Anda mungkin juga menyukai

- Purchase ConsiderationDokumen5 halamanPurchase ConsiderationAR Ananth Rohith BhatBelum ada peringkat

- OG1 9 Branch AccountingDokumen25 halamanOG1 9 Branch AccountingsridhartksBelum ada peringkat

- Inventory Valuation-ProblemsDokumen3 halamanInventory Valuation-ProblemsKaran100% (1)

- Cost Accounting 9 Edition: Muhammad Shahid Mba (Finance) UOSDokumen16 halamanCost Accounting 9 Edition: Muhammad Shahid Mba (Finance) UOSRahila Rafiq0% (1)

- 08-Rectification-Of-Errors Good OneDokumen54 halaman08-Rectification-Of-Errors Good OneAejaz MohamedBelum ada peringkat

- Cost Accounting Past PapersDokumen66 halamanCost Accounting Past Paperssalamankhana100% (2)

- Labour Costing Practical Questions With Answers: SolutionDokumen7 halamanLabour Costing Practical Questions With Answers: SolutionDeepsak0% (1)

- 3246accounting - CA IPCCDokumen116 halaman3246accounting - CA IPCCPrashant Pandey100% (1)

- 1 Eoq PDFDokumen12 halaman1 Eoq PDFLyber PereiraBelum ada peringkat

- Assignment Questions For Financial StatementsDokumen5 halamanAssignment Questions For Financial StatementsAejaz Mohamed100% (2)

- Job and Batch Costing NotesDokumen5 halamanJob and Batch Costing NotesFarrukhsg100% (1)

- Cost SheetDokumen29 halamanCost Sheetnidhisanjeet0% (1)

- 13 17227rtp Ipcc Nov09 Paper3aDokumen24 halaman13 17227rtp Ipcc Nov09 Paper3aemmanuel JohnyBelum ada peringkat

- Manufacturing Accounts FormatDokumen6 halamanManufacturing Accounts Formatkerwinm6894% (16)

- Chapter - 03 Final Accounts With AdjustmentsDokumen114 halamanChapter - 03 Final Accounts With AdjustmentsAuthor Jyoti Prakash rathBelum ada peringkat

- FA IV As at 23 March 2006Dokumen327 halamanFA IV As at 23 March 2006Daniel Kariuki100% (1)

- 5 Accounting Problems On RoyaltiesDokumen16 halaman5 Accounting Problems On RoyaltiesHakim JanBelum ada peringkat

- Functional BudgetsDokumen12 halamanFunctional Budgetsarjun sachdev100% (1)

- Chapter 4 Overhead ProblemsDokumen5 halamanChapter 4 Overhead Problemsthiluvnddi100% (1)

- Tough LekkaluDokumen42 halamanTough Lekkaludeviprasad03Belum ada peringkat

- Branch AccountsDokumen57 halamanBranch Accountsasadqhse50% (2)

- 4 5931788210203003021Dokumen139 halaman4 5931788210203003021Issa Boy100% (1)

- EOQ With DiscountsDokumen18 halamanEOQ With Discountsprashullp100% (1)

- Cost and Management Accounting Notes and FormulaDokumen84 halamanCost and Management Accounting Notes and FormulaKanchan Chaturvedi74% (47)

- L3-L4 CostsheetDokumen30 halamanL3-L4 CostsheetDhawal RajBelum ada peringkat

- IAS 2 Summary-MergedDokumen19 halamanIAS 2 Summary-MergedShameel IrshadBelum ada peringkat

- Cost Sheet Exercise 1Dokumen3 halamanCost Sheet Exercise 1Phaniraj LenkalapallyBelum ada peringkat

- Pass The Necessary Journal Entries and Post The Entries in The Ledger AccountsDokumen37 halamanPass The Necessary Journal Entries and Post The Entries in The Ledger AccountsBhavya Patel0% (1)

- Ratio Analysis Notes and Practice Questions With SolutionsDokumen23 halamanRatio Analysis Notes and Practice Questions With SolutionsAnkith Poojary67% (6)

- Chapter 9 Accounting For Branches Including Foreign Branches PMDokumen48 halamanChapter 9 Accounting For Branches Including Foreign Branches PMviji88mba60% (5)

- FinAccUnit 3 - Partnership Accounts Lecture Notes PDFDokumen8 halamanFinAccUnit 3 - Partnership Accounts Lecture Notes PDFSherona Reid100% (5)

- Accounting For Single Entry and Incomplete RecordsDokumen18 halamanAccounting For Single Entry and Incomplete RecordsCA Deepak Ehn77% (13)

- Chapter 3 Current Liability PayrollDokumen39 halamanChapter 3 Current Liability PayrollAbdi Mucee Tube100% (1)

