Anda mungkin juga menyukai

- STANDARD COSTING CALCULATIONSDokumen65 halamanSTANDARD COSTING CALCULATIONSAlbert MuzitiBelum ada peringkat

- Standard Costing 2Dokumen69 halamanStandard Costing 2Jash SanghviBelum ada peringkat

- PDF To DocsDokumen72 halamanPDF To Docs777priyankaBelum ada peringkat

- MCV MPVDokumen8 halamanMCV MPVHarsh MittalBelum ada peringkat

- 7166materials Problems-Standard CostingDokumen14 halaman7166materials Problems-Standard CostingLumina JulieBelum ada peringkat

- Unit 6 Module 10 Standard Costing: Practical ProblemsDokumen14 halamanUnit 6 Module 10 Standard Costing: Practical ProblemsShubham NamdevBelum ada peringkat

- Standard Costing Practical ProblemsDokumen14 halamanStandard Costing Practical ProblemsAlbsBelum ada peringkat

- Unit 6 Module 10 Standard Costing: Practical ProblemsDokumen14 halamanUnit 6 Module 10 Standard Costing: Practical ProblemsyanbladeBelum ada peringkat

- 18-10-SA-V1-S1 Solved Problems SC PDFDokumen14 halaman18-10-SA-V1-S1 Solved Problems SC PDFAlbsBelum ada peringkat

- Standard Costing Practical ProblemsDokumen14 halamanStandard Costing Practical ProblemsDerrick de los ReyesBelum ada peringkat

- Unit 6 Module 10 Standard Costing: Practical ProblemsDokumen14 halamanUnit 6 Module 10 Standard Costing: Practical ProblemsShruti BannerjeeBelum ada peringkat

- Unit 6 Module 10 Standard Costing: Practical ProblemsDokumen14 halamanUnit 6 Module 10 Standard Costing: Practical ProblemsRuchi pariharBelum ada peringkat

- 18 10 SA V1 S1 Solved Problems SC PDFDokumen14 halaman18 10 SA V1 S1 Solved Problems SC PDFTheVagabond HarshalBelum ada peringkat

- Unit 6 Module 10 Standard Costing: Practical ProblemsDokumen14 halamanUnit 6 Module 10 Standard Costing: Practical Problemsyousuf AhmedBelum ada peringkat

- Unit 6 Module 10 Standard Costing: Practical ProblemsDokumen14 halamanUnit 6 Module 10 Standard Costing: Practical ProblemsAfsahBelum ada peringkat

- Standard Costing Practical ProblemsDokumen14 halamanStandard Costing Practical Problemskiran shettyBelum ada peringkat

- Unit 6 Module 10 Standard Costing: Practical ProblemsDokumen14 halamanUnit 6 Module 10 Standard Costing: Practical ProblemsNeelima Varma NadimpalliBelum ada peringkat

- Standard CostingDokumen65 halamanStandard CostingSyed Hussam Haider Tirmazi100% (2)

- Chapter 12 Standard Costing Nov 2020 2Dokumen112 halamanChapter 12 Standard Costing Nov 2020 2Kunal KuvadiaBelum ada peringkat

- Management Accounting and Decision Making: Submitted ByDokumen12 halamanManagement Accounting and Decision Making: Submitted ByKavisha singhBelum ada peringkat

- PROBLEMSChap 7 SMDokumen27 halamanPROBLEMSChap 7 SMVillena Divina VictoriaBelum ada peringkat

- Cost Accountin1ccm 116Dokumen3 halamanCost Accountin1ccm 116gakumoBelum ada peringkat

- Cost II - Ch-5-Mix & Yield VariancesDokumen8 halamanCost II - Ch-5-Mix & Yield VariancesYitera SisayBelum ada peringkat

- Process - Operating CostingDokumen3 halamanProcess - Operating CostingShivansh NahataBelum ada peringkat

- Problem 2 of STD CostingDokumen3 halamanProblem 2 of STD CostingBiswajit BBelum ada peringkat

- CH - 4 Mix and Yield Variance Ahmed FinalDokumen8 halamanCH - 4 Mix and Yield Variance Ahmed FinalYohannes MeridBelum ada peringkat

- Strathmore University study pack on cost and management accountingDokumen3 halamanStrathmore University study pack on cost and management accountinggakumoBelum ada peringkat

- STANDARD COSTING With GP VARIANCE ANALYSIS KEY ANSWERSDokumen19 halamanSTANDARD COSTING With GP VARIANCE ANALYSIS KEY ANSWERSaziel caith florentinBelum ada peringkat

