Anda mungkin juga menyukai

- Cred and BudgDokumen26 halamanCred and BudgAndrea SesennaBelum ada peringkat

- WHAT'S F.R.E.E. CREDIT? the personal game changerDari EverandWHAT'S F.R.E.E. CREDIT? the personal game changerPenilaian: 2 dari 5 bintang2/5 (1)

- Guide To Understanding Credit GuideDokumen11 halamanGuide To Understanding Credit GuideRobert Glen Murrell JrBelum ada peringkat

- Comparative Analysis of Home Loans Across Different Banks inDokumen55 halamanComparative Analysis of Home Loans Across Different Banks inAnil MaruBelum ada peringkat

- DIY Credit Repair And Building Guide: Financial Free VictoryDari EverandDIY Credit Repair And Building Guide: Financial Free VictoryBelum ada peringkat

- 8 Get Your Finances & Credit in OrderDokumen15 halaman8 Get Your Finances & Credit in OrdercropdownunderBelum ada peringkat

- Home Loan ProjectDokumen15 halamanHome Loan Projectrashmishetty03Belum ada peringkat

- Boost Your Credit Score In 30 Days: Credit Repair BlueprintDari EverandBoost Your Credit Score In 30 Days: Credit Repair BlueprintBelum ada peringkat

- 5 Mistakes To Avoid When Paying Off Your Mortgage EarlyDokumen10 halaman5 Mistakes To Avoid When Paying Off Your Mortgage EarlyGoKi VoregisBelum ada peringkat

- Easy Guide to Building a Good Credit Score: Personal Finance, #3Dari EverandEasy Guide to Building a Good Credit Score: Personal Finance, #3Belum ada peringkat

- Comparision of BanksDokumen8 halamanComparision of BanksAvani MistryBelum ada peringkat

- Safari - Jun 5, 2019 at 9:49 PMDokumen1 halamanSafari - Jun 5, 2019 at 9:49 PMamir.jahed50Belum ada peringkat

- SODPRMDP-Makaguro Loans (1) (2) (1) - 1Dokumen13 halamanSODPRMDP-Makaguro Loans (1) (2) (1) - 1MaximusBelum ada peringkat

- Inflation & Your Loan - Primer by BankBazaarDokumen12 halamanInflation & Your Loan - Primer by BankBazaarAR HemantBelum ada peringkat

- Think Successfully: The Ultimate Credit Repair GuideDari EverandThink Successfully: The Ultimate Credit Repair GuideBelum ada peringkat

- Credit Card Debt DefinitionDokumen9 halamanCredit Card Debt Definitionako akoBelum ada peringkat

- Financial Fitness Report: Customer NameDokumen11 halamanFinancial Fitness Report: Customer NameDitto NadarBelum ada peringkat

- Name:Rashi Milind Virkud Batch No: S220152Dokumen31 halamanName:Rashi Milind Virkud Batch No: S220152Rashi virkudBelum ada peringkat

- Personal LoansDokumen49 halamanPersonal Loansrohitservi50% (2)

- Credit Mastery For BegginersDokumen16 halamanCredit Mastery For Begginerslubiesplackies009Belum ada peringkat

- Credit Health ReportDokumen13 halamanCredit Health ReportHameed BashaBelum ada peringkat

- Home Loan Procedure: Credit AppraisalDokumen5 halamanHome Loan Procedure: Credit AppraisalShruthi ShettyBelum ada peringkat

- Faqcs PDFDokumen10 halamanFaqcs PDFAnanda VijayasarathyBelum ada peringkat

- Summer Training Project Presentation: Vivek Kumar Gaur MBA-06Dokumen11 halamanSummer Training Project Presentation: Vivek Kumar Gaur MBA-06vivekgaurthestudBelum ada peringkat

- Your Credit Score: What It Means To You As A Prospective Home BuyerDokumen5 halamanYour Credit Score: What It Means To You As A Prospective Home BuyerRyan5Cents100% (2)

- The Subprime & India: PresentersDokumen30 halamanThe Subprime & India: Presentersgauravsurana213065100% (2)

