ACCOUNTS - Note PDFDokumen6 halamanLESSON 26 - ANALYSIS OF PUBLISHED ACCOUNTS - Note PDFFathik FouzanBelum ada peringkat

- Managerial Accounting - Chapter6Dokumen20 halamanManagerial Accounting - Chapter6Nazia AdeelBelum ada peringkat

- Apollo Tyres' Financial Performance Analysis from 2004-2009Dokumen65 halamanApollo Tyres' Financial Performance Analysis from 2004-2009Mitisha GaurBelum ada peringkat

- Key Financial Performance IndicatorsDokumen19 halamanKey Financial Performance Indicatorsmariana.zamudio7aBelum ada peringkat

- Britannia Industries Ltd. (India) Ratio AnalysisDokumen35 halamanBritannia Industries Ltd. (India) Ratio AnalysisMansiShahBelum ada peringkat

- Financial Statement Analysis-IIDokumen45 halamanFinancial Statement Analysis-IINeelisetty Satya SaiBelum ada peringkat

- Management Advisory Services Financial Statement AnalysisDokumen1 halamanManagement Advisory Services Financial Statement AnalysisErica GaytosBelum ada peringkat

- Cash Flow and Ratio AnalysisDokumen7 halamanCash Flow and Ratio AnalysisShalal Bin YousufBelum ada peringkat

- ATHE Financial Management Assignment AnalysisDokumen11 halamanATHE Financial Management Assignment AnalysisEngr AtiqBelum ada peringkat

- Managing finance profit statement ratiosDokumen6 halamanManaging finance profit statement ratiosCarolina Guzman TorresBelum ada peringkat

- Financial RatiosDokumen7 halamanFinancial RatiosarungarBelum ada peringkat

- Ratio Analysis: Theory and ProblemsDokumen51 halamanRatio Analysis: Theory and ProblemsAnit Jacob Philip100% (1)

- Untitled DocumentDokumen4 halamanUntitled DocumentTran Duc Tuan QP2569Belum ada peringkat

- Financial Analysis: Analysis of The Annual Report & AccountsDokumen19 halamanFinancial Analysis: Analysis of The Annual Report & AccountsSrikar NamalaBelum ada peringkat

- Basics of Accounting and Finance: by S.S. BarmaDokumen29 halamanBasics of Accounting and Finance: by S.S. BarmaArya BarmaBelum ada peringkat

- 11 Week of Lectures: Financial Management - MGT201Dokumen19 halaman11 Week of Lectures: Financial Management - MGT201Syed Abdul Mussaver ShahBelum ada peringkat

- Financial Management 1Dokumen4 halamanFinancial Management 1Edith MartinBelum ada peringkat

- Accounting4 2Dokumen16 halamanAccounting4 2Anonymous GDOULL9Belum ada peringkat

- Ratio Analysis of Life Insurance - IBADokumen116 halamanRatio Analysis of Life Insurance - IBANusrat Saragin NovaBelum ada peringkat

- BANK 311 SlidesDokumen18 halamanBANK 311 SlidesMaha AlanjawiBelum ada peringkat

- Shark Loans Financial Statement AnalysisDokumen2 halamanShark Loans Financial Statement AnalysisBai Al-Saraffiah UlamaBelum ada peringkat

- Report On Liquidity Ratios-1Dokumen38 halamanReport On Liquidity Ratios-1Dalia's TechBelum ada peringkat

- Chapter 17Dokumen18 halamanChapter 17sundaravalliBelum ada peringkat

- Financial Accounting - Want to Become Financial Accountant in 30 Days?Dari EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Penilaian: 5 dari 5 bintang5/5 (1)

- RedBullExampleAssessment4Dokumen64 halamanRedBullExampleAssessment4Rahul AhujaBelum ada peringkat

- PRSK4048 Professional Skills Spring 2017: Learning Outcomes AssessedDokumen10 halamanPRSK4048 Professional Skills Spring 2017: Learning Outcomes AssessedRahul AhujaBelum ada peringkat

- Literature Review: INF5261 Kham Viravong - Khamphiv Paulo Fierro - PaulofDokumen14 halamanLiterature Review: INF5261 Kham Viravong - Khamphiv Paulo Fierro - PaulofRahul AhujaBelum ada peringkat

- Language Translator Device Rental Service in Hospitality IndustryDokumen12 halamanLanguage Translator Device Rental Service in Hospitality IndustryRahul AhujaBelum ada peringkat

