Anda mungkin juga menyukai

- Problems 1-1Dokumen2 halamanProblems 1-1Jane Villanueva71% (7)

- 52955515Dokumen133 halaman52955515mohamedBelum ada peringkat

- Oath of Confidentiality FormDokumen1 halamanOath of Confidentiality FormGodswill Umah OkorieBelum ada peringkat

- Secured Borrowing and A Sale of ReceivablesDokumen1 halamanSecured Borrowing and A Sale of Receivableswarsidi100% (1)

- Debt SettlementDokumen5 halamanDebt SettlementtintypeadherenthplaBelum ada peringkat

- Guide To Par Syndicated LoansDokumen10 halamanGuide To Par Syndicated LoansBagus Deddy AndriBelum ada peringkat

- Safe Guarding Your Future: Financial Literacy How a Trusts Can Shield Your Assets & Reduce TaxesDari EverandSafe Guarding Your Future: Financial Literacy How a Trusts Can Shield Your Assets & Reduce TaxesBelum ada peringkat

- Group Project Breakdown of Debentures & BondsDokumen13 halamanGroup Project Breakdown of Debentures & BondsLakhan KodiyatarBelum ada peringkat

- Chpater 5 - Banking SystemDokumen10 halamanChpater 5 - Banking System21augustBelum ada peringkat

- Debt Instruments: Types, Features & AdvantagesDokumen14 halamanDebt Instruments: Types, Features & AdvantagesAnubhav GoelBelum ada peringkat

- Amer. Surety Co. v. Bethlehem Bank, 314 U.S. 314 (1941)Dokumen9 halamanAmer. Surety Co. v. Bethlehem Bank, 314 U.S. 314 (1941)Scribd Government DocsBelum ada peringkat

- Unenforceable Contract: Everything You Need To KnowDokumen3 halamanUnenforceable Contract: Everything You Need To KnowAnne CervantesBelum ada peringkat

- SuretyDokumen2 halamanSuretyNiño Rey LopezBelum ada peringkat

- Underwriting: Pranav SharmaDokumen23 halamanUnderwriting: Pranav SharmaPranav SharmaBelum ada peringkat

- The Economics of ContractsDokumen172 halamanThe Economics of ContractsXXXBelum ada peringkat

- 2012mar8 - Howard Griswold Conference CallDokumen14 halaman2012mar8 - Howard Griswold Conference CallGemini ResearchBelum ada peringkat

- Business LawDokumen76 halamanBusiness LawJohn MainaBelum ada peringkat

- An Inquiry Into Lies and Liars, and The Pantomimes of LiarsDokumen13 halamanAn Inquiry Into Lies and Liars, and The Pantomimes of LiarsBob Hurt100% (1)

- Investment: Types of InvestmentsDokumen20 halamanInvestment: Types of InvestmentsAtul YadavBelum ada peringkat

- The Uncertainty of True Sale AnalysisDokumen41 halamanThe Uncertainty of True Sale AnalysisHarpott Ghanta0% (1)

- The Ten Commercial Maxims by Jack HarperDokumen10 halamanThe Ten Commercial Maxims by Jack HarpermattheworeillytmBelum ada peringkat

- Nature and Origins of EquityDokumen8 halamanNature and Origins of EquityShabir AhmadBelum ada peringkat

- Promissory Notes - How Negotiability Has Fouled Up The Secondary Mortgage Market, and What To Do About ItDokumen48 halamanPromissory Notes - How Negotiability Has Fouled Up The Secondary Mortgage Market, and What To Do About It83jjmack100% (1)

- Contract EssentialsDokumen17 halamanContract EssentialsTerwabe WapagovskiBelum ada peringkat

- Borrowing Powers of CompanyDokumen37 halamanBorrowing Powers of CompanyRohan NambiarBelum ada peringkat

- Definition of Bonds and DebenturesDokumen3 halamanDefinition of Bonds and Debenturesremruata rascalralteBelum ada peringkat

- Inside Biggest Hedge Fund Dalio 31mar09Dokumen6 halamanInside Biggest Hedge Fund Dalio 31mar09travisandellen100% (1)

- Your Unalienable Rights ExplainedDokumen1 halamanYour Unalienable Rights Explaineda1z403Belum ada peringkat

- Commercial Liens: A Most Potent Weapon: Home Search Guest Book Contact What'S New Disclaimer Source AreaDokumen74 halamanCommercial Liens: A Most Potent Weapon: Home Search Guest Book Contact What'S New Disclaimer Source AreaMicheal Lee100% (1)

- Conyngton, Knapp, Pinkerton - Wills Estates and Trusts, Vol 1 PT I-III (1921, 382 PP)Dokumen382 halamanConyngton, Knapp, Pinkerton - Wills Estates and Trusts, Vol 1 PT I-III (1921, 382 PP)Joshua Daniel-SettlorBelum ada peringkat

- Areas Covered in FPRDokumen4 halamanAreas Covered in FPRNikunj BhatnagarBelum ada peringkat