- Study On Credit Appraisal Methods in State Bank of IndiaDokumen5 halamanStudy On Credit Appraisal Methods in State Bank of IndiamuktaBelum ada peringkat

- L1 BankingDokumen38 halamanL1 BankingdjroytatanBelum ada peringkat

- Debt and CreditDokumen19 halamanDebt and CreditMa'am Katrina Marie MirandaBelum ada peringkat

- What Is Credit Appraisal?Dokumen4 halamanWhat Is Credit Appraisal?maniyarasanBelum ada peringkat

- Education Loans For Higher StudiesDokumen7 halamanEducation Loans For Higher StudiesSREYABelum ada peringkat

- UntitledDokumen11 halamanUntitledJust Satisfying ThingsBelum ada peringkat

- CHR Report - 28 August 2023Dokumen12 halamanCHR Report - 28 August 2023Alok G ShindeBelum ada peringkat

- Free Credit Score: How to get your REAL FICO Credit Score for FreeDari EverandFree Credit Score: How to get your REAL FICO Credit Score for FreePenilaian: 4.5 dari 5 bintang4.5/5 (3)

- 101 Powerful Tips For Legally Improving Your Credit ScoreDari Everand101 Powerful Tips For Legally Improving Your Credit ScoreBelum ada peringkat

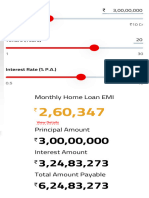

- Home Loan EMI Calculator EMI Calculator CalcuDokumen1 halamanHome Loan EMI Calculator EMI Calculator Calcuarjun rajBelum ada peringkat

- Repair Your Credit Score: The Ultimate Personal Finance Guide. Learn Effective Credit Repair Strategies, Fix Bad Debt and Improve Your Score.Dari EverandRepair Your Credit Score: The Ultimate Personal Finance Guide. Learn Effective Credit Repair Strategies, Fix Bad Debt and Improve Your Score.Belum ada peringkat

- Interest Rates Union Bank of IndiaDokumen1 halamanInterest Rates Union Bank of IndiaNanki SBelum ada peringkat

- Fee Based ManagementDokumen57 halamanFee Based ManagementvahidBelum ada peringkat

- Cibil Score ReportDokumen8 halamanCibil Score ReportrogersBelum ada peringkat

- GK Capsule For Ibps ClerkDokumen16 halamanGK Capsule For Ibps ClerkHitesh MendirattaBelum ada peringkat

- CHR Report - 03 January 2024Dokumen84 halamanCHR Report - 03 January 2024Dev Nayak BkBelum ada peringkat

- Retail BankingDokumen25 halamanRetail BankingTrusha Hodiwala80% (5)

- Evaluating Consumer Loans - 3rd Unit NotesDokumen18 halamanEvaluating Consumer Loans - 3rd Unit NotesDr VIRUPAKSHA GOUD GBelum ada peringkat

- 40 Credit Repair SecretsDokumen8 halaman40 Credit Repair Secretswlingle11753% (19)

- Vulneable GazetteDokumen33 halamanVulneable Gazettecheeramath raryBelum ada peringkat

- DDO Wise List - BF414Dokumen5 halamanDDO Wise List - BF414dineshmarginalBelum ada peringkat

- Leave Rule PDFDokumen37 halamanLeave Rule PDFdineshmarginalBelum ada peringkat

- Gels-2019 - LF Audit-For 78.RVM and 79.SPM Ac'sDokumen5 halamanGels-2019 - LF Audit-For 78.RVM and 79.SPM Ac'sdineshmarginalBelum ada peringkat

- MDG Geh Ngweh .: 78 Rishivandiyam Ac - Supervisor List - 2020-2021Dokumen10 halamanMDG Geh Ngweh .: 78 Rishivandiyam Ac - Supervisor List - 2020-2021dineshmarginal100% (1)

- Expenditure Statement in The Election Section For The Month of 04-2020Dokumen1 halamanExpenditure Statement in The Election Section For The Month of 04-2020dineshmarginalBelum ada peringkat

