Anda mungkin juga menyukai

- Consumer MathDokumen28 halamanConsumer MathMylene Magalong De GuzmanBelum ada peringkat

- More Minute Math Drills, Grades 3 - 6: Multiplication and DivisionDari EverandMore Minute Math Drills, Grades 3 - 6: Multiplication and DivisionPenilaian: 5 dari 5 bintang5/5 (1)

- Little Black Book of Options Secrets AbDokumen12 halamanLittle Black Book of Options Secrets AbRaju.KonduruBelum ada peringkat

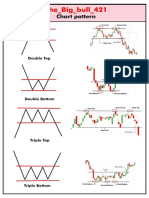

- Big Bull Ghost TownDokumen5 halamanBig Bull Ghost TownMAHEMOOD SHAH100% (10)

- eBookTraders JournalJanFeb2006Dokumen76 halamaneBookTraders JournalJanFeb2006mpamcr100% (1)

- Technical AnalysisDokumen69 halamanTechnical AnalysisMRINMOY KARMAKAR100% (1)

- International FinanceDokumen32 halamanInternational FinanceahmeddanafBelum ada peringkat

- Rakesh Jhunjhunwala'sDokumen34 halamanRakesh Jhunjhunwala'sneo26950% (2)

- Vsa PDFDokumen7 halamanVsa PDFGerrardBelum ada peringkat

- IMT CeresDokumen7 halamanIMT CeresHarsha HoneyBelum ada peringkat

- Quality Kitchens Meat Loaf Mix: Team 8Dokumen7 halamanQuality Kitchens Meat Loaf Mix: Team 8JaouadiBelum ada peringkat

- Assignment Schumpeter CaseDokumen1 halamanAssignment Schumpeter CaseValentin Is0% (1)

- Acca BPP Practice & Revision KitDokumen505 halamanAcca BPP Practice & Revision KitHenry Fayol89% (9)

- Montessori School Financial Plan V1Dokumen8 halamanMontessori School Financial Plan V1kazimBelum ada peringkat

- AdxDokumen4 halamanAdxDarshanBelum ada peringkat

- Market RatiosDokumen4 halamanMarket RatiosHamid NasirBelum ada peringkat

- FinanzasDokumen2 halamanFinanzasRod MarquezBelum ada peringkat

- FSA Project.. Sakhawat Hossain..Id-20-91724-2.Dokumen11 halamanFSA Project.. Sakhawat Hossain..Id-20-91724-2.Durjoy SakhawatBelum ada peringkat

- Ratio Analysis of Square Pharmaceuticals LTDDokumen4 halamanRatio Analysis of Square Pharmaceuticals LTDIfaz Mahsinul HaqueBelum ada peringkat

- 高顿财经ACCA acca.gaodun.cn: Advanced Performance ManagementDokumen12 halaman高顿财经ACCA acca.gaodun.cn: Advanced Performance ManagementIskandar BudionoBelum ada peringkat

- Time SeriesDokumen6 halamanTime SeriesSalman ButtBelum ada peringkat

- Ratio Analysis of Crown CementDokumen9 halamanRatio Analysis of Crown CementSadi The-Darkraven KafiBelum ada peringkat

- Taller - Franklin RodilDokumen16 halamanTaller - Franklin Rodilalejandro rodilBelum ada peringkat

- Habib Bank Limeted Ratio Analysis of Five Years 2005-2009 Appendix A-1Dokumen24 halamanHabib Bank Limeted Ratio Analysis of Five Years 2005-2009 Appendix A-1surajoadBelum ada peringkat

- Vijay Project Review - 2Dokumen12 halamanVijay Project Review - 2NALLANKI RAJA KUMARBelum ada peringkat

- Tema 2 - Econometrie - Ungureanu Cristian Amedeo Mihail - Cig Id An 2 - Grupa 2Dokumen4 halamanTema 2 - Econometrie - Ungureanu Cristian Amedeo Mihail - Cig Id An 2 - Grupa 2cornel grigorasBelum ada peringkat

- Latihan Spss 3Dokumen26 halamanLatihan Spss 3ulumBelum ada peringkat

- Informe de Laboratorio Molaridad EtcDokumen8 halamanInforme de Laboratorio Molaridad EtcShadia PanizaBelum ada peringkat