- Republic Vs DemocracyDokumen4 halamanRepublic Vs DemocracyJustin JinorioBelum ada peringkat

- Bretton Woods Act 1944Dokumen7 halamanBretton Woods Act 1944Theplaymaker508Belum ada peringkat

- Crocker v. Malley, 249 U.S. 223 (1919)Dokumen5 halamanCrocker v. Malley, 249 U.S. 223 (1919)Scribd Government DocsBelum ada peringkat

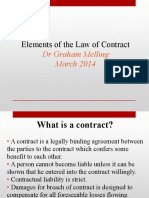

- Elements of The Law of Contract: DR Graham Melling March 2014Dokumen70 halamanElements of The Law of Contract: DR Graham Melling March 2014kks8070Belum ada peringkat

- State Street Trust Company, Executors v. United States, 263 F.2d 635, 1st Cir. (1959)Dokumen10 halamanState Street Trust Company, Executors v. United States, 263 F.2d 635, 1st Cir. (1959)Scribd Government DocsBelum ada peringkat

- MERS Agency (Or Lack Thereof)Dokumen32 halamanMERS Agency (Or Lack Thereof)Tim Bryant100% (7)

- Guide To Estate Planning and WillsDokumen14 halamanGuide To Estate Planning and WillsJessamine LeeBelum ada peringkat

- Law of Trusts CombinationDokumen53 halamanLaw of Trusts Combinationsabiti edwinBelum ada peringkat

- Adverse Selection & Moral HazardDokumen4 halamanAdverse Selection & Moral HazardAJAY KUMAR SAHUBelum ada peringkat

- Hecht v. Malley, 265 U.S. 144 (1924)Dokumen15 halamanHecht v. Malley, 265 U.S. 144 (1924)Scribd Government DocsBelum ada peringkat

- "A Mortgage Loan Is ADokumen14 halaman"A Mortgage Loan Is ASUSHILRRAVAL0% (1)

- Credit River CaseDokumen4 halamanCredit River CaseAngela Wigley100% (1)

- SecuritizationDokumen46 halamanSecuritizationHitesh MoreBelum ada peringkat

- Jed Friedman Bankruptcy Outline-Gerber Fall- ‘06Dokumen106 halamanJed Friedman Bankruptcy Outline-Gerber Fall- ‘06Jed_Friedman_8744100% (1)

- Introduction To Law PDFDokumen24 halamanIntroduction To Law PDFKenny JBelum ada peringkat

- Histroy of BankingDokumen7 halamanHistroy of BankingKiki Longschtrumpf100% (1)

- Bank of America, NT & SA, Petitioner, vs. COURT OF Appeals, Inter-Resin Industrial Corporation, Francisco Trajano, John Doe and Jane DOE, RespondentsDokumen29 halamanBank of America, NT & SA, Petitioner, vs. COURT OF Appeals, Inter-Resin Industrial Corporation, Francisco Trajano, John Doe and Jane DOE, Respondentseasa^belleBelum ada peringkat

- UNIDROIT - Modelclauses-2013Dokumen49 halamanUNIDROIT - Modelclauses-2013luthfi.kBelum ada peringkat

- Law of Property AssignemtDokumen16 halamanLaw of Property AssignemtJaime SmithBelum ada peringkat

- The Story of The Buck Act: Security Number"Dokumen4 halamanThe Story of The Buck Act: Security Number"Bálint Fodor100% (1)

- Escrow Instructions Internet Escrow Services PDFDokumen9 halamanEscrow Instructions Internet Escrow Services PDFByron IniotakisBelum ada peringkat

- The Future of Securitization: Born Free, But Living With More Adult SupervisionDokumen7 halamanThe Future of Securitization: Born Free, But Living With More Adult Supervisionsss1453100% (1)

- InstructionsDokumen3 halamanInstructionsmreagansBelum ada peringkat

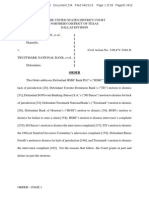

- Order - Bank CaseDokumen28 halamanOrder - Bank CaseAllenStanfordBelum ada peringkat

- Securitization of BanksDokumen31 halamanSecuritization of BanksKumar Deepak100% (1)

- Reining in The Constructive Trust: Darryn JensenDokumen26 halamanReining in The Constructive Trust: Darryn JensenGina CoxBelum ada peringkat

- Privacy ActDokumen62 halamanPrivacy ActMarkMemmottBelum ada peringkat

- Securitization and Structured Finance Post Credit Crunch: A Best Practice Deal Lifecycle GuideDari EverandSecuritization and Structured Finance Post Credit Crunch: A Best Practice Deal Lifecycle GuideBelum ada peringkat

- You Are My Servant and I Have Chosen You: What It Means to Be Called, Chosen, Prepared and Ordained by God for MinistryDari EverandYou Are My Servant and I Have Chosen You: What It Means to Be Called, Chosen, Prepared and Ordained by God for MinistryBelum ada peringkat

