Anda mungkin juga menyukai

- 1040 Exam Prep: Module I: The Form 1040 FormulaDari Everand1040 Exam Prep: Module I: The Form 1040 FormulaPenilaian: 1 dari 5 bintang1/5 (3)

- Be It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledDokumen5 halamanBe It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledReah CrezzBelum ada peringkat

- Ra 9504 Minimum Wage and Optional Standard DeductionDokumen6 halamanRa 9504 Minimum Wage and Optional Standard Deductionapi-247793055Belum ada peringkat

- Republic Act No 9504Dokumen4 halamanRepublic Act No 9504Brian BaldwinBelum ada peringkat

- Ra 9504Dokumen5 halamanRa 9504MRose SerranoBelum ada peringkat

- Republic Act No. 9504Dokumen4 halamanRepublic Act No. 9504Xyril Ü LlanesBelum ada peringkat

- RA 9504 Amending NIRC Section 34 (L)Dokumen2 halamanRA 9504 Amending NIRC Section 34 (L)RB BalanayBelum ada peringkat

- Be It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledDokumen4 halamanBe It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledHansel Jake B. PampiloBelum ada peringkat

- Be It Enacted by The Senate and House of Representatives of The Philippine Congress AssembledDokumen6 halamanBe It Enacted by The Senate and House of Representatives of The Philippine Congress AssembledAdeline HoodhemwinfordBelum ada peringkat

- Philippines amends income tax rates and capital gains taxDokumen7 halamanPhilippines amends income tax rates and capital gains taxDaniel OngBelum ada peringkat

- Section 5. Section 24 of The NIRC, As Amended, Is Hereby Further Amended To Read As FollowsDokumen3 halamanSection 5. Section 24 of The NIRC, As Amended, Is Hereby Further Amended To Read As FollowsMamerto Egargo Jr.Belum ada peringkat

- Ra 11534Dokumen41 halamanRa 11534Jan Aristhedes AsisBelum ada peringkat

- RA 7497-Amendment On NIRC Relative To The Final Witholding Tax...Dokumen5 halamanRA 7497-Amendment On NIRC Relative To The Final Witholding Tax...Crislene CruzBelum ada peringkat

- CREATE LAWDokumen56 halamanCREATE LAWcall.ppmgyBelum ada peringkat

- R.A. No. 11534 Create LawDokumen42 halamanR.A. No. 11534 Create LawJessa PuerinBelum ada peringkat

- CREATE Bill - Draft Enrolled Copy 02.16.21Dokumen77 halamanCREATE Bill - Draft Enrolled Copy 02.16.21Joshua CustodioBelum ada peringkat

- An Act Reforming The Corporate Income Tax and Incentives SystemDokumen25 halamanAn Act Reforming The Corporate Income Tax and Incentives SystemMhaniell TorrejasBelum ada peringkat

- 2.3 Tax On Income - Tax On IndividualsDokumen14 halaman2.3 Tax On Income - Tax On IndividualsfelixacctBelum ada peringkat

- New Proposals To The TRAIN LawDokumen12 halamanNew Proposals To The TRAIN LawJohn Michael OxalesBelum ada peringkat

- Guese - Income Tax - Project - Create - 001Dokumen21 halamanGuese - Income Tax - Project - Create - 001Guese, Christian Nicolas ABelum ada peringkat

- Create LawDokumen46 halamanCreate LawKimberly Claire CaoileBelum ada peringkat

- Create LawDokumen47 halamanCreate LawRen Mar CruzBelum ada peringkat

- NIRC NotesDokumen9 halamanNIRC NotesCen TanaBelum ada peringkat

- CREATE ActDokumen34 halamanCREATE ActErica Dela CruzBelum ada peringkat

- FINAL CREATE BICAM BILL (As of 1 Feb 540pm)Dokumen198 halamanFINAL CREATE BICAM BILL (As of 1 Feb 540pm)KimBelum ada peringkat

- RA 7496-Simplified Net Income Scheme For Self-Employed & Professionals...Dokumen5 halamanRA 7496-Simplified Net Income Scheme For Self-Employed & Professionals...Crislene CruzBelum ada peringkat

- Executive Order No. 37 July 31, 1986Dokumen32 halamanExecutive Order No. 37 July 31, 1986Bobby Olavides SebastianBelum ada peringkat