- SubrosDokumen31 halamanSubrossumit3902Belum ada peringkat

- Data Olah Eviews Bagi 100Dokumen13 halamanData Olah Eviews Bagi 100kurvax konsultanBelum ada peringkat

- Chapter 6 - 2020Dokumen62 halamanChapter 6 - 2020Nga Ying WuBelum ada peringkat

- Average Collection PeriodDokumen5 halamanAverage Collection PeriodAmad IsmailBelum ada peringkat

- Accounting Question 2Dokumen8 halamanAccounting Question 2Moustafa Almoataz100% (1)

- Exportadores Periodo 2012 1 2013 2 2014 3 2015 4 2016 5: Demanda en El MundoDokumen6 halamanExportadores Periodo 2012 1 2013 2 2014 3 2015 4 2016 5: Demanda en El MundoJenryAvalosBelum ada peringkat

- 11 Plus Exam Maths Primer (Paper 1) Only Allow 30 Minutes To Complete This Test Calculators Are Not AllowedDokumen3 halaman11 Plus Exam Maths Primer (Paper 1) Only Allow 30 Minutes To Complete This Test Calculators Are Not AllowedAaroushan RichardBelum ada peringkat

- RESOLUCION REPASO No 1Dokumen3 halamanRESOLUCION REPASO No 1Rosario GonzalesBelum ada peringkat

- Revised Financial PlanDokumen11 halamanRevised Financial PlanJhosep EsquivelBelum ada peringkat

- Lecture 7 Index Numbers 2Dokumen23 halamanLecture 7 Index Numbers 2Emmmanuel ArthurBelum ada peringkat

- Tugas Anggaran Perusahaan X y Tahun Ke Penjualan: Regression StatisticsDokumen2 halamanTugas Anggaran Perusahaan X y Tahun Ke Penjualan: Regression Statisticsadi anggoroBelum ada peringkat

- Calculating Industry Debt: Shaiham Hwawell Family Prime Safko Daccadye TunnghaiDokumen4 halamanCalculating Industry Debt: Shaiham Hwawell Family Prime Safko Daccadye TunnghaikajalBelum ada peringkat

- Reliance IndustrDokumen10 halamanReliance IndustrCarl CjBelum ada peringkat

- Ratio Analysis of Company Report (2012/13) : Short Term Solvency Ratios/liquidity RatiosDokumen8 halamanRatio Analysis of Company Report (2012/13) : Short Term Solvency Ratios/liquidity RatiosRehan AbdullahBelum ada peringkat

- Diesel or Electric Jeepney A Case Study of Public Transport Investment in The Philippines Using Real Options ApproachDokumen16 halamanDiesel or Electric Jeepney A Case Study of Public Transport Investment in The Philippines Using Real Options ApproachRhona Liza CruzBelum ada peringkat

- Executive SummaryDokumen12 halamanExecutive SummaryShehbaz HameedBelum ada peringkat

- Presentasi: SOAL Dan JawabanDokumen18 halamanPresentasi: SOAL Dan JawabanAkkhu Anx AmkBelum ada peringkat

- Reliance IndustrDokumen10 halamanReliance Industrravi.youBelum ada peringkat

- Ratio Analysis TanyaDokumen10 halamanRatio Analysis Tanyatanya chauhanBelum ada peringkat

- Bufe Aaron A. SuperheaterDokumen5 halamanBufe Aaron A. SuperheaterArabia, Elmo C.Belum ada peringkat

- Reviewer LETDokumen5 halamanReviewer LETIrene Grace Edralin AdenaBelum ada peringkat

- Standalone Financial Results, Limited Review Report For December 31, 2016 (Result)Dokumen5 halamanStandalone Financial Results, Limited Review Report For December 31, 2016 (Result)Shyam SunderBelum ada peringkat

- Reliance IndustrDokumen10 halamanReliance IndustrAman RajBelum ada peringkat

- Group Project On Corporate Finance BSRM Xtreme & GPH Ispat LTDDokumen16 halamanGroup Project On Corporate Finance BSRM Xtreme & GPH Ispat LTDTamim ChowdhuryBelum ada peringkat