- Case Study For B301A Tma Apple Apple's Profitable But Risky StrategyDokumen5 halamanCase Study For B301A Tma Apple Apple's Profitable But Risky StrategyRahul AhujaBelum ada peringkat

- Riding School Management ReportDokumen6 halamanRiding School Management ReportRahul AhujaBelum ada peringkat

- The Importance of Critical Reflection in Service-LearningDokumen9 halamanThe Importance of Critical Reflection in Service-LearningLogavani ThamilmaranBelum ada peringkat

- Tutor Marked Assignment (TMA) : InstructionsDokumen2 halamanTutor Marked Assignment (TMA) : InstructionsRahul AhujaBelum ada peringkat

- 3053 en PDFDokumen366 halaman3053 en PDFRahul AhujaBelum ada peringkat

- SIGIRDokumen27 halamanSIGIRRahul AhujaBelum ada peringkat

- 194430's essay on the importance of educationDokumen11 halaman194430's essay on the importance of educationRahul AhujaBelum ada peringkat

- Impact of Recession On Small and Medium Enterprises (Smes) : BUSN20016: Research IN BusinessDokumen18 halamanImpact of Recession On Small and Medium Enterprises (Smes) : BUSN20016: Research IN BusinessRahul AhujaBelum ada peringkat

- AssessmentBrief BusAcc AssessmDokumen4 halamanAssessmentBrief BusAcc AssessmRahul AhujaBelum ada peringkat

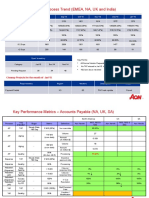

- Vendor Management Process Trend (EMEA, NA, UK and India) : Category Aug'14 Sep'14 Oct'14 Nov'14 Dec'14 Jan'15Dokumen9 halamanVendor Management Process Trend (EMEA, NA, UK and India) : Category Aug'14 Sep'14 Oct'14 Nov'14 Dec'14 Jan'15Rahul AhujaBelum ada peringkat

- Efficient Communication Between A Manager and An Employee As A Way To Sustainable Development of The Contemporary Organisation-Based On Empirical Research Anna Wziątek-StaśkoDokumen7 halamanEfficient Communication Between A Manager and An Employee As A Way To Sustainable Development of The Contemporary Organisation-Based On Empirical Research Anna Wziątek-StaśkoRahul AhujaBelum ada peringkat

- Reading6Dokumen9 halamanReading6Rahul AhujaBelum ada peringkat

- Date Who Received Date Size Subject Asignee Action CommentDokumen44 halamanDate Who Received Date Size Subject Asignee Action CommentRahul AhujaBelum ada peringkat

- 577503Dokumen14 halaman577503Rahul AhujaBelum ada peringkat

- File Time Submitted Submission Id Word Count Character CountDokumen11 halamanFile Time Submitted Submission Id Word Count Character CountRahul AhujaBelum ada peringkat

- 3797 14906 1 PB PDFDokumen7 halaman3797 14906 1 PB PDFRahul AhujaBelum ada peringkat

- BusinessSkillsFinalRESITJul16Dokumen5 halamanBusinessSkillsFinalRESITJul16Rahul AhujaBelum ada peringkat

- Robin RanaDokumen2 halamanRobin RanaRahul AhujaBelum ada peringkat

- Varun Jetley: Career ObjectiveDokumen3 halamanVarun Jetley: Career ObjectiveRahul AhujaBelum ada peringkat

- Consumer Behavior To Fast FoodDokumen9 halamanConsumer Behavior To Fast FoodRahul AhujaBelum ada peringkat

- File Time Submitted Submission Id Word Count Character CountDokumen17 halamanFile Time Submitted Submission Id Word Count Character CountRahul AhujaBelum ada peringkat

- Reflection and Reflective Practice RcogDokumen17 halamanReflection and Reflective Practice RcogRahul AhujaBelum ada peringkat

- Google Pixel Select Stores TnCsDokumen96 halamanGoogle Pixel Select Stores TnCsRahul AhujaBelum ada peringkat

- Confllict and NegotiationDokumen19 halamanConfllict and NegotiationWishnu SeptiyanaBelum ada peringkat

- US AP Team Contact DetailsDokumen25 halamanUS AP Team Contact DetailsRahul AhujaBelum ada peringkat