- Role of Mortgage Finance Institutions in NigeriaDokumen68 halamanRole of Mortgage Finance Institutions in NigeriaCrystalBelum ada peringkat

- Kotak Mahindra Bank Gets RBI Approval To Open Its First Overseas Branch in Dubai International Financial Centre (Company Update)Dokumen3 halamanKotak Mahindra Bank Gets RBI Approval To Open Its First Overseas Branch in Dubai International Financial Centre (Company Update)Shyam SunderBelum ada peringkat

- Account Statement BY90MTBK30140008000003271543Dokumen1 halamanAccount Statement BY90MTBK30140008000003271543savasdvsdavsadvdBelum ada peringkat

- CHP 11 Discussion Questions HandwriteDokumen2 halamanCHP 11 Discussion Questions HandwriteAnatasyaOktavianiHandriatiTataBelum ada peringkat

- DownloadDokumen4 halamanDownloadSruthi RenganathBelum ada peringkat

- International Bank For Reconstruction and DevelopmentDokumen7 halamanInternational Bank For Reconstruction and DevelopmentbeyyBelum ada peringkat

- PDFDokumen2 halamanPDFp.madhukarreddyBelum ada peringkat

- Indian Banking SectorDokumen18 halamanIndian Banking Sectorapurva JainBelum ada peringkat

- CPS Group - Global Settlement InstructionsDokumen8 halamanCPS Group - Global Settlement InstructionsChris GuarnyBelum ada peringkat

- Disbursal advice loan detailsDokumen2 halamanDisbursal advice loan detailsNaman ModBelum ada peringkat

- No:-1900235370 - Issue Date 24.10.2022: Alliance Broadband Services Pvt. LTDDokumen1 halamanNo:-1900235370 - Issue Date 24.10.2022: Alliance Broadband Services Pvt. LTDSandeep SinghBelum ada peringkat

- Chapter IDokumen83 halamanChapter IAruna TalapatiBelum ada peringkat

- Banking Products and ServicesDokumen5 halamanBanking Products and ServicesAikya GandhiBelum ada peringkat

- Account StatementDokumen5 halamanAccount StatementAabi GujjarBelum ada peringkat

- Quiz 6 Journalizing Without AnswerDokumen8 halamanQuiz 6 Journalizing Without AnswerJazzy MercadoBelum ada peringkat

- Audit of Cash and Marketable SecuritiesDokumen21 halamanAudit of Cash and Marketable Securitiesዝምታ ተሻለBelum ada peringkat

- Three Essays On Macroeconomic Management 2008Dokumen214 halamanThree Essays On Macroeconomic Management 2008Chan RithBelum ada peringkat

- Foreign Currency Accounts ICICI BankDokumen13 halamanForeign Currency Accounts ICICI BankbahlkartikBelum ada peringkat

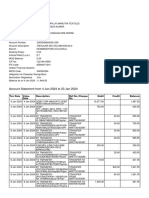

- Account Statement From 4 Jan 2024 To 23 Jan 2024: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDokumen4 halamanAccount Statement From 4 Jan 2024 To 23 Jan 2024: TXN Date Value Date Description Ref No./Cheque No. Debit Credit Balancerangaswamy8194Belum ada peringkat

- B Dam SBI Silchar AC PDFDokumen3 halamanB Dam SBI Silchar AC PDFsanjibannathBelum ada peringkat

- Namma Kalvi Economics Unit 6 Surya Economics Guide emDokumen33 halamanNamma Kalvi Economics Unit 6 Surya Economics Guide emAakaash C.K.Belum ada peringkat

- Banking Law B.com - Docx LatestDokumen38 halamanBanking Law B.com - Docx LatestViraja GuruBelum ada peringkat

- ID Strategi Pemasaran Produk Kredit Perbankan Kasus Bank Nagari Cabang PekanbaruDokumen10 halamanID Strategi Pemasaran Produk Kredit Perbankan Kasus Bank Nagari Cabang Pekanbaru32 yudith trianneBelum ada peringkat

- CHAP - 5 - Lending Policies and Procedures - Managing Credit RiskDokumen56 halamanCHAP - 5 - Lending Policies and Procedures - Managing Credit RiskTran Thanh Ngan0% (1)

- Profile - Dr. Shiva Narayan PHDDokumen3 halamanProfile - Dr. Shiva Narayan PHDDr. Shiva NarayanBelum ada peringkat

- The Monetary SystemDokumen50 halamanThe Monetary SystemRohit GoyalBelum ada peringkat

- Get Shubham Sir's study material on TelegramDokumen14 halamanGet Shubham Sir's study material on TelegramArisha AzharBelum ada peringkat

- Banking Awareness PDFDokumen213 halamanBanking Awareness PDFsrikant ganaluBelum ada peringkat

- Hkex New Entrusted Loan Arrangement 信达国际Dokumen9 halamanHkex New Entrusted Loan Arrangement 信达国际Martin JpBelum ada peringkat