Anda mungkin juga menyukai

- Auditing RacfDokumen57 halamanAuditing Racfசிங்கார வேலன்Belum ada peringkat

- Internal Auditing 03 Framework PDFDokumen4 halamanInternal Auditing 03 Framework PDFEarlkenneth NavarroBelum ada peringkat

- Chart of AccountsDokumen6 halamanChart of Accountssundar kaveetaBelum ada peringkat

- Common Accounting System For PACSDokumen43 halamanCommon Accounting System For PACSanilpanmandBelum ada peringkat

- DBM 2011 Coa Observation RecommendatoinDokumen55 halamanDBM 2011 Coa Observation RecommendatoinAnthony Sutton83% (6)

- Uacs Faqs: Department of Budget and Management Commission On Audit Department of FinanceDokumen7 halamanUacs Faqs: Department of Budget and Management Commission On Audit Department of FinancePhryz PajarilloBelum ada peringkat

- Government Accounting Punzalan SolmanDokumen4 halamanGovernment Accounting Punzalan SolmanAlarich Catayoc100% (1)

- BLGF SRE Manual 2015 PDFDokumen120 halamanBLGF SRE Manual 2015 PDFBench Bayan100% (1)

- AA 4102 1st Hand OutDokumen9 halamanAA 4102 1st Hand OutMana XDBelum ada peringkat

- Treasury and Cash Management - Investment SectionDokumen6 halamanTreasury and Cash Management - Investment Sectionritunath100% (1)

- Project Engineering Change Management ProcedureDokumen17 halamanProject Engineering Change Management Procedurevictorvikram100% (1)

- Efrs Manual Acctg ProcessDokumen57 halamanEfrs Manual Acctg ProcessShobi Dionela100% (2)

- A Comparison Study of Capability Maturity Model and ISO StandardsDokumen74 halamanA Comparison Study of Capability Maturity Model and ISO Standardsapi-3738458Belum ada peringkat

- Government Accounting ReportDokumen48 halamanGovernment Accounting ReportReina Regina S. CamusBelum ada peringkat

- Uganda Implementing An IFMSDokumen6 halamanUganda Implementing An IFMSkhan_sadi100% (1)

- 6s AuditchecklistDokumen7 halaman6s Auditchecklistpremrrs0% (1)

- Feliciano Vs Coa (GR No. 147402 January 14, 2004)Dokumen1 halamanFeliciano Vs Coa (GR No. 147402 January 14, 2004)Joan PabloBelum ada peringkat

- FICCI Course - List of ParticipantsDokumen8 halamanFICCI Course - List of Participantsmano1574Belum ada peringkat

- AutobiographyDokumen2 halamanAutobiographyjulie anne mae mendoza83% (6)

- Ipsas Software ProposalDokumen5 halamanIpsas Software ProposalDahiru MahmudBelum ada peringkat

- Law On Cooperative QuizzerDokumen7 halamanLaw On Cooperative QuizzerDiscord HowBelum ada peringkat

- FAU - InternationalDokumen8 halamanFAU - InternationalShu Xuan ChongBelum ada peringkat

- A. UACS Definition: 1. What Is The UACS?Dokumen28 halamanA. UACS Definition: 1. What Is The UACS?BeomiBelum ada peringkat

- Unified Accounts Code StructureDokumen3 halamanUnified Accounts Code Structurenica leeBelum ada peringkat

- Midterm ForumDokumen5 halamanMidterm ForumRuiz, CherryjaneBelum ada peringkat

- Unified Account Code SystemDokumen5 halamanUnified Account Code SystemHanz paul IguironBelum ada peringkat

- Office Memorandum Subject: Mission Mode Project (Treasury Computerization) Under The National E-Governance Plan (Negp)Dokumen11 halamanOffice Memorandum Subject: Mission Mode Project (Treasury Computerization) Under The National E-Governance Plan (Negp)Information Point KapurthalaBelum ada peringkat

- Unified Accounts Code Structure (UACS)Dokumen4 halamanUnified Accounts Code Structure (UACS)Hammurabi BugtaiBelum ada peringkat

- The Unified Accounts Code StructureDokumen36 halamanThe Unified Accounts Code StructureAzil Jane Protacio GasparBelum ada peringkat

- Basic Features of The New Government Accounting SystemDokumen4 halamanBasic Features of The New Government Accounting SystemabbiecdefgBelum ada peringkat

- Other Financial Management ToolsDokumen4 halamanOther Financial Management ToolsPrudentBelum ada peringkat

- ToR SOE Monitoring Plataform - Final12072021Dokumen6 halamanToR SOE Monitoring Plataform - Final12072021António MarquesBelum ada peringkat

- Comments On Accrual Based Accounting SOPs-Salman SBDokumen2 halamanComments On Accrual Based Accounting SOPs-Salman SBMuhammad EzaanBelum ada peringkat

- Commerce ResponseDokumen8 halamanCommerce ResponseSunlight FoundationBelum ada peringkat

- 16122485Dokumen104 halaman16122485Jacob YeboaBelum ada peringkat

- Chapter 1Dokumen68 halamanChapter 1Merrill Ojeda SaflorBelum ada peringkat

- New Ac 518 Hand OutsDokumen16 halamanNew Ac 518 Hand OutsJieve Licca G. FanoBelum ada peringkat

- Part 1 and Part II of AA 4102 Hand Outs 1Dokumen14 halamanPart 1 and Part II of AA 4102 Hand Outs 1Don Michaelangelo BesabellaBelum ada peringkat

- System To Assist The Goss To Track Aid-Funded Projects and Donor Funds, inDokumen4 halamanSystem To Assist The Goss To Track Aid-Funded Projects and Donor Funds, inmad4anBelum ada peringkat

- If There Is Government Accounting, Why Are Still Their Fraudulent Report?Dokumen3 halamanIf There Is Government Accounting, Why Are Still Their Fraudulent Report?Charlotte PalmaBelum ada peringkat

- 19996ipcc Paper5 App1Dokumen17 halaman19996ipcc Paper5 App1anilBelum ada peringkat

- Central Police Canteen (CPC), Ministry of Home Affairs (Govt of India)Dokumen12 halamanCentral Police Canteen (CPC), Ministry of Home Affairs (Govt of India)jithinrajpkBelum ada peringkat

- Management Information System: Submitted by Presented byDokumen18 halamanManagement Information System: Submitted by Presented byrani222Belum ada peringkat

- (IMF Working Papers) Introducing Financial Management Information Systems in Developing CountriesDokumen25 halaman(IMF Working Papers) Introducing Financial Management Information Systems in Developing Countriesstratmen.sinisa8966Belum ada peringkat

- UACS ManualDokumen41 halamanUACS ManualHammurabi BugtaiBelum ada peringkat

- 3sm Finalnew Accpro-Part1Dokumen18 halaman3sm Finalnew Accpro-Part1B GANAPATHYBelum ada peringkat

- Government Accounting Ch1Dokumen31 halamanGovernment Accounting Ch1John Evan Raymund Besid100% (1)

- Prelim-ExaminationDokumen8 halamanPrelim-Examinationshi shiiisshh100% (1)

- An Introduction An Introduction: Nature and Scope of Accounting For Government and Non-Profit OrganizationsDokumen38 halamanAn Introduction An Introduction: Nature and Scope of Accounting For Government and Non-Profit OrganizationsPhrexilyn PajarilloBelum ada peringkat

- Course Module - Chapter 1 - Overview of Government AccountingDokumen13 halamanCourse Module - Chapter 1 - Overview of Government Accountingssslll2Belum ada peringkat

- Establish and Maintain Cash Based Accounting SystemDokumen31 halamanEstablish and Maintain Cash Based Accounting SystemTegene Tesfaye100% (1)

- Chapter One: Introduction To Federal Government of Ethiopia Accounting and Financial ManagementDokumen61 halamanChapter One: Introduction To Federal Government of Ethiopia Accounting and Financial ManagementGirma100% (4)

- Unit 8 Regulatory Framework of AccountingDokumen16 halamanUnit 8 Regulatory Framework of AccountingerrolbrandfordBelum ada peringkat

- GIFMIS Project BriefDokumen2 halamanGIFMIS Project BriefHammurabi BugtaiBelum ada peringkat

- Aa 4102 Hand Outs Part 1Dokumen12 halamanAa 4102 Hand Outs Part 1Ace Hulsey TevesBelum ada peringkat

- No. 2016-14 August 2016: Not-for-Profit Entities (Topic 958)Dokumen270 halamanNo. 2016-14 August 2016: Not-for-Profit Entities (Topic 958)dinis irikaBelum ada peringkat

- 66487bos53751 Accp 1Dokumen21 halaman66487bos53751 Accp 1Sabareesh KpBelum ada peringkat

- PFMSDokumen5 halamanPFMSShravan Kumar AmanchaBelum ada peringkat

- Philippine: Ublic Inancial AnagementDokumen2 halamanPhilippine: Ublic Inancial AnagementJetmark MarcosBelum ada peringkat

- AC 518 Hand Outs Continuation Disbursements RepairedDokumen17 halamanAC 518 Hand Outs Continuation Disbursements RepairedBenzell Ann BathanBelum ada peringkat

- Accounting Information System in PalestineDokumen11 halamanAccounting Information System in PalestineMohammed AlashiBelum ada peringkat

- Terms of Reference For Sifmis Implementation Quality Assurance Consultant (Firm)Dokumen8 halamanTerms of Reference For Sifmis Implementation Quality Assurance Consultant (Firm)Oshinfowokan OloladeBelum ada peringkat

- Unified Accounts Code StructureDokumen5 halamanUnified Accounts Code StructureCristel TannaganBelum ada peringkat

- Pifra Business Finance ProjectDokumen17 halamanPifra Business Finance ProjectWaqas AhmedBelum ada peringkat

- 5 - Notes On Government AccountingDokumen3 halaman5 - Notes On Government AccountingLabLab Chatto0% (1)

- Psa522 Group 6 - Liyana 2017525427Dokumen32 halamanPsa522 Group 6 - Liyana 2017525427Liyana IzyanBelum ada peringkat

- The Unified Accounts Code Structure: Eulalia V. Ugale, CPA Subject InstructorDokumen47 halamanThe Unified Accounts Code Structure: Eulalia V. Ugale, CPA Subject InstructorMay AugustusBelum ada peringkat

- Unified Accounts Code Structure, Part 1Dokumen24 halamanUnified Accounts Code Structure, Part 1Lala BubBelum ada peringkat

- Financial StatementDokumen22 halamanFinancial StatementHJ ManviBelum ada peringkat

- International Public Sector Accounting Standards Implementation Road Map for UzbekistanDari EverandInternational Public Sector Accounting Standards Implementation Road Map for UzbekistanBelum ada peringkat

- BIR EFPS Quick GuideDokumen2 halamanBIR EFPS Quick Guidejulie anne mae mendozaBelum ada peringkat

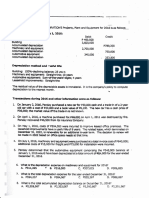

- Y 1H"? J:fr?i"k: p6,135,933 p6,140,433 C. p6,10g, 333Dokumen1 halamanY 1H"? J:fr?i"k: p6,135,933 p6,140,433 C. p6,10g, 333julie anne mae mendozaBelum ada peringkat

- New IAR Key Audit MattersDokumen4 halamanNew IAR Key Audit Mattersjulie anne mae mendozaBelum ada peringkat

- Administrative and Finance Department Accounting DivisionDokumen10 halamanAdministrative and Finance Department Accounting Divisionjulie anne mae mendozaBelum ada peringkat

- Mendoza Written ReportDokumen6 halamanMendoza Written Reportjulie anne mae mendozaBelum ada peringkat

- Audit Rev 1Dokumen1 halamanAudit Rev 1julie anne mae mendozaBelum ada peringkat

- Amunt: Foilows:-FanualyDokumen1 halamanAmunt: Foilows:-Fanualyjulie anne mae mendozaBelum ada peringkat

- Bus - Strat. ReviewerDokumen21 halamanBus - Strat. Reviewerjulie anne mae mendozaBelum ada peringkat

- D. All of The Above Are RequiredDokumen2 halamanD. All of The Above Are Requiredjulie anne mae mendozaBelum ada peringkat

- Ojt DTRDokumen1 halamanOjt DTRjulie anne mae mendozaBelum ada peringkat

- Painting: Ranch Cliffs (Fig 4-12)Dokumen15 halamanPainting: Ranch Cliffs (Fig 4-12)julie anne mae mendoza100% (1)

- Recipe Ham & Cheese Pizza CupcakeDokumen3 halamanRecipe Ham & Cheese Pizza Cupcakejulie anne mae mendozaBelum ada peringkat

- Work SchedDokumen1 halamanWork Schedjulie anne mae mendozaBelum ada peringkat

- SculptureDokumen13 halamanSculpturejulie anne mae mendozaBelum ada peringkat

- Assignment in MathDokumen4 halamanAssignment in Mathjulie anne mae mendozaBelum ada peringkat

- Waiver Form: Signature of Student Over Printed NameDokumen1 halamanWaiver Form: Signature of Student Over Printed Namejulie anne mae mendozaBelum ada peringkat

- Iso 9000Dokumen136 halamanIso 9000BPushevaBelum ada peringkat

- Notice of AGM and EOGMDokumen3 halamanNotice of AGM and EOGMSyed Mujtaba HassanBelum ada peringkat

- Case 06Dokumen4 halamanCase 06Mohammad FaridBelum ada peringkat

- Retail Stores Financial StatementsDokumen29 halamanRetail Stores Financial Statementssribalakarthik_21435Belum ada peringkat

- Jpdf051 Oracle Security Privacy AuditingDokumen2 halamanJpdf051 Oracle Security Privacy AuditingJohn MungaiBelum ada peringkat

- Comprehensive Annual: Mayor Chokwe A. LumumbaDokumen237 halamanComprehensive Annual: Mayor Chokwe A. Lumumbathe kingfishBelum ada peringkat

- P 19 COST & MANAGEMENT AUDIT - Mohit Agarwal Sir PDFDokumen318 halamanP 19 COST & MANAGEMENT AUDIT - Mohit Agarwal Sir PDFray100% (1)

- ACC 213 SylabusDokumen5 halamanACC 213 Sylabusfbicia218Belum ada peringkat

- Assignment On Cadbury Code: Submitted To Submitted byDokumen15 halamanAssignment On Cadbury Code: Submitted To Submitted bytoaha0% (1)

- Chapter 7 Auditing in A Computerize EnvironmentDokumen9 halamanChapter 7 Auditing in A Computerize EnvironmentAngela Miles Dizon100% (1)

- Fundamentals of Assurance Services - Docx'Dokumen8 halamanFundamentals of Assurance Services - Docx'jhell dela cruzBelum ada peringkat

- CAS 510 Initial Audit EngagementsDokumen13 halamanCAS 510 Initial Audit EngagementszelcomeiaukBelum ada peringkat

- NIST CSF 20 Audit Checklist Part 1 - 240429 - 094544Dokumen21 halamanNIST CSF 20 Audit Checklist Part 1 - 240429 - 094544andrewjoriiBelum ada peringkat

- Optimizing The Use of Government AssetsDokumen10 halamanOptimizing The Use of Government AssetsInternational Journal of Innovative Science and Research TechnologyBelum ada peringkat

- Cybersecurity and Data Protection Guideline-2022Dokumen81 halamanCybersecurity and Data Protection Guideline-2022bullshit0976587Belum ada peringkat

- Payroll Sample CVDokumen2 halamanPayroll Sample CVBajrangiBelum ada peringkat

- Internal Audit Report - Education - Secondary SchoolsDokumen16 halamanInternal Audit Report - Education - Secondary SchoolsDanishBelum ada peringkat

- BRSM Form 009 - QMS MDD IsvDokumen16 halamanBRSM Form 009 - QMS MDD IsvAnonymous q8lh3fldWMBelum ada peringkat

- S1194-Audit Report-Modern Precision Engineering FactoryDokumen9 halamanS1194-Audit Report-Modern Precision Engineering FactoryMuhammad IrfanBelum ada peringkat

- Power of The Commissioner To Obtain Information, and To Summon, Examine, and Take Testimony of Persons (Sec. 5)Dokumen6 halamanPower of The Commissioner To Obtain Information, and To Summon, Examine, and Take Testimony of Persons (Sec. 5)ABEGAILE LUCIANOBelum ada peringkat