- Standard Costing & Variance AnalysisDokumen19 halamanStandard Costing & Variance AnalysisFUNTV5Belum ada peringkat

- Standard Costing Example SolutionDokumen2 halamanStandard Costing Example SolutionVikas KhuranaBelum ada peringkat

- 400L Standard CostingDokumen8 halaman400L Standard CostingKadeyemo 77Belum ada peringkat

- Hilton MAcc Ch10 SolutionDokumen8 halamanHilton MAcc Ch10 Solutionokquan33% (3)

- Standard CostingDokumen11 halamanStandard CostinganishaBelum ada peringkat

- Fact Pattern: Example 10.5 (Direct Material Cost Variances)Dokumen9 halamanFact Pattern: Example 10.5 (Direct Material Cost Variances)Saiyed KosinBelum ada peringkat

- VariancesDokumen16 halamanVariancesaroridouglas880Belum ada peringkat

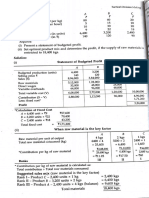

- RAT/AC/2018/F/0008: Budgeted Profit StatementDokumen8 halamanRAT/AC/2018/F/0008: Budgeted Profit StatementumeshBelum ada peringkat

- Variance Analysis CW QuestionsDokumen14 halamanVariance Analysis CW QuestionsMedhaBelum ada peringkat

- Book 1Dokumen12 halamanBook 1Vincent Luigil AlceraBelum ada peringkat

- CH 22 Wiley Kimmel Quiz HomeworkDokumen8 halamanCH 22 Wiley Kimmel Quiz Homeworkmki100% (1)

- Assignment: AnswerDokumen6 halamanAssignment: AnswerumeshBelum ada peringkat

- Standard CostingDokumen16 halamanStandard CostingJash SanghviBelum ada peringkat

- Homework No.12Dokumen6 halamanHomework No.12Danna ClaireBelum ada peringkat

- Activity Cost BehaviorDokumen50 halamanActivity Cost BehavioriqbalrzzBelum ada peringkat

- Standard cost analysis solutionsDokumen4 halamanStandard cost analysis solutionsMohammed Al DhaheriBelum ada peringkat

- Activity Cost BehaviorDokumen49 halamanActivity Cost BehaviorTheresia RumsowekBelum ada peringkat

- Standard costing analysisDokumen8 halamanStandard costing analysisMieanne dela rosaBelum ada peringkat

- 9.1 Solution - Standard CostingDokumen3 halaman9.1 Solution - Standard CostingKendall Anne MendozaBelum ada peringkat

- 2023 Answer CHAPTER 11 PDFDokumen12 halaman2023 Answer CHAPTER 11 PDFRianne NavidadBelum ada peringkat

- Cpa Review School of The Philippines Manila Advanced Financial Accounting and Reporting First Preboard Examination SolutionsDokumen12 halamanCpa Review School of The Philippines Manila Advanced Financial Accounting and Reporting First Preboard Examination SolutionsSophia PerezBelum ada peringkat

- @ProCA - Inter Contract Costing Past Exam QuestionsDokumen10 halaman@ProCA - Inter Contract Costing Past Exam QuestionscallbvipinjainBelum ada peringkat

- Unit 2-3 ADM TYBBADokumen24 halamanUnit 2-3 ADM TYBBAVohra AimanBelum ada peringkat

- SolutionDokumen3 halamanSolutionHilary GaureaBelum ada peringkat

- Suggested Answers Final Examination - Winter 2014: Management AccounitngDokumen5 halamanSuggested Answers Final Examination - Winter 2014: Management AccounitngAbdulAzeemBelum ada peringkat

- Topic 4231Dokumen3 halamanTopic 4231Richard mwanaBelum ada peringkat

- Cost and Management AccountingDokumen7 halamanCost and Management AccountingJoseph PhaustineBelum ada peringkat

- Finalcosting NiyazDokumen29 halamanFinalcosting Niyazakramshaikh87Belum ada peringkat

- 8 Standard CostingDokumen10 halaman8 Standard CostingLakshay SharmaBelum ada peringkat

- Test Material Cost IGPDokumen9 halamanTest Material Cost IGPParth GandhiBelum ada peringkat

- Advanced Opensees Algorithms, Volume 1: Probability Analysis Of High Pier Cable-Stayed Bridge Under Multiple-Support Excitations, And LiquefactionDari EverandAdvanced Opensees Algorithms, Volume 1: Probability Analysis Of High Pier Cable-Stayed Bridge Under Multiple-Support Excitations, And LiquefactionBelum ada peringkat

- How The Credit Card Processing Flow WorksDokumen4 halamanHow The Credit Card Processing Flow Works777priyankaBelum ada peringkat

- 13 June ASDokumen6 halaman13 June AS777priyankaBelum ada peringkat

- Indian Money MarketDokumen7 halamanIndian Money Market777priyankaBelum ada peringkat

- Understanding the Term Structure of Interest RatesDokumen24 halamanUnderstanding the Term Structure of Interest Rates777priyankaBelum ada peringkat

- Meaning of InflationDokumen5 halamanMeaning of Inflation777priyankaBelum ada peringkat

- Mba III Investment Management m6Dokumen3 halamanMba III Investment Management m6777priyankaBelum ada peringkat

- Cheque Introduction: A Cheque Is A Document of Very Great Importance in TheDokumen13 halamanCheque Introduction: A Cheque Is A Document of Very Great Importance in The777priyankaBelum ada peringkat

- Investment FunctionDokumen3 halamanInvestment Function777priyankaBelum ada peringkat

- Risk Aversion and Capital Allocation To Risky AssetsDokumen16 halamanRisk Aversion and Capital Allocation To Risky Assets777priyankaBelum ada peringkat

- The Keynesian Theory of Money and PricesDokumen11 halamanThe Keynesian Theory of Money and Prices777priyankaBelum ada peringkat

- What Is Unemployment?: IndicatorsDokumen9 halamanWhat Is Unemployment?: Indicators777priyankaBelum ada peringkat

- Determinants of InvestmentDokumen4 halamanDeterminants of Investment777priyankaBelum ada peringkat

- Patrícia Meneses & Enric Calvet. Vic. March, The 12thDokumen47 halamanPatrícia Meneses & Enric Calvet. Vic. March, The 12th777priyankaBelum ada peringkat

- Mba III Investment Management m6Dokumen3 halamanMba III Investment Management m6777priyankaBelum ada peringkat

- Principles of Insurance: Presented By: Chaithra.G Chaitra.M. Chandni.K. Devika.B.Z. Niveditha.CDokumen18 halamanPrinciples of Insurance: Presented By: Chaithra.G Chaitra.M. Chandni.K. Devika.B.Z. Niveditha.CaashishBelum ada peringkat

- Banking Business and Financial ServicesDokumen20 halamanBanking Business and Financial ServicesAnuraag SharmaBelum ada peringkat

- Mba III Investment Management m2Dokumen18 halamanMba III Investment Management m2777priyankaBelum ada peringkat

- Micro and MacroDokumen12 halamanMicro and Macro777priyankaBelum ada peringkat

- RM & I Detailed PDFDokumen187 halamanRM & I Detailed PDFDevikaBelum ada peringkat

- Keynesian Theory of Money and PricesDokumen30 halamanKeynesian Theory of Money and Prices777priyankaBelum ada peringkat

- Internationalfinance 120630012630 Phpapp01Dokumen73 halamanInternationalfinance 120630012630 Phpapp01777priyankaBelum ada peringkat

- Introduction To Computerised AccountingDokumen12 halamanIntroduction To Computerised Accountinghajihalvi86% (7)

- Choclate CADBURYDokumen45 halamanChoclate CADBURYanon_131421Belum ada peringkat

- Disciplines Disasters and EM BookDokumen39 halamanDisciplines Disasters and EM BookBones S. MrBonesBelum ada peringkat

- Loss To Agriculture Due To Floods and DroughtDokumen2 halamanLoss To Agriculture Due To Floods and Drought777priyankaBelum ada peringkat

- Role of World Bank in International Business ScenarioDokumen1 halamanRole of World Bank in International Business ScenarioRANOBIR DEY100% (2)

- International Monetary FundDokumen10 halamanInternational Monetary Fund777priyankaBelum ada peringkat

- Euromarkets chp13Dokumen6 halamanEuromarkets chp13bhumidesaiBelum ada peringkat

- International Monetary FundDokumen10 halamanInternational Monetary Fund777priyankaBelum ada peringkat

- Business and Transfer Taxation Test BankDokumen186 halamanBusiness and Transfer Taxation Test Bankprettyboiy19Belum ada peringkat

- MKT 201 NNP RC LemonDokumen22 halamanMKT 201 NNP RC LemonMd. Masud IslamBelum ada peringkat

- PLA Bio-Based Packaging Substitute for CosmeticsDokumen3 halamanPLA Bio-Based Packaging Substitute for Cosmetics赵烨琦Belum ada peringkat

- SwapsDokumen17 halamanSwapsBruno André NunesBelum ada peringkat

- Accounting Fundamentals - Session 6 - For ClassDokumen25 halamanAccounting Fundamentals - Session 6 - For ClassPawani ShuklaBelum ada peringkat

- Adjusting Entries PDFDokumen3 halamanAdjusting Entries PDFreaderBelum ada peringkat

- Integrated Advertising, Promotion, and Marketing CommunicationsDokumen42 halamanIntegrated Advertising, Promotion, and Marketing Communicationswaleed ahmadBelum ada peringkat

- Lingerie IndustryDokumen6 halamanLingerie IndustryGaurav BhaskarBelum ada peringkat

- Taller Uno Acco 112Dokumen44 halamanTaller Uno Acco 112api-274120622Belum ada peringkat

- Group 6 - Principal & Agent RelationshipDokumen9 halamanGroup 6 - Principal & Agent RelationshipwalsondevBelum ada peringkat

- Talent Acquisition Manager ResumeDokumen5 halamanTalent Acquisition Manager Resumegbfcseajd100% (2)

- La Filipina Uy Gongco BODDokumen2 halamanLa Filipina Uy Gongco BODReginaldo BucuBelum ada peringkat

- A Study of Multi Level Marketing Busines-56241751Dokumen8 halamanA Study of Multi Level Marketing Busines-56241751sowyam saleBelum ada peringkat

- Kei Industries LTD SCM StrategyDokumen8 halamanKei Industries LTD SCM StrategyPoorna VinayBelum ada peringkat

- Blanket Requisition ProcessDokumen1 halamanBlanket Requisition ProcessAndrow zulfikar AlBelum ada peringkat

- Mco-06 eDokumen388 halamanMco-06 ekirti dadhichBelum ada peringkat

- FABM 2nd Quarter Exam 41 PtsDokumen6 halamanFABM 2nd Quarter Exam 41 PtsMa Rk100% (3)

- TomsDokumen32 halamanTomsSreten Žujkić PenzionerBelum ada peringkat

- Ch.10 Branch AccountingDokumen30 halamanCh.10 Branch AccountingCA INTERBelum ada peringkat

- Sponsored: Exploring the Emergence of Influencer Marketing on Social MediaDokumen26 halamanSponsored: Exploring the Emergence of Influencer Marketing on Social MediaMiruna MihăilăBelum ada peringkat

- The Multichannel Challenge at Natura in Beauty and Personal CareDokumen14 halamanThe Multichannel Challenge at Natura in Beauty and Personal CareMaría José Chávez Estrada0% (1)

- MJ, J, JL JH LKNDokumen285 halamanMJ, J, JL JH LKNdvgfgfdhBelum ada peringkat

- Strategi Komunikasi Pemasaran Terpadu Mangsi Coffee Dalam Memperkenalkan KopiDokumen6 halamanStrategi Komunikasi Pemasaran Terpadu Mangsi Coffee Dalam Memperkenalkan KopiMade Aristiawan100% (1)

- Operations and Supply Chain Management 15th EditionDokumen13 halamanOperations and Supply Chain Management 15th EditionKimBelum ada peringkat

- Leverage PPTDokumen13 halamanLeverage PPTamdBelum ada peringkat

- SEGMENTATION STRATEGY NestleDokumen3 halamanSEGMENTATION STRATEGY Nestlekamranullah50% (4)

- Job Analysis: X CompanyDokumen5 halamanJob Analysis: X CompanyNovan HanifBelum ada peringkat

- Distinguish Between Capital Expenditure and Revenue ExpenditureDokumen11 halamanDistinguish Between Capital Expenditure and Revenue ExpenditureGopika GopalakrishnanBelum ada peringkat

- Carefully read instructions and answer relevant questionsDokumen3 halamanCarefully read instructions and answer relevant questionsRaymond karikariBelum ada peringkat

- Ferns and Petals: Group - 7 Ankit Ranjan Ghosh Ishita Jain Kshitij Goyal Nilay Ranjan Taru ChaurasiaDokumen9 halamanFerns and Petals: Group - 7 Ankit Ranjan Ghosh Ishita Jain Kshitij Goyal Nilay Ranjan Taru Chaurasiaishita jainBelum ada peringkat