- Revenue e 267 2021 0Dokumen2 halamanRevenue e 267 2021 0Vishveshwaran SudharshanBelum ada peringkat

- CHOGO Ms 874 PDFDokumen15 halamanCHOGO Ms 874 PDFPreethiBelum ada peringkat

- CJAR PetitionDokumen18 halamanCJAR PetitiondineshmarginalBelum ada peringkat

- RCDokumen1 halamanRCdineshmarginalBelum ada peringkat

- Standard Treatment GuidelineDokumen261 halamanStandard Treatment GuidelineEmaBelum ada peringkat

- Tape PDFDokumen4 halamanTape PDFRed GonzalesBelum ada peringkat

- Introduction STGDokumen2 halamanIntroduction STGdineshmarginalBelum ada peringkat

- 8 ViluppuramDokumen312 halaman8 Viluppuramdineshmarginal100% (2)

- Sempada-Nativity Cert-1!11!16 To 31-01-2017Dokumen6 halamanSempada-Nativity Cert-1!11!16 To 31-01-2017dineshmarginalBelum ada peringkat

- Old CommunityDokumen1 halamanOld CommunitydineshmarginalBelum ada peringkat

- Kolanji EcDokumen7 halamanKolanji EcdineshmarginalBelum ada peringkat

- OnlineecDokumen7 halamanOnlineecNAVIN LADDHABelum ada peringkat

- Tamil Nilam-Patta TransferDokumen2 halamanTamil Nilam-Patta Transferdineshmarginal0% (1)

- OnlineecDokumen7 halamanOnlineecNAVIN LADDHABelum ada peringkat

- OnlineecDokumen7 halamanOnlineecNAVIN LADDHABelum ada peringkat

- Ponpara-Nativity Cert-01!11!16 To 31-01-17Dokumen1 halamanPonpara-Nativity Cert-01!11!16 To 31-01-17dineshmarginalBelum ada peringkat

- Ka - Alamb Nativity Cert-01!11!16 To 31-01-17Dokumen4 halamanKa - Alamb Nativity Cert-01!11!16 To 31-01-17dineshmarginalBelum ada peringkat

- Ka - Alamb Nativity Cert-01!11!16 To 31-01-17Dokumen4 halamanKa - Alamb Nativity Cert-01!11!16 To 31-01-17dineshmarginalBelum ada peringkat

- Tamil Nilam Patta Transfer 2Dokumen1 halamanTamil Nilam Patta Transfer 2dineshmarginalBelum ada peringkat

- Model Village PDFDokumen6 halamanModel Village PDFakshat100% (1)

- Common Guidelines 2008Dokumen57 halamanCommon Guidelines 2008jagadeeshsunkadBelum ada peringkat

- Pds Electricity CertDokumen1 halamanPds Electricity CertdineshmarginalBelum ada peringkat

- Larmore Pol PhilDokumen31 halamanLarmore Pol PhilAnonymous 5aaAT38pZkBelum ada peringkat

- Dengue Guideline DengueDokumen33 halamanDengue Guideline DenguedrkkdbBelum ada peringkat

- Volcano Lesson PlanDokumen5 halamanVolcano Lesson Planapi-294963286Belum ada peringkat

- Retailing PPT (Shailwi Nitish)Dokumen14 halamanRetailing PPT (Shailwi Nitish)vinit PatidarBelum ada peringkat

- Nuttall Gear CatalogDokumen275 halamanNuttall Gear Catalogjose huertasBelum ada peringkat

- Text Extraction From Image: Team Members CH - Suneetha (19mcmb22) Mohit Sharma (19mcmb13)Dokumen20 halamanText Extraction From Image: Team Members CH - Suneetha (19mcmb22) Mohit Sharma (19mcmb13)suneethaBelum ada peringkat

- IEEE 802 StandardsDokumen14 halamanIEEE 802 StandardsHoney RamosBelum ada peringkat

- Necromunda CatalogDokumen35 halamanNecromunda Catalogzafnequin8494100% (1)