- RA No. 10963 - Tax Reform For Acceleration and Inclusion (TRAIN Law)Dokumen54 halamanRA No. 10963 - Tax Reform For Acceleration and Inclusion (TRAIN Law)Anostasia NemusBelum ada peringkat

- And Individual Resident Alien of The Philippines. and Individual Resident Alien of The PhilippinesDokumen14 halamanAnd Individual Resident Alien of The Philippines. and Individual Resident Alien of The Philippinesdave_88opBelum ada peringkat

- Provided, That Minimum Wage Earners As Defined in Section 22 (HH) of This Code ShallDokumen5 halamanProvided, That Minimum Wage Earners As Defined in Section 22 (HH) of This Code ShallFrancis DiazBelum ada peringkat

- Republic Act 8424 The Tax Reform Act of 1997 TAX ON INDIVIDUALS SEC. 24. Income Tax Rates.Dokumen23 halamanRepublic Act 8424 The Tax Reform Act of 1997 TAX ON INDIVIDUALS SEC. 24. Income Tax Rates.Dominic EmbodoBelum ada peringkat

- 11-134191-1987-Tio v. Videogram Regulatory BoardDokumen9 halaman11-134191-1987-Tio v. Videogram Regulatory Boarderic akoBelum ada peringkat

- Revenue Regulations 10-2008Dokumen43 halamanRevenue Regulations 10-2008mary lou100% (29)

- RR No. 10-2008Dokumen37 halamanRR No. 10-2008Kristan John ZernaBelum ada peringkat

- Taxation Reviewer 1Dokumen110 halamanTaxation Reviewer 1bigbully23Belum ada peringkat

- Tax On IndividualsDokumen9 halamanTax On IndividualsshakiraBelum ada peringkat

- RA 10963 Tax Reform For Acceleration and InclusionDokumen54 halamanRA 10963 Tax Reform For Acceleration and Inclusionjpeb100% (2)

- RR 30-03Dokumen8 halamanRR 30-03matinikkiBelum ada peringkat

- Tax I-TSN-Finals Coverage: Tax 1-Lectures by Atty. AbrantesDokumen107 halamanTax I-TSN-Finals Coverage: Tax 1-Lectures by Atty. AbrantesEmma PaglalaBelum ada peringkat

- Real Estate Tax ChallengeDokumen24 halamanReal Estate Tax ChallengeChristine Rose Bonilla LikiganBelum ada peringkat

- SPONSOR: Rep. Kowalko & Rep. Keeley & Rep. Lynn & Rep. Potter & Sen. Peterson Reps. Baumbach, J. Johnson, OsienskiDokumen4 halamanSPONSOR: Rep. Kowalko & Rep. Keeley & Rep. Lynn & Rep. Potter & Sen. Peterson Reps. Baumbach, J. Johnson, OsienskiKevinOhlandtBelum ada peringkat

- Tax AmendmentsDokumen109 halamanTax AmendmentsPrincess Hazel GriñoBelum ada peringkat

- CIR Vs CA RetirementDokumen8 halamanCIR Vs CA RetirementAira Mae P. LayloBelum ada peringkat

- Taxation CasesDokumen296 halamanTaxation CasesshelBelum ada peringkat

- Section 7. Section 28 of The National Internal Revenue Code of 1997, AsDokumen6 halamanSection 7. Section 28 of The National Internal Revenue Code of 1997, As0506sheltonBelum ada peringkat

- East African Taxation Law Imposition SummaryDokumen14 halamanEast African Taxation Law Imposition SummaryEDWARD BIRYETEGABelum ada peringkat

- Real Estate Groups Challenge Constitutionality of Minimum Corporate Tax and Creditable Withholding TaxDokumen14 halamanReal Estate Groups Challenge Constitutionality of Minimum Corporate Tax and Creditable Withholding TaxJohn Basil ManuelBelum ada peringkat

- CREBA v. Executive SecretaryDokumen35 halamanCREBA v. Executive Secretarydes_4562Belum ada peringkat

- GCL Retirement Plan Tax RefundDokumen6 halamanGCL Retirement Plan Tax RefundLord AumarBelum ada peringkat

- Be It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledDokumen4 halamanBe It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledMuslimeenSalamBelum ada peringkat

- SB 1944 PDFDokumen7 halamanSB 1944 PDFEdu ParungaoBelum ada peringkat

- Notes - Tax I - Create Law - Nov 24Dokumen9 halamanNotes - Tax I - Create Law - Nov 240506sheltonBelum ada peringkat