- Conflict Management & NegotiationDokumen13 halamanConflict Management & NegotiationRahul AhujaBelum ada peringkat

- Assign 2 MKT420 (Aina&ameera)Dokumen18 halamanAssign 2 MKT420 (Aina&ameera)ainaBelum ada peringkat

- Grand PT For APP 004Dokumen20 halamanGrand PT For APP 004Ilumirose Arangcon TamayoBelum ada peringkat

- Impact of Internal Auditors, Audit Committees, and Firm Size on Audit Report LagDokumen9 halamanImpact of Internal Auditors, Audit Committees, and Firm Size on Audit Report LagYohana ElvieraBelum ada peringkat

- Customer Satisfaction Survey Questions For Exide BatteriesDokumen3 halamanCustomer Satisfaction Survey Questions For Exide BatteriesArihant Aski GoswamiBelum ada peringkat

- FBGGBDokumen5 halamanFBGGBPaul Robert DonacaoBelum ada peringkat

- 02 Break Even AnalysisDokumen9 halaman02 Break Even AnalysisMarenightBelum ada peringkat

- Lavigne RoofDokumen7 halamanLavigne Roofusmanf87Belum ada peringkat

- Variable Costing Lecture NotesDokumen2 halamanVariable Costing Lecture NotesCrestu JinBelum ada peringkat

- Turtle Trader Practical SummaryDokumen7 halamanTurtle Trader Practical SummaryGrant Muddle67% (6)

- Denaneso GemechuDokumen86 halamanDenaneso GemechumedrekBelum ada peringkat

- Case Study 06Dokumen4 halamanCase Study 06lieselenaBelum ada peringkat

- CA career profileDokumen2 halamanCA career profilepratikBelum ada peringkat

- SOBHA DEVELOPERS LTD Investor PresentationDokumen29 halamanSOBHA DEVELOPERS LTD Investor PresentationSobha Developers Ltd.Belum ada peringkat

- DUNNING'S OLI PARADIGM AND FDI THEORIESDokumen12 halamanDUNNING'S OLI PARADIGM AND FDI THEORIESankushkumar2000Belum ada peringkat

- Case 1-2 Amazon - Final PresentationDokumen29 halamanCase 1-2 Amazon - Final PresentationBrian SawyerBelum ada peringkat

- Chapter 2 HWDokumen4 halamanChapter 2 HWFarah Nader GoodaBelum ada peringkat

- Indian Money MarketDokumen79 halamanIndian Money MarketParth Shah100% (5)

- Organizational Structure.Dokumen6 halamanOrganizational Structure.Jeannie de leonBelum ada peringkat

- Nature and Scope 1Dokumen1 halamanNature and Scope 1chIBelum ada peringkat

- Amazon Process InnovationDokumen13 halamanAmazon Process InnovationShakti ShikharBelum ada peringkat

- ICAZ Guidance On Code of Ethics and Other Professional Conduct RequiremeDokumen6 halamanICAZ Guidance On Code of Ethics and Other Professional Conduct RequiremePrimrose NgoshiBelum ada peringkat

- Cover FadilDokumen42 halamanCover FadiltitirBelum ada peringkat

- Case Assignment 2Dokumen5 halamanCase Assignment 2Ashish BhanotBelum ada peringkat

- Chapter 6 PDFDokumen28 halamanChapter 6 PDFDiva CarissaBelum ada peringkat

- ASSIGNMENT NO 1 EntrepreneurshipDokumen3 halamanASSIGNMENT NO 1 EntrepreneurshipSyed Hasnain YaseenBelum ada peringkat

- UntitledDokumen10 halamanUntitledRima WahyuBelum ada peringkat

- Sales Forecasting: Sales Forecasting Is The Process of Estimating WhatDokumen13 halamanSales Forecasting: Sales Forecasting Is The Process of Estimating WhatarunangshusenguptaBelum ada peringkat

- Burger King Strategic AnalysisDokumen19 halamanBurger King Strategic AnalysisRamy Mehelba100% (3)

- OIS DiscountingDokumen25 halamanOIS DiscountingAakash Khandelwal100% (1)

- Solution Manual For College Accounting A Contemporary Approach 5th Edition M David Haddock John Price Michael FarinaDokumen2 halamanSolution Manual For College Accounting A Contemporary Approach 5th Edition M David Haddock John Price Michael FarinaLoura Parks100% (30)