- 3 AcmeCorporation Fullstrategicplan 06052015 PDFDokumen11 halaman3 AcmeCorporation Fullstrategicplan 06052015 PDFDina DawoodBelum ada peringkat

- 1 s2.0 S2238785423001345 MainDokumen10 halaman1 s2.0 S2238785423001345 MainHamada Shoukry MohammedBelum ada peringkat

- Small Business and Entrepreneurship ProjectDokumen38 halamanSmall Business and Entrepreneurship ProjectMădălina Elena FotacheBelum ada peringkat

- Alufix Slab Formwork Tim PDFDokumen18 halamanAlufix Slab Formwork Tim PDFMae FalcunitinBelum ada peringkat

- Group 4&5 Activity Syntax AnalyzerDokumen6 halamanGroup 4&5 Activity Syntax AnalyzerJuan PransiskoBelum ada peringkat

- Iit-Jam Mathematics Test: Modern Algebra Time: 60 Minutes Date: 08-10-2017 M.M.: 45Dokumen6 halamanIit-Jam Mathematics Test: Modern Algebra Time: 60 Minutes Date: 08-10-2017 M.M.: 45Lappy TopBelum ada peringkat

- Subject: PSCP (15-10-19) : Syllabus ContentDokumen4 halamanSubject: PSCP (15-10-19) : Syllabus ContentNikunjBhattBelum ada peringkat

- Work Permits New Guideline Amendments 2021 23.11.2021Dokumen7 halamanWork Permits New Guideline Amendments 2021 23.11.2021Sabrina BrathwaiteBelum ada peringkat

- U2 KeyDokumen2 halamanU2 KeyHằng ĐặngBelum ada peringkat

- HYDRAULIC WINCH-MS1059 - Operation & Maintenance Manual Rev ADokumen33 halamanHYDRAULIC WINCH-MS1059 - Operation & Maintenance Manual Rev Azulu80Belum ada peringkat

- Evolution of Campus Switching: Marketing Presentation Marketing PresentationDokumen35 halamanEvolution of Campus Switching: Marketing Presentation Marketing PresentationRosal Mark JovenBelum ada peringkat

- Ep Docx Sca SMSC - V2Dokumen45 halamanEp Docx Sca SMSC - V290007Belum ada peringkat

- Carte EnglezaDokumen112 halamanCarte EnglezageorgianapopaBelum ada peringkat

- History of Old English GrammarDokumen9 halamanHistory of Old English GrammarAla CzerwinskaBelum ada peringkat

- Certificate of Attendance: Yosapat NashulahDokumen2 halamanCertificate of Attendance: Yosapat NashulahStrata WebBelum ada peringkat

- Transformational LeadershipDokumen75 halamanTransformational LeadershipvincentpalaniBelum ada peringkat

- LET-English-Structure of English-ExamDokumen57 halamanLET-English-Structure of English-ExamMarian Paz E Callo80% (5)

- MPPSC ACF Test Paper 8 (26 - 06 - 2022)Dokumen6 halamanMPPSC ACF Test Paper 8 (26 - 06 - 2022)Hari Harul VullangiBelum ada peringkat

- Star Wars Galactic Connexionstm Galactic Beckett Star Wars Story Connexions CallingDokumen4 halamanStar Wars Galactic Connexionstm Galactic Beckett Star Wars Story Connexions CallingJuan TorresBelum ada peringkat

- Operator'S Manual PM20X-X-X-BXX: 2" Diaphragm PumpDokumen12 halamanOperator'S Manual PM20X-X-X-BXX: 2" Diaphragm PumpOmar TadeoBelum ada peringkat

- Patricio Gerpe ResumeDokumen2 halamanPatricio Gerpe ResumeAnonymous 3ID4TBBelum ada peringkat

- Alienation Thesis StatementDokumen8 halamanAlienation Thesis Statementafbteepof100% (2)

- NHL DB Rulebook ENGLISHDokumen6 halamanNHL DB Rulebook ENGLISHAdhika WidyaparagaBelum ada peringkat

- How To Make An Effective PowerPoint PresentationDokumen12 halamanHow To Make An Effective PowerPoint PresentationZach Hansen100% (1)