Anda mungkin juga menyukai

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (894)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (587)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- Answers To in Text Questions Sloman J 6eDokumen165 halamanAnswers To in Text Questions Sloman J 6eGeorge MSenoir81% (16)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (73)

- UGANDA Voter Count by Polling Stations 2021Dokumen1.446 halamanUGANDA Voter Count by Polling Stations 2021jadwongscribdBelum ada peringkat

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- Elected Members of Parliament 2021Dokumen13 halamanElected Members of Parliament 2021African Centre for Media Excellence100% (2)

- Tumukunde ManifestoDokumen20 halamanTumukunde ManifestoAfrican Centre for Media ExcellenceBelum ada peringkat

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- Macro Formula SheetDokumen3 halamanMacro Formula SheetWin NguyenBelum ada peringkat

- Transcript ExampleDokumen5 halamanTranscript ExampleCardoBelum ada peringkat

- Case Study 5.2Dokumen5 halamanCase Study 5.2Jessa Beloy100% (6)

- Economic Performance Report, June 2021Dokumen39 halamanEconomic Performance Report, June 2021African Centre for Media ExcellenceBelum ada peringkat

- Daily Monitor Sexual Harassment PolicyDokumen11 halamanDaily Monitor Sexual Harassment PolicyAfrican Centre for Media ExcellenceBelum ada peringkat

- National Budget Financial Year 2021/22Dokumen54 halamanNational Budget Financial Year 2021/22GCICBelum ada peringkat

- Rejoinder Statement by Amelia Kyambadde To ParliamentDokumen4 halamanRejoinder Statement by Amelia Kyambadde To ParliamentAfrican Centre for Media ExcellenceBelum ada peringkat

- STATUTORY INSTRUMENTS: The Public Health (Control of COVID - 19) Rules, 2021Dokumen12 halamanSTATUTORY INSTRUMENTS: The Public Health (Control of COVID - 19) Rules, 2021African Centre for Media Excellence100% (1)

- Presidential Election PetitionDokumen14 halamanPresidential Election PetitionAfrican Centre for Media ExcellenceBelum ada peringkat

- Audit Report On COVID - 19 Pandemic Government InterventionsDokumen40 halamanAudit Report On COVID - 19 Pandemic Government InterventionsAfrican Centre for Media ExcellenceBelum ada peringkat

- Vision Group Sexual Harassment PolicyDokumen4 halamanVision Group Sexual Harassment PolicyAfrican Centre for Media ExcellenceBelum ada peringkat

- Constitutional Court Dismisses Suit Challenging Press and Journalists' ActDokumen30 halamanConstitutional Court Dismisses Suit Challenging Press and Journalists' ActAfrican Centre for Media ExcellenceBelum ada peringkat

- National Guidelines For Management of Covid-19Dokumen203 halamanNational Guidelines For Management of Covid-19African Centre for Media ExcellenceBelum ada peringkat

- Report of Budget Committee On Supplementary ExpenditureDokumen33 halamanReport of Budget Committee On Supplementary ExpenditureAfrican Centre for Media ExcellenceBelum ada peringkat

- Performance of The Economy Monthly Report - January 2021Dokumen35 halamanPerformance of The Economy Monthly Report - January 2021African Centre for Media ExcellenceBelum ada peringkat

- Amended Presidential Election PetitionDokumen28 halamanAmended Presidential Election PetitionAfrican Centre for Media ExcellenceBelum ada peringkat

- Statement On Irregularities in Payment of Police ConstablesDokumen4 halamanStatement On Irregularities in Payment of Police ConstablesAfrican Centre for Media ExcellenceBelum ada peringkat

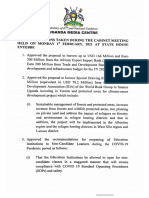

- Cabinet DecisionsDokumen6 halamanCabinet DecisionsAfrican Centre for Media ExcellenceBelum ada peringkat

- Editors Guild CEPIL V AG MC 400 of 2020Dokumen10 halamanEditors Guild CEPIL V AG MC 400 of 2020African Centre for Media ExcellenceBelum ada peringkat

- Absa Africa Financial Market IndexDokumen40 halamanAbsa Africa Financial Market IndexSandraBelum ada peringkat

- Uganda Media Coverage of The 2021 Elections - December 2020Dokumen86 halamanUganda Media Coverage of The 2021 Elections - December 2020African Centre for Media ExcellenceBelum ada peringkat

- Kabuleta Kiiza Joseph ManifestoDokumen27 halamanKabuleta Kiiza Joseph ManifestoAfrican Centre for Media ExcellenceBelum ada peringkat

- Voter Count by District 2021Dokumen4 halamanVoter Count by District 2021African Centre for Media ExcellenceBelum ada peringkat

- NUP ManifestoDokumen47 halamanNUP ManifestoAfrican Centre for Media Excellence100% (1)

- Pastor Fred Mwesigye ManifestoDokumen24 halamanPastor Fred Mwesigye ManifestoAfrican Centre for Media ExcellenceBelum ada peringkat

- Uganda Media Coverage of The 2021 Elections PDFDokumen80 halamanUganda Media Coverage of The 2021 Elections PDFAfrican Centre for Media ExcellenceBelum ada peringkat