- Chamber of Real Estate and Builders' Association v. RomuloDokumen19 halamanChamber of Real Estate and Builders' Association v. RomuloNxxxBelum ada peringkat

- TRAIN (Changes) ???? Pages 2, 6, 10, 14, 15 PDFDokumen5 halamanTRAIN (Changes) ???? Pages 2, 6, 10, 14, 15 PDFblackmail1Belum ada peringkat

- HBN 4125 (Ease of Paying Taxes)Dokumen21 halamanHBN 4125 (Ease of Paying Taxes)DonaldDeLeonBelum ada peringkat

- Commissioner of Internal Revenue v. GCL Retirement Plan G.R. 95022Dokumen6 halamanCommissioner of Internal Revenue v. GCL Retirement Plan G.R. 95022Dino Bernard LapitanBelum ada peringkat

- CREBA Vs RomuloDokumen19 halamanCREBA Vs RomuloVincent OngBelum ada peringkat

- Bar Review Companion: Taxation: Anvil Law Books Series, #4Dari EverandBar Review Companion: Taxation: Anvil Law Books Series, #4Belum ada peringkat

- 1040 Exam Prep Module V: Adjustments to Income or DeductionsDari Everand1040 Exam Prep Module V: Adjustments to Income or DeductionsBelum ada peringkat

- Amendments To 2011 NLRC RulesDokumen11 halamanAmendments To 2011 NLRC Rulesgoannamarie7814Belum ada peringkat

- DOLE Department Order On Night WorkersDokumen5 halamanDOLE Department Order On Night Workersgoannamarie7814100% (1)

- Guidelines For Accreditation of Surety CompanieDokumen7 halamanGuidelines For Accreditation of Surety Companiegoannamarie7814Belum ada peringkat

- NLRC Rules of Procedure 2011Dokumen30 halamanNLRC Rules of Procedure 2011Angela FeliciaBelum ada peringkat

- Peckson vs. Robinsons SupermarketDokumen17 halamanPeckson vs. Robinsons Supermarketgoannamarie7814Belum ada peringkat

- Herida vs. F&C PawnshopDokumen9 halamanHerida vs. F&C Pawnshopgoannamarie7814Belum ada peringkat

- Mercury Drug vs. Araceli DomingoDokumen16 halamanMercury Drug vs. Araceli Domingogoannamarie7814Belum ada peringkat

- PAL vs. ZamoraDokumen16 halamanPAL vs. Zamoragoannamarie7814Belum ada peringkat

- DOLE Department Order On Night WorkersDokumen5 halamanDOLE Department Order On Night Workersgoannamarie7814100% (1)

- Alert Security vs. PasawilanDokumen18 halamanAlert Security vs. Pasawilangoannamarie7814Belum ada peringkat

- Amended Small ClaimsDokumen5 halamanAmended Small ClaimscarterbrantBelum ada peringkat

- Department Order On SeNADokumen9 halamanDepartment Order On SeNAgoannamarie7814Belum ada peringkat

- DOLE Handbook-English Version 2014Dokumen73 halamanDOLE Handbook-English Version 2014Mark Aguinaldo100% (2)

- Humanitarian law-ICRCDokumen2 halamanHumanitarian law-ICRCmugu100% (1)

- Environmental RationaleDokumen97 halamanEnvironmental Rationalegoannamarie7814Belum ada peringkat

- Tax Code AmendedDokumen212 halamanTax Code Amendedgoannamarie7814Belum ada peringkat

- Final Rules of Procedure For Environmental CasesDokumen40 halamanFinal Rules of Procedure For Environmental CasesSuiBelum ada peringkat

- CoxDokumen44 halamanCoxgoannamarie7814Belum ada peringkat

- Tax Code AmendedDokumen212 halamanTax Code Amendedgoannamarie7814Belum ada peringkat

- Environmental RationaleDokumen97 halamanEnvironmental Rationalegoannamarie7814Belum ada peringkat

- REVENUE REGULATIONS NO. 02-98 (§2.78) WITHHOLDING TAXDokumen13 halamanREVENUE REGULATIONS NO. 02-98 (§2.78) WITHHOLDING TAXgoannamarie7814Belum ada peringkat

- Chapter 22Dokumen61 halamanChapter 22Tim LeeBelum ada peringkat

- CHAPTER 13 A - Regular Allowable Itemized DeductionsDokumen4 halamanCHAPTER 13 A - Regular Allowable Itemized DeductionsDeviane CalabriaBelum ada peringkat

- Money Meter Track Your Mandatory and Voluntary ExpensesDokumen1 halamanMoney Meter Track Your Mandatory and Voluntary ExpensesEstaban A GonsalvesBelum ada peringkat

- Unicredit vs. IngDokumen3 halamanUnicredit vs. IngAlina AndrioaeBelum ada peringkat

- Transcript Global BlueDokumen2 halamanTranscript Global Blue6s2rsfv9kgBelum ada peringkat

- Important Information About Form 1099-G: D D Flaumenbaum 2481 Haff Ave North Bellmore Ny 11710-2735Dokumen1 halamanImportant Information About Form 1099-G: D D Flaumenbaum 2481 Haff Ave North Bellmore Ny 11710-2735ddouglasf2357Belum ada peringkat

- BFCI FINAL ENGAGEMENT PROPOSAL Silver FernDokumen2 halamanBFCI FINAL ENGAGEMENT PROPOSAL Silver FernGeram ConcepcionBelum ada peringkat

- 1201 Rental Tax Books of AcctDokumen3 halaman1201 Rental Tax Books of AcctMaddahayota College100% (1)

- Hul PPT (CTP)Dokumen31 halamanHul PPT (CTP)vedantBelum ada peringkat

- Credit Card DetailsDokumen5 halamanCredit Card Detailsjrbossfps75% (8)

- Inv 407306401237Dokumen2 halamanInv 407306401237hesima4637 bodeem.comBelum ada peringkat

- Water BillDokumen1 halamanWater BillAlex R0% (1)

- YatraDokumen1 halamanYatraANANTHAKRISHNANRRBelum ada peringkat

- Reception For Mitt RomneyDokumen2 halamanReception For Mitt RomneySunlight FoundationBelum ada peringkat

- TallyDokumen38 halamanTallyDhananjay RokadeBelum ada peringkat

- Chapter 4Dokumen25 halamanChapter 4crackheads philippinesBelum ada peringkat

- s5 PDFDokumen5 halamans5 PDFKeshav KumarBelum ada peringkat

- Capital One Bank Statement Summary for Andrea SmithDokumen5 halamanCapital One Bank Statement Summary for Andrea SmithUsm amBelum ada peringkat

- Assignment 1 - Fundamental Principles of TaxationDokumen8 halamanAssignment 1 - Fundamental Principles of TaxationMark Paul RamosBelum ada peringkat

- Amit Cotton Industries vs. Principal Commissioner of Customs Gujarat High CourtDokumen49 halamanAmit Cotton Industries vs. Principal Commissioner of Customs Gujarat High CourtMaragani MuraligangadhararaoBelum ada peringkat

- Fredrickson v. Starbucks CorporationDokumen51 halamanFredrickson v. Starbucks Corporationmary engBelum ada peringkat

- Policy Statement - U010146572Dokumen1 halamanPolicy Statement - U010146572Dipak ChandwaniBelum ada peringkat

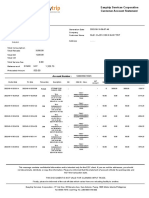

- ESC Customer Account StatementDokumen2 halamanESC Customer Account StatementJake CastañedaBelum ada peringkat

- Financial Statement of Bingo Operations (BC-7, BC-7B)Dokumen7 halamanFinancial Statement of Bingo Operations (BC-7, BC-7B)Jacob GiffenBelum ada peringkat

- ICMAP Business Law Past PapersDokumen2 halamanICMAP Business Law Past Papersmuhzahid786Belum ada peringkat

- BqZ WiFi Voucher Codes ListDokumen1 halamanBqZ WiFi Voucher Codes Listangga13Belum ada peringkat

- AP SetupDokumen7 halamanAP SetupRizwan Jaffer SultanBelum ada peringkat

- Concepts of Taxation: Economics Subject Teacher: Razel G. Taquiso Summer Class 2017Dokumen5 halamanConcepts of Taxation: Economics Subject Teacher: Razel G. Taquiso Summer Class 2017Anonymous mfw5CNq4Belum ada peringkat

- Chapter 1 TB Corporate TaxDokumen15 halamanChapter 1 TB Corporate TaxLahari NeelapareddyBelum ada peringkat

- B-4 Account Computation PFC SuerteDokumen3 halamanB-4 Account Computation PFC SuerteElmer AlasBelum ada peringkat