Anda mungkin juga menyukai

- ING Think Rates Spark Shifting GroundsDokumen6 halamanING Think Rates Spark Shifting GroundsbobmezzBelum ada peringkat

- Towards A Theory of Volatility Trading: Cambridge Books Online © Cambridge University Press, 2010Dokumen19 halamanTowards A Theory of Volatility Trading: Cambridge Books Online © Cambridge University Press, 2010bobmezzBelum ada peringkat

- FX Talking: Some Stark DivergenceDokumen15 halamanFX Talking: Some Stark DivergencebobmezzBelum ada peringkat

- 1 IEOR 4701: Continuous-Time Markov ChainsDokumen22 halaman1 IEOR 4701: Continuous-Time Markov ChainsbobmezzBelum ada peringkat

- c1Dokumen68 halamanc1dey_zicoBelum ada peringkat

- Applied Probability: Nathana El Berestycki, University of Cambridge Part II, Lent 2014Dokumen32 halamanApplied Probability: Nathana El Berestycki, University of Cambridge Part II, Lent 2014bobmezzBelum ada peringkat

- The Convexity Maven: "Building A Better Volatility Mousetrap"Dokumen13 halamanThe Convexity Maven: "Building A Better Volatility Mousetrap"bobmezzBelum ada peringkat

- 4703 07 Notes PP NSPPDokumen9 halaman4703 07 Notes PP NSPPМилан МишићBelum ada peringkat

- Transelliptical Component Analysis: Johns Hopkins University Princeton UniversityDokumen26 halamanTranselliptical Component Analysis: Johns Hopkins University Princeton UniversitybobmezzBelum ada peringkat

- Pca Portfolio SelectionDokumen18 halamanPca Portfolio Selectionluli_kbreraBelum ada peringkat

- 1 Discrete-Time Markov ChainsDokumen7 halaman1 Discrete-Time Markov ChainsbobmezzBelum ada peringkat

- A Tutorial On Principal Component AnalysisDokumen12 halamanA Tutorial On Principal Component AnalysisCristóbal Alberto Campos MuñozBelum ada peringkat

- Learning from interest rate implied volatilitiesDokumen85 halamanLearning from interest rate implied volatilitiesbobmezzBelum ada peringkat

- 1 Communication Classes and Irreducibility For Markov ChainsDokumen8 halaman1 Communication Classes and Irreducibility For Markov ChainsbobmezzBelum ada peringkat

- Statistical Properties of Forward Libor RatesDokumen33 halamanStatistical Properties of Forward Libor RatesbobmezzBelum ada peringkat

- A Tutorial On Principal Component AnalysisDokumen12 halamanA Tutorial On Principal Component AnalysisCristóbal Alberto Campos MuñozBelum ada peringkat

- Global Markets Analyst - Top Ten Market Themes For 2021 - A Shot in The ArmDokumen23 halamanGlobal Markets Analyst - Top Ten Market Themes For 2021 - A Shot in The ArmbobmezzBelum ada peringkat

- GARCH Models in Python 1Dokumen31 halamanGARCH Models in Python 1visBelum ada peringkat

- Siegel ParadoxDokumen4 halamanSiegel ParadoxbobmezzBelum ada peringkat

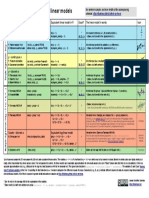

- Common Statistical Tests Are Linear ModelsDokumen1 halamanCommon Statistical Tests Are Linear ModelsbobmezzBelum ada peringkat

- Berenberg Global ForecastsDokumen15 halamanBerenberg Global ForecastsbobmezzBelum ada peringkat

- FX Talking: Dovish Fed, Calm Seas - What Could Go Wrong?Dokumen15 halamanFX Talking: Dovish Fed, Calm Seas - What Could Go Wrong?bobmezzBelum ada peringkat

- Measuring cross-gamma riskDokumen16 halamanMeasuring cross-gamma riskbobmezzBelum ada peringkat

- Derivatives Across Asset ClassesDokumen59 halamanDerivatives Across Asset ClassesbobmezzBelum ada peringkat

- Market Volatility BulletinDokumen28 halamanMarket Volatility BulletinbobmezzBelum ada peringkat

- Global Cycle Notes Hope Springs EternalDokumen27 halamanGlobal Cycle Notes Hope Springs EternalbobmezzBelum ada peringkat

- Rate Curves For Forward Euribor Estimation and CSA-Discounting, AmetranoDokumen94 halamanRate Curves For Forward Euribor Estimation and CSA-Discounting, AmetranosindhusrivastavaBelum ada peringkat

- GS Inflation Implementation 10-20Dokumen20 halamanGS Inflation Implementation 10-20bobmezzBelum ada peringkat

- Gatheral 1Dokumen18 halamanGatheral 1Zhenhuan Song100% (1)

- Elices - 2013 - Infoline - The Role of The Model Validation Function To Manage and Mitigate Model RiskDokumen32 halamanElices - 2013 - Infoline - The Role of The Model Validation Function To Manage and Mitigate Model RiskbobmezzBelum ada peringkat

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5784)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (399)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (890)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (587)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (72)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2219)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (119)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- Axioms Convexity Monotonicity and Continuity PDFDokumen68 halamanAxioms Convexity Monotonicity and Continuity PDFMohsin ShabbirBelum ada peringkat

- Cormen Growth of FunctionsDokumen10 halamanCormen Growth of FunctionsNidhiGoel GuptaBelum ada peringkat

- U2 Rational Functions Test Q3Dokumen4 halamanU2 Rational Functions Test Q3Farhan HabibzaiBelum ada peringkat

- HW 3Dokumen3 halamanHW 3Mohammad Naser HashemniaBelum ada peringkat

- Maxima Book Chapter 3Dokumen35 halamanMaxima Book Chapter 3prakush_prakushBelum ada peringkat

- Fractions Worksheet KeyDokumen4 halamanFractions Worksheet KeySimna BijuBelum ada peringkat

- Trig Graphs Worksheet: Unit 4-2Dokumen6 halamanTrig Graphs Worksheet: Unit 4-2catBelum ada peringkat

- Ugmath2022 22may PDFDokumen6 halamanUgmath2022 22may PDFManashree VyasBelum ada peringkat

- 2.3 Linear EquationsDokumen2 halaman2.3 Linear EquationsFaraa BellaBelum ada peringkat

- Geometric Buckling SphericalDokumen2 halamanGeometric Buckling SphericalSyeilendra PramudityaBelum ada peringkat

- Multivariable Calculus Dr. S. K. Gupta Department of Mathematics Indian Institute of Technology, Roorkee Lecture - 08 Differentiability-IIDokumen13 halamanMultivariable Calculus Dr. S. K. Gupta Department of Mathematics Indian Institute of Technology, Roorkee Lecture - 08 Differentiability-IIAnu DasBelum ada peringkat

- MATHEMATICS Summative Assessment Revision Level 1Dokumen2 halamanMATHEMATICS Summative Assessment Revision Level 1Linus Babu DasariBelum ada peringkat

- Sheet (1) - Home Work: Q 8: Determine The Fourier Series Up To and Including The Third Harmonic For The FunctionDokumen5 halamanSheet (1) - Home Work: Q 8: Determine The Fourier Series Up To and Including The Third Harmonic For The FunctionZayn AhmedBelum ada peringkat

- Matlab For Civil EngineerDokumen4 halamanMatlab For Civil EngineerYusuf TrunkwalaBelum ada peringkat

- AnalGeom Activity PDFDokumen11 halamanAnalGeom Activity PDFJozel Bryan Mestiola TerrìbleBelum ada peringkat

- Mariano Marcos State University: College of EngineeringDokumen8 halamanMariano Marcos State University: College of EngineeringLyka Jane Tapia OpeñaBelum ada peringkat

- Solving simultaneous equations worksheetDokumen3 halamanSolving simultaneous equations worksheetZach ChngBelum ada peringkat

- MST326 TMA03 Tutorial SolutionsDokumen11 halamanMST326 TMA03 Tutorial SolutionsllynusBelum ada peringkat

- Euler's Formula and Hyperbolic FunctionsDokumen1 halamanEuler's Formula and Hyperbolic FunctionsbauemmvssBelum ada peringkat

- Computer Numerical Control: TransformationsDokumen56 halamanComputer Numerical Control: TransformationsibraheemBelum ada peringkat

- 2020 - HCI - Promo - QN - No Ans PDFDokumen6 halaman2020 - HCI - Promo - QN - No Ans PDFJohn SmithBelum ada peringkat

- Statika 2Dokumen22 halamanStatika 2Berlinda ElBelum ada peringkat

- Calculus III TowsonDokumen166 halamanCalculus III TowsonCarlos Marques100% (1)

- TRIGONOMETRYDokumen4 halamanTRIGONOMETRYRachel Delosreyes100% (1)

- Chapter 4 Shape FunctionDokumen34 halamanChapter 4 Shape FunctionSunitha SasiBelum ada peringkat

- Inverse Trigonometric Functions MCQDokumen6 halamanInverse Trigonometric Functions MCQAshmita GoyalBelum ada peringkat

- Linear Congruence PDFDokumen1 halamanLinear Congruence PDFdarnok9Belum ada peringkat

- Lesson 3 Understanding Addition of IntegersDokumen5 halamanLesson 3 Understanding Addition of Integersapi-261894355Belum ada peringkat

- Coimbatore - Class XII - Math - Answer Key - I RevDokumen8 halamanCoimbatore - Class XII - Math - Answer Key - I RevShanthi VinodBelum ada peringkat

- New Budget of Work in Mathematics For Grade FiveDokumen8 halamanNew Budget of Work in Mathematics For Grade FiveAnonymous yIlaBBQQBelum ada peringkat