- Alliance For National Transformation ManifestoDokumen50 halamanAlliance For National Transformation ManifestoAfrican Centre for Media ExcellenceBelum ada peringkat

- Nancy Linda Kalembe ManifestoDokumen14 halamanNancy Linda Kalembe ManifestoAfrican Centre for Media ExcellenceBelum ada peringkat

- FDC ManifestoDokumen70 halamanFDC ManifestoAfrican Centre for Media ExcellenceBelum ada peringkat

- NRM Manifesto 2021-2026Dokumen288 halamanNRM Manifesto 2021-2026African Centre for Media ExcellenceBelum ada peringkat

- Extra Session Midterm 2023Dokumen13 halamanExtra Session Midterm 2023Yasmine MkBelum ada peringkat

- Solved Suppose That All Social Programs Simultaneously Become More Generous inDokumen1 halamanSolved Suppose That All Social Programs Simultaneously Become More Generous inM Bilal SaleemBelum ada peringkat

- 01A Flow of Economic ActivitiesDokumen11 halaman01A Flow of Economic ActivitiesShrey JoshiBelum ada peringkat

- EconomicsDokumen241 halamanEconomicsSumit Dhall100% (2)

- National Income Sunil Panda SirDokumen30 halamanNational Income Sunil Panda SirAnanya GuptaBelum ada peringkat

- Ch23 - Measuring A Nations IncomeDokumen13 halamanCh23 - Measuring A Nations IncomeMai Anh NguyễnBelum ada peringkat

- Sample For Solution Manual Economics Global Edition by Daron Acemoglu & David LaibsonDokumen14 halamanSample For Solution Manual Economics Global Edition by Daron Acemoglu & David Laibsonavani.goenkaug25Belum ada peringkat

- C Notes: Diagrammatic Derivation of Saving Curve From Consumption CurveDokumen5 halamanC Notes: Diagrammatic Derivation of Saving Curve From Consumption CurveGauravBelum ada peringkat

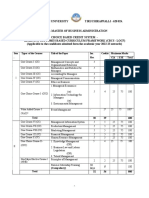

- MBA Syllabus 2022-23Dokumen162 halamanMBA Syllabus 2022-23Trichy MaheshBelum ada peringkat

- The Concept of Equilibrium' in The Goods & Services MarketDokumen3 halamanThe Concept of Equilibrium' in The Goods & Services Marketgosaye desalegnBelum ada peringkat

- Fisher' Equation of ExchangeDokumen5 halamanFisher' Equation of ExchangeDHWANI DEDHIABelum ada peringkat

- Aggregate Supply & Aggregate Demand: Questions To Be AnsweredDokumen12 halamanAggregate Supply & Aggregate Demand: Questions To Be AnswereditvmerivelesBelum ada peringkat

- Vdocument - in - Project Report On Equity Research On Indian Banking SectorDokumen100 halamanVdocument - in - Project Report On Equity Research On Indian Banking SectorNarendran BalarajuBelum ada peringkat

- ECO101 POE - UEH-ISB - 3 2020 - Unit Guide - DR Anh NguyenDokumen11 halamanECO101 POE - UEH-ISB - 3 2020 - Unit Guide - DR Anh NguyenKhanh Ngan PhanBelum ada peringkat

- Hsslive XII Eco Macro ch2 National Income PDFDokumen7 halamanHsslive XII Eco Macro ch2 National Income PDFIRSHAD KIZHISSERIBelum ada peringkat

- Lecture 3 Measurement Model of Productivity 27 FebDokumen33 halamanLecture 3 Measurement Model of Productivity 27 Febbabanianjali100% (1)

- Dovish Vs HawkishDokumen9 halamanDovish Vs Hawkisharti guptaBelum ada peringkat

- Outlook: Asian DevelopmentDokumen301 halamanOutlook: Asian DevelopmentmaharpiciBelum ada peringkat

- BEGP2 OutDokumen28 halamanBEGP2 OutSainadha Reddy PonnapureddyBelum ada peringkat

- History of Econ Thought-9 Pysiocracy-Jaquis TurgotDokumen7 halamanHistory of Econ Thought-9 Pysiocracy-Jaquis TurgotAbiotBelum ada peringkat

- International Trade and the Real Exchange RateDokumen39 halamanInternational Trade and the Real Exchange RateSzabó TamásBelum ada peringkat

- Bretton Woods ConferenceDokumen25 halamanBretton Woods ConferenceNikita MutrejaBelum ada peringkat

- Principles of Macroeconomics: Allama Iqbal Open UniversityDokumen132 halamanPrinciples of Macroeconomics: Allama Iqbal Open UniversityMalik Nouman WarisBelum ada peringkat

- AP Exam Past Exam PaperDokumen3 halamanAP Exam Past Exam PaperAnnaLuxeBelum ada peringkat

- Keynesion Theory of EmploymentDokumen9 halamanKeynesion Theory of EmploymentPoorvi MedatwalBelum ada peringkat

- B. Inggris 2 Uas. Genap 2022Dokumen4 halamanB. Inggris 2 Uas. Genap 2022Tifa latifahBelum ada peringkat