Anda mungkin juga menyukai

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5782)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (399)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (72)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (890)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (587)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (265)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (119)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- Economic Nationalism As A Challenge To Economic LiberalismDokumen23 halamanEconomic Nationalism As A Challenge To Economic LiberalismBejmanjinBelum ada peringkat

- United States Court of Appeals, Fourth CircuitDokumen8 halamanUnited States Court of Appeals, Fourth CircuitScribd Government DocsBelum ada peringkat

- Let's Talk Book 2Dokumen17 halamanLet's Talk Book 2Valentina Verginia100% (1)

- 12.1 INVENTORY ITEM $ VAlUEICASEDokumen5 halaman12.1 INVENTORY ITEM $ VAlUEICASERonald Huanca Calle50% (4)

- The DragonDokumen2 halamanThe DragonNana NaanBelum ada peringkat

- Arl Ship ChandlingDokumen7 halamanArl Ship ChandlingGabriel Canlas AblolaBelum ada peringkat

- Cat 94Dokumen255 halamanCat 94Fakerooooooooooooooooo100% (1)

- Argumentation and DebateDokumen6 halamanArgumentation and DebateKristalFaithRamirezPagaduanBelum ada peringkat

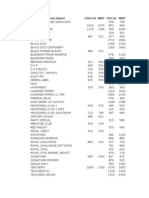

- Price ListDokumen28 halamanPrice Listhomerahul9070Belum ada peringkat

- StabilityDokumen77 halamanStabilitybabissoul100% (2)

- KiG 26 KnjigePrirucnikDokumen6 halamanKiG 26 KnjigePrirucnikIvanBagaric0% (1)

- Chapter 5 - ConclusionsDokumen7 halamanChapter 5 - ConclusionsANA MAE DE LA CRUZBelum ada peringkat

- The Leaf: Short Notes Class 6 ScienceDokumen4 halamanThe Leaf: Short Notes Class 6 ScienceParimala DhanasekaranBelum ada peringkat

- Improvement of Layout Increases ProductivityDokumen21 halamanImprovement of Layout Increases ProductivityTesfa TeshomeBelum ada peringkat

- Tour Report - Quality Control and Improvement of Glass Industries LimitedDokumen30 halamanTour Report - Quality Control and Improvement of Glass Industries LimitedCryptic Sufi0% (1)

- Cambridge International General Certificate of Secondary EducationDokumen16 halamanCambridge International General Certificate of Secondary EducationSheimaBelum ada peringkat

- Presentation Slides: Contemporary Strategy Analysis: Concepts, Techniques, ApplicationsDokumen11 halamanPresentation Slides: Contemporary Strategy Analysis: Concepts, Techniques, ApplicationsMonika SharmaBelum ada peringkat

- Chaotic Sword GodDokumen1.928 halamanChaotic Sword Godxdmhundz999100% (1)

- Ceremony - Baby Dedication PDFDokumen5 halamanCeremony - Baby Dedication PDFrafaelgsccBelum ada peringkat

- Tumbler Test For CokeDokumen3 halamanTumbler Test For CokeDavid CazorlaBelum ada peringkat

- Southern Majority 20/20 Insights PollingDokumen5 halamanSouthern Majority 20/20 Insights PollingSoMa2022Belum ada peringkat

- Colonial Letters FolderDokumen6 halamanColonial Letters Folderapi-198803582Belum ada peringkat

- Chaucer To Shakespearean PeriodDokumen28 halamanChaucer To Shakespearean PeriodSusrita DasBelum ada peringkat

- Nighshift Magazine - December 2011Dokumen24 halamanNighshift Magazine - December 2011wpl955gBelum ada peringkat

- Indore - Smart City Proposal - MasterplanDokumen92 halamanIndore - Smart City Proposal - MasterplansiddarthsoniBelum ada peringkat

- Job Offer Letter Agreement Paris Job Pierre Gattaz PDFDokumen3 halamanJob Offer Letter Agreement Paris Job Pierre Gattaz PDFBiki Dutta100% (2)

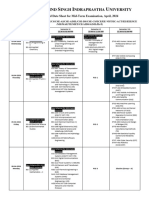

- Mid Term Date Sheet - pq0NsApDokumen2 halamanMid Term Date Sheet - pq0NsApSahil HansBelum ada peringkat

- Celular LG CodesDokumen6 halamanCelular LG CodesGeorgeBelum ada peringkat

- Dos Vs Linux PDFDokumen2 halamanDos Vs Linux PDFJawad Sandhu0% (1)

- Therapy Format I. Therapy: News Sharing Therapy Date: July 28, 2021 II. Materials/EquipmentDokumen2 halamanTherapy Format I. Therapy: News Sharing Therapy Date: July 28, 2021 II. Materials/EquipmentAesthea BondadBelum ada peringkat