- Curso Sesión 3Dokumen21 halamanCurso Sesión 3Cristopher Amir Hernandez AlvarezBelum ada peringkat

- 4.3. Profitability RatioDokumen5 halaman4.3. Profitability RatioKashmi VishnayaBelum ada peringkat

- Structural Change in Developing Countries Has It Decreased Gender InequalityDokumen12 halamanStructural Change in Developing Countries Has It Decreased Gender Inequalitylifetips6786Belum ada peringkat

- Ratio AnalysisDokumen2 halamanRatio AnalysisShalehBelum ada peringkat

- Ch1 Solutions 1Dokumen59 halamanCh1 Solutions 1YoungCheon JungBelum ada peringkat

- Reliance IndustrDokumen10 halamanReliance IndustrneroBelum ada peringkat

- Financial Analysis of NMB Bank For The Fiscal Year of 2073: Balance SheetDokumen4 halamanFinancial Analysis of NMB Bank For The Fiscal Year of 2073: Balance SheetKamana Thp MgrBelum ada peringkat

- Xyz Company: Profit and Loss Account For The Year EndedDokumen19 halamanXyz Company: Profit and Loss Account For The Year EndedYaswanth MaripiBelum ada peringkat

- Analyze and Benchmark The CompanyDokumen31 halamanAnalyze and Benchmark The CompanyCH OMBelum ada peringkat

- Kerja Projek Matematik Tambahan 2019Dokumen18 halamanKerja Projek Matematik Tambahan 2019anon_157118857Belum ada peringkat

- Assignmen3 (Mahmoud Abd El Aziz)Dokumen5 halamanAssignmen3 (Mahmoud Abd El Aziz)Mahmoud ZizoBelum ada peringkat

- 2307Dokumen2 halaman2307Vladan PrigaraBelum ada peringkat

- Timeseries - ForecastingDokumen3 halamanTimeseries - ForecastingMehulsinh SindhaBelum ada peringkat

- Rasio Lancar (Current Ratio)Dokumen3 halamanRasio Lancar (Current Ratio)rezaaaBelum ada peringkat

- Analisis de Sismico (Portico Plano) Ejemplo 1Dokumen12 halamanAnalisis de Sismico (Portico Plano) Ejemplo 1Marco Antonio Marceliano SifuentesBelum ada peringkat

- Book 1Dokumen1 halamanBook 1AJAY PAL SINGHBelum ada peringkat

- Financial Analysis of Power SectorDokumen19 halamanFinancial Analysis of Power SectorPKBelum ada peringkat

- Gabungin PenforDokumen4 halamanGabungin Penforsella puspita handayaniBelum ada peringkat

- MssaDokumen9 halamanMssaToma AmaliaBelum ada peringkat

- Strategic Managment in PTCL: Group MembersDokumen18 halamanStrategic Managment in PTCL: Group MembersHamid NasirBelum ada peringkat

- StrategicDokumen10 halamanStrategicHamid NasirBelum ada peringkat

- Equipment & Machinery Equipment Unit Price Total Cost (RS.) (RS.)Dokumen13 halamanEquipment & Machinery Equipment Unit Price Total Cost (RS.) (RS.)Hamid NasirBelum ada peringkat

- Analysis of Financial StatementsDokumen48 halamanAnalysis of Financial StatementsHamid NasirBelum ada peringkat

- Sale Agreement: 1. The PartiesDokumen1 halamanSale Agreement: 1. The PartiesHamid NasirBelum ada peringkat

- Capacity of PartiesDokumen3 halamanCapacity of PartiesHamid NasirBelum ada peringkat

- DiscfacDokumen3 halamanDiscfacapi-3855915Belum ada peringkat

- The Ratio Analysis Technique Applied To PersonalDokumen15 halamanThe Ratio Analysis Technique Applied To PersonalladycocoBelum ada peringkat

- Topic 2 - Introduction To Accounting Concept and ConventionDokumen27 halamanTopic 2 - Introduction To Accounting Concept and ConventionJamilah Edward50% (2)

- Chapter 10 Solutions - Foundations of Finance 8th Edition - CheggDokumen14 halamanChapter 10 Solutions - Foundations of Finance 8th Edition - ChegghshshdhdBelum ada peringkat

- Dwnload Full Fundamentals of Corporate