- Advanced Financial Accounting - Slides Lecture 21Dokumen16 halamanAdvanced Financial Accounting - Slides Lecture 21DiljanKhanBelum ada peringkat

- Accounting Concepts Case Study and SolutionDokumen8 halamanAccounting Concepts Case Study and SolutionAlok Biswas100% (1)

- MEA AssignmentDokumen13 halamanMEA Assignmentankit07777100% (1)

- Contract CostingDokumen60 halamanContract Costinganon_67206536267% (6)

- Marginal Costing and Decision MakingDokumen31 halamanMarginal Costing and Decision Makingkalaswami100% (1)

- 1st Semester Accounts Selected Question PDFDokumen32 halaman1st Semester Accounts Selected Question PDFVernon Roy100% (1)

- CH 16Dokumen4 halamanCH 16Riya Desai100% (5)

- Ias 2 Questions and AnswersDokumen3 halamanIas 2 Questions and AnswersShameel Irshad75% (8)

- Advanced Worksheet - CH 1Dokumen3 halamanAdvanced Worksheet - CH 1Jichang Hik100% (3)

- Inventory 3-8-2021Dokumen3 halamanInventory 3-8-2021bobBelum ada peringkat

- Company Final Accounts PDFDokumen31 halamanCompany Final Accounts PDFakshay64% (11)

- EPS MCQs PDFDokumen8 halamanEPS MCQs PDFMaria Jawed100% (1)

- Cost Accs Reconciliation Extra SumsDokumen7 halamanCost Accs Reconciliation Extra Sumspurvi doshiBelum ada peringkat

- Chapter 8 Departmental Accounts PDFDokumen22 halamanChapter 8 Departmental Accounts PDFKathem Hadi67% (12)

- Matching QuestionsDokumen9 halamanMatching QuestionsNguyen Thanh Thao (K16 HCM)100% (1)

- Job CostingDokumen18 halamanJob CostingBiswajeet DashBelum ada peringkat

- 7 - Conversion of Single Entry To Double Entry PDFDokumen6 halaman7 - Conversion of Single Entry To Double Entry PDFmiftah fauzi100% (2)

- Royalty AccountsDokumen19 halamanRoyalty Accountsjashveer rekhi100% (2)

- Process Operation CostingDokumen71 halamanProcess Operation CostingMansi IndurkarBelum ada peringkat

- Budgetary ControlDokumen5 halamanBudgetary ControlJasdeep Singh DeepuBelum ada peringkat

- Financial Leverage QuestionsDokumen2 halamanFinancial Leverage QuestionsjeganrajrajBelum ada peringkat

- Home Work Section Working CapitalDokumen10 halamanHome Work Section Working CapitalSaloni AgrawalBelum ada peringkat

- MCQ Questions Set 2 Introduction To AccountingDokumen3 halamanMCQ Questions Set 2 Introduction To AccountingHsiu PingBelum ada peringkat

- Ratio Analysis-1Dokumen4 halamanRatio Analysis-1Aakash RamakrishnanBelum ada peringkat

- NCERT Solutions For Class 11 Accountancy Financial Accounting Part-2 Chapter 1Dokumen41 halamanNCERT Solutions For Class 11 Accountancy Financial Accounting Part-2 Chapter 1Asiya GhaznaviBelum ada peringkat

- Ratio Analysis-1Dokumen3 halamanRatio Analysis-1Ramakrishna J RBelum ada peringkat

- Chapter 4, 5, 6 AssignmentDokumen23 halamanChapter 4, 5, 6 AssignmentSamantha Charlize VizcondeBelum ada peringkat

- Introduction To ICTDokumen89 halamanIntroduction To ICTNelsonMoseMBelum ada peringkat

- Lines and PlanesDokumen16 halamanLines and PlanesNelsonMoseMBelum ada peringkat

- Probability MathsDokumen21 halamanProbability MathsNelsonMoseMBelum ada peringkat

- Binomial DistributionDokumen15 halamanBinomial DistributionNelsonMoseMBelum ada peringkat

- 14 2 PDFDokumen12 halaman14 2 PDFNelsonMoseMBelum ada peringkat

- 16 2 PDFDokumen21 halaman16 2 PDFNelsonMoseM100% (1)

- Integration by Parts: PrerequisitesDokumen9 halamanIntegration by Parts: PrerequisitesNelsonMoseMBelum ada peringkat

- Exact EquationsDokumen11 halamanExact EquationsNelsonMoseMBelum ada peringkat

- Chemistry Physical Chemistry: BiochemistryDokumen5 halamanChemistry Physical Chemistry: BiochemistryNelsonMoseMBelum ada peringkat

- 15 G Form (Pre-Filled)Dokumen3 halaman15 G Form (Pre-Filled)Ravi JammulaBelum ada peringkat

- Semple WoodsDokumen19 halamanSemple WoodsgetakhilsBelum ada peringkat

- Response SummaryDokumen6 halamanResponse SummarySheena MachinjiriBelum ada peringkat

- 01 Place of Supply - GST IDTC - CA. Vishal Poddar - 23-Sep-2020Dokumen58 halaman01 Place of Supply - GST IDTC - CA. Vishal Poddar - 23-Sep-2020TheEnigmatic AccountantBelum ada peringkat

- Waterflow Switch VSR - Potter ElectricDokumen8 halamanWaterflow Switch VSR - Potter ElectricXioBelum ada peringkat

- 07 Quiz 1Dokumen2 halaman07 Quiz 1Von Marvic PonceBelum ada peringkat

- Introduction of Toshiba CorporationDokumen24 halamanIntroduction of Toshiba CorporationPui YanBelum ada peringkat

- Ext Plant For Jto To Sde ExaminationDokumen7 halamanExt Plant For Jto To Sde ExaminationbhagBelum ada peringkat

- CETking MBA CET 2014 Question Paper With Solution PDFDokumen37 halamanCETking MBA CET 2014 Question Paper With Solution PDFmaheeBelum ada peringkat

- Fundamentals of Public Administration - Lecture 12 - NOTEDokumen10 halamanFundamentals of Public Administration - Lecture 12 - NOTEmuntasirulislam42Belum ada peringkat

- Elasticity of DemandDokumen64 halamanElasticity of DemandWadOod KhAn100% (1)

- Transfer Pricing PDFDokumen10 halamanTransfer Pricing PDFFabrienne Kate Eugenio LiberatoBelum ada peringkat

- P1 Robles PDFDokumen80 halamanP1 Robles PDFClarisseBelum ada peringkat

- Motor's Bearing DetailsDokumen9 halamanMotor's Bearing DetailsValipireddy NagarjunBelum ada peringkat

- Rights of Unpaid Seller Against The GoodsDokumen16 halamanRights of Unpaid Seller Against The GoodsDharma TejaBelum ada peringkat

- Planned Maintenance Manual: GEK-75889J SUP. 2, REV. 1Dokumen2 halamanPlanned Maintenance Manual: GEK-75889J SUP. 2, REV. 1ait mimouneBelum ada peringkat

- Math For JU Admision Test PDFDokumen43 halamanMath For JU Admision Test PDFUzma ProthomaBelum ada peringkat

- 1641975023561Dokumen12 halaman1641975023561AbhishekBelum ada peringkat

- Customer Inquiry Report PDFDokumen3 halamanCustomer Inquiry Report PDFbang KinjazzBelum ada peringkat

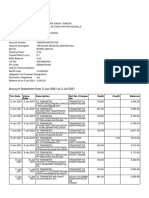

- Account Statement From 3 Jan 2021 To 3 Jul 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDokumen8 halamanAccount Statement From 3 Jan 2021 To 3 Jul 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceSanatan ThakurBelum ada peringkat

- МетодикаDokumen25 halamanМетодикаЮрий ПетровBelum ada peringkat

- 100liter Solar Hitech 5Dokumen2 halaman100liter Solar Hitech 5vicky rBelum ada peringkat

- Chapter - 14 (1) .PDF R.D SharmaDokumen79 halamanChapter - 14 (1) .PDF R.D Sharmaom2390057Belum ada peringkat

- As95234 Reverse Bayonet Connector Catalog PDFDokumen42 halamanAs95234 Reverse Bayonet Connector Catalog PDFdatcuflorinBelum ada peringkat

- Index NumbersDokumen7 halamanIndex NumbersAllauddinaghaBelum ada peringkat

- Analysis of Time SeriesDokumen32 halamanAnalysis of Time SeriesAnika KumarBelum ada peringkat

- Total Qty - 4 Nos Material - UNS F33100 / ASTM A536 65-45-12Dokumen1 halamanTotal Qty - 4 Nos Material - UNS F33100 / ASTM A536 65-45-12sudipta dasBelum ada peringkat

- Salva Vs Magpile 844 SCRA 586Dokumen13 halamanSalva Vs Magpile 844 SCRA 586Jay Telan IIBelum ada peringkat

- Topic 8 AsphaltDokumen20 halamanTopic 8 Asphaltvirkaalam02Belum ada peringkat

- Sheet Metal Products 3940Dokumen298 halamanSheet Metal Products 3940maxisinc.in100% (1)