Anda mungkin juga menyukai

- Exercise 1: On December 31, Bryniuk's Company, The Accounting Records Showed The Following InformationDokumen10 halamanExercise 1: On December 31, Bryniuk's Company, The Accounting Records Showed The Following InformationJohn Kenneth Bohol50% (2)

- Accounts ReceivableDokumen11 halamanAccounts Receivablesarahbee89% (9)

- Financial StatementsDokumen4 halamanFinancial StatementsBobby VisitacionBelum ada peringkat

- PAS 1 With Notes - Pres of FS PDFDokumen75 halamanPAS 1 With Notes - Pres of FS PDFFatima Ann GuevarraBelum ada peringkat

- Accounting Standards ProjectDokumen6 halamanAccounting Standards ProjectPuneet ChawlaBelum ada peringkat

- AFARrDokumen989 halamanAFARrIvhy Cruz Estrella100% (1)

- ILM Leadership SkillsDokumen22 halamanILM Leadership Skillsektasharma123Belum ada peringkat

- Solution of Finanical Statement AnalysisDokumen14 halamanSolution of Finanical Statement AnalysisMUHAMMAD AZAM100% (2)

- Expo NG Stan Tion of Osure D Ndard (A Financ Draft AS) 1 (Cial Sta (Revise Atement D) TsDokumen26 halamanExpo NG Stan Tion of Osure D Ndard (A Financ Draft AS) 1 (Cial Sta (Revise Atement D) TsratiBelum ada peringkat

- IAS Standards IAS 1 Presentation of Financial StatementsDokumen23 halamanIAS Standards IAS 1 Presentation of Financial StatementsmulualemBelum ada peringkat

- Indian Accounting Standards (Abbreviated As Ind-AS) in India Accounting StandardsDokumen6 halamanIndian Accounting Standards (Abbreviated As Ind-AS) in India Accounting Standardsmba departmentBelum ada peringkat

- Notes To Interim Finacial StatementsDokumen7 halamanNotes To Interim Finacial StatementsJhoanna Marie Manuel-AbelBelum ada peringkat

- Fa 534Dokumen11 halamanFa 534Sonia MakwanaBelum ada peringkat

- Mawlana Bhashani Science and Technology University: Course Title: Accounting Theory Course Code: AIS 421Dokumen33 halamanMawlana Bhashani Science and Technology University: Course Title: Accounting Theory Course Code: AIS 421rakibul islamBelum ada peringkat

- Financial StatementDokumen7 halamanFinancial StatementEunice SorianoBelum ada peringkat

- International Public Sector Accounting Standards (IPSAS)Dokumen40 halamanInternational Public Sector Accounting Standards (IPSAS)budsy.lambaBelum ada peringkat

- Nestle Project - AccountsDokumen31 halamanNestle Project - AccountsNishant Shah75% (4)

- 6 - IasDokumen25 halaman6 - Iasking brothersBelum ada peringkat

- Recommendations and Conclusion:: Disadvantages-Of-Accounting-Standards-Accounting-Essay - Php#Ixzz3TrnjpbraDokumen9 halamanRecommendations and Conclusion:: Disadvantages-Of-Accounting-Standards-Accounting-Essay - Php#Ixzz3TrnjpbraarpanavsBelum ada peringkat

- Indian and International Accounting StandardsDokumen13 halamanIndian and International Accounting StandardsBhanu PrakashBelum ada peringkat

- A Complete Set of Financial Statements ComprisesDokumen9 halamanA Complete Set of Financial Statements Comprisesۦۦۦۦۦ ۦۦ ۦۦۦBelum ada peringkat

- ACC803 Advanced Financial Reporting: Week 2: Financial Statement Preparation and PresentationDokumen21 halamanACC803 Advanced Financial Reporting: Week 2: Financial Statement Preparation and PresentationRavinesh PrasadBelum ada peringkat

- Accounting Standards 5Dokumen13 halamanAccounting Standards 5prash1820Belum ada peringkat

- Accounting StandardDokumen13 halamanAccounting StandardJohanna Pauline SequeiraBelum ada peringkat

- Accounting Is The Art of Recording Transactions in The Best MannerDokumen22 halamanAccounting Is The Art of Recording Transactions in The Best MannerSunny PandeyBelum ada peringkat

- Accounting Is The Art of Recording Transactions in The Best MannerDokumen22 halamanAccounting Is The Art of Recording Transactions in The Best MannerSunny PandeyBelum ada peringkat

- International Accounting StandardsDokumen10 halamanInternational Accounting Standardsgotambahrani2Belum ada peringkat

- Group 47 Assignment Acc306Dokumen18 halamanGroup 47 Assignment Acc306Nathanael MudohBelum ada peringkat

- Accounting StandardsDokumen24 halamanAccounting Standardslakhan619Belum ada peringkat

- Ac Standard - AS05Dokumen6 halamanAc Standard - AS05api-3705877Belum ada peringkat

- Document 2Dokumen8 halamanDocument 2sohamBelum ada peringkat

- Indian Accounting StandardsDokumen7 halamanIndian Accounting StandardsAnand MakhijaBelum ada peringkat

- Accounting Standards (Satyanath Mohapatra)Dokumen39 halamanAccounting Standards (Satyanath Mohapatra)smrutiranjan swain100% (1)

- Accounting StandardsDokumen10 halamanAccounting Standardschiragmittal286Belum ada peringkat

- Disclosure of Accounting PoliciesDokumen9 halamanDisclosure of Accounting Policieskisser141Belum ada peringkat

- Accounting StandardsDokumen10 halamanAccounting StandardsSakshi JaiswalBelum ada peringkat

- Preparation and Presentation of Financial Statements of IAS 1Dokumen7 halamanPreparation and Presentation of Financial Statements of IAS 1Md AladinBelum ada peringkat

- Presentation of Financial Statements:: International Accounting Standards IAS 1Dokumen19 halamanPresentation of Financial Statements:: International Accounting Standards IAS 1Barif khanBelum ada peringkat

- Accounting Standards 32Dokumen91 halamanAccounting Standards 32bathinisridhar100% (3)

- Accounting StandardsDokumen28 halamanAccounting StandardsIbrahim BashaBelum ada peringkat

- Gaap and AuditDokumen35 halamanGaap and AuditAayushi AroraBelum ada peringkat

- Indian Accounting StandardsDokumen7 halamanIndian Accounting StandardsVishal JoshiBelum ada peringkat

- LkasDokumen19 halamanLkaskavindyatharaki2002Belum ada peringkat

- International Financial Reporting Standards - FinaDokumen13 halamanInternational Financial Reporting Standards - FinanishanthanBelum ada peringkat

- Chapter Two International Public Sector Accounting Standard (Ipsas) Ipsas 1 Presentation of Financial StatementsDokumen21 halamanChapter Two International Public Sector Accounting Standard (Ipsas) Ipsas 1 Presentation of Financial StatementsSara NegashBelum ada peringkat

- Final Accounts: Prof. P. KumaresanDokumen21 halamanFinal Accounts: Prof. P. KumaresanalexanderBelum ada peringkat

- IAS 34 Part 2Dokumen61 halamanIAS 34 Part 2anjali sharmaBelum ada peringkat

- Why We Need of Accounting StandardDokumen5 halamanWhy We Need of Accounting StandardrashidgBelum ada peringkat

- Objective of IAS 1Dokumen10 halamanObjective of IAS 1April IsidroBelum ada peringkat

- Assignment 1 Describe The System of Developing Indian Accounting StandardsDokumen20 halamanAssignment 1 Describe The System of Developing Indian Accounting StandardsShashank100% (1)

- FA Assignment 2 MarkupDokumen2 halamanFA Assignment 2 MarkupKomal RehmanBelum ada peringkat

- Ibtisam MurtazaDokumen4 halamanIbtisam MurtazaMR ABelum ada peringkat

- FA Ind As and IfrsDokumen42 halamanFA Ind As and IfrsFirdoseBelum ada peringkat

- Objective of PAS 1Dokumen7 halamanObjective of PAS 1kristelle0marisseBelum ada peringkat

- AS 5 Net Profit or Loss For The Period, Prior Period Items and Changes in Accounting PoliciesDokumen8 halamanAS 5 Net Profit or Loss For The Period, Prior Period Items and Changes in Accounting PoliciesChandan KumarBelum ada peringkat

- Accounting InformationDokumen9 halamanAccounting InformationAtaulBelum ada peringkat

- 2016 CRP-Question Paper SolvedDokumen17 halaman2016 CRP-Question Paper SolvedKomala0% (1)

- 948 Muhammad Ali HaiderDokumen3 halaman948 Muhammad Ali HaiderMR ABelum ada peringkat

- AfmDokumen15 halamanAfmabcd dcbaBelum ada peringkat

- Engagement Essentials: Preparation, Compilation, and Review of Financial StatementsDari EverandEngagement Essentials: Preparation, Compilation, and Review of Financial StatementsBelum ada peringkat

- Annual Update and Practice Issues for Preparation, Compilation, and Review EngagementsDari EverandAnnual Update and Practice Issues for Preparation, Compilation, and Review EngagementsBelum ada peringkat

- "The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"Dari Everand"The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"Belum ada peringkat

- Audit Risk Alert: General Accounting and Auditing Developments, 2017/18Dari EverandAudit Risk Alert: General Accounting and Auditing Developments, 2017/18Belum ada peringkat

- Audit Risk Alert: Employee Benefit Plans Industry Developments, 2018Dari EverandAudit Risk Alert: Employee Benefit Plans Industry Developments, 2018Belum ada peringkat

- Statement of Cash Flows: Preparation, Presentation, and UseDari EverandStatement of Cash Flows: Preparation, Presentation, and UseBelum ada peringkat

- Reservation 1675238Dokumen1 halamanReservation 1675238EZEKIELBelum ada peringkat

- FinalDokumen104 halamanFinalEZEKIELBelum ada peringkat

- Merged PDFDokumen40 halamanMerged PDFEZEKIELBelum ada peringkat

- Ilovepdf Merged PDFDokumen25 halamanIlovepdf Merged PDFEZEKIELBelum ada peringkat

- Ipsas 27 AgricultureDokumen27 halamanIpsas 27 AgricultureEZEKIELBelum ada peringkat

- Reservation 1183244 PDFDokumen1 halamanReservation 1183244 PDFEZEKIELBelum ada peringkat

- Merged PDFDokumen10 halamanMerged PDFEZEKIELBelum ada peringkat

- Mamic SacerDokumen18 halamanMamic SacerAnonymous 7CxwuBUJz3Belum ada peringkat

- IIIDokumen8 halamanIIIEZEKIELBelum ada peringkat

- Int Finance Nov 2005 ExamDokumen6 halamanInt Finance Nov 2005 ExamEZEKIELBelum ada peringkat

- Ipsas 17 PpeDokumen29 halamanIpsas 17 PpeEZEKIELBelum ada peringkat

- Group KazDokumen16 halamanGroup KazEZEKIELBelum ada peringkat

- Real AssignmentDokumen27 halamanReal AssignmentEZEKIELBelum ada peringkat

- Ipsassummary2012 PDFDokumen30 halamanIpsassummary2012 PDFJean Roselle SiojoBelum ada peringkat

- Q&P Ch7 20080411Dokumen36 halamanQ&P Ch7 20080411EZEKIELBelum ada peringkat

- Foreign Exchange Markets, End of Chapter Solutions.Dokumen27 halamanForeign Exchange Markets, End of Chapter Solutions.PankajatSIBMBelum ada peringkat

- B8 Ipsas - 32 PDFDokumen60 halamanB8 Ipsas - 32 PDFEZEKIELBelum ada peringkat

- ER Ch05 Solution ManualDokumen14 halamanER Ch05 Solution Manualsupering143Belum ada peringkat

- The Foreign Exchange MarketDokumen42 halamanThe Foreign Exchange MarketAtul JainBelum ada peringkat

- Foreign Exchange Market: Spot and Forward FX Markets Are Over-The-Counter Markets DealersDokumen5 halamanForeign Exchange Market: Spot and Forward FX Markets Are Over-The-Counter Markets DealersEZEKIELBelum ada peringkat

- Judy Tax RealDokumen2 halamanJudy Tax RealEZEKIELBelum ada peringkat

- IFRS 10. Consolidated Financial StatementsDokumen7 halamanIFRS 10. Consolidated Financial StatementsEZEKIELBelum ada peringkat

- Account Title Trial Balance: James Khan Distributing Company Worksheet For The Year Ended December 31, 2006Dokumen8 halamanAccount Title Trial Balance: James Khan Distributing Company Worksheet For The Year Ended December 31, 2006Jonathan VidarBelum ada peringkat

- Fabm2 q3 Week1 Module 1 Statement of Financial Position For LrmdsDokumen33 halamanFabm2 q3 Week1 Module 1 Statement of Financial Position For Lrmdstysabell1220Belum ada peringkat

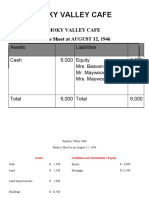

- Smoky Valley CafeDokumen3 halamanSmoky Valley CafeRajkumar KrishnamoorthyBelum ada peringkat

- Worksheet and Closing EntriesDokumen3 halamanWorksheet and Closing EntriesL LiteBelum ada peringkat

- LK Almi 2017 PDFDokumen62 halamanLK Almi 2017 PDFTeguh SetiaBelum ada peringkat

- Luyong - 4TH Q - Fabm1Dokumen3 halamanLuyong - 4TH Q - Fabm1Jonavi LuyongBelum ada peringkat

- Financial Accounting Chapter 9: Accounts Receivable: Classification of ReceivablesDokumen2 halamanFinancial Accounting Chapter 9: Accounts Receivable: Classification of ReceivablesMay Grethel Joy PeranteBelum ada peringkat

- AfarDokumen53 halamanAfarrodell pabloBelum ada peringkat

- Pelabuhan Indonesia III (Persero) Billingual 31 December 2019 Released - pdf-1585646321Dokumen183 halamanPelabuhan Indonesia III (Persero) Billingual 31 December 2019 Released - pdf-1585646321Norival HadiBelum ada peringkat

- Multi Step IncomeDokumen2 halamanMulti Step IncomeRena Rose MalunesBelum ada peringkat

- MYOB Accounting Standard Balance SheetDokumen1 halamanMYOB Accounting Standard Balance SheetMuhammad Choirul ImamBelum ada peringkat

- Accounting Global 9th Edition Horngren Solutions ManualDokumen12 halamanAccounting Global 9th Edition Horngren Solutions Manualmrsamandareynoldsiktzboqwad100% (26)

- Solution Manual Advanced Accounting 11E by Beams 03 Solution Manual Advanced Accounting 11E by Beams 03Dokumen22 halamanSolution Manual Advanced Accounting 11E by Beams 03 Solution Manual Advanced Accounting 11E by Beams 03vvBelum ada peringkat

- Fundamentals of Accountancy, Business and Management: Adjusting Entries (Step 5)Dokumen39 halamanFundamentals of Accountancy, Business and Management: Adjusting Entries (Step 5)Francine Onos GalarpeBelum ada peringkat

- Financial Statements (With Adjustments) : ModuleDokumen17 halamanFinancial Statements (With Adjustments) : ModuleTushar SainiBelum ada peringkat

- Far670 Tutorial Basis of AnalysisDokumen3 halamanFar670 Tutorial Basis of Analysis2020482736Belum ada peringkat

- ch04 Completing The Accounting Cycle - StudentDokumen13 halamanch04 Completing The Accounting Cycle - StudentTâm Vũ NhậtBelum ada peringkat

- Chapter 5 Test BankDokumen12 halamanChapter 5 Test Bankmyngoc181233% (3)

- CH 3 Accounting For Merchandisng BusinessDokumen73 halamanCH 3 Accounting For Merchandisng BusinessYohanna SisayBelum ada peringkat

- Advance Accounting Book 1Dokumen187 halamanAdvance Accounting Book 1Albert Macapagal86% (7)

- LEISURE ON JULY 31STDokumen4 halamanLEISURE ON JULY 31STMaryBelum ada peringkat

- แบบฝึกหัดบทที่1Dokumen3 halamanแบบฝึกหัดบทที่1Rasatja YongskulroteBelum ada peringkat

- IFRS Disclosure Checklist: October 2012Dokumen164 halamanIFRS Disclosure Checklist: October 2012Nizam Uddin MasudBelum ada peringkat

- Intangibe AssetsDokumen4 halamanIntangibe AssetsUNKNOWNNBelum ada peringkat

- PRE BATTERY EXAM 2018 Part 1 FARDokumen11 halamanPRE BATTERY EXAM 2018 Part 1 FARFrl RizalBelum ada peringkat

- Biogen Valuation TemplateDokumen44 halamanBiogen Valuation TemplateYin LukBelum ada peringkat

- Operating Segment Reporting: Essay QuestionsDokumen19 halamanOperating Segment Reporting: Essay QuestionsRainBelum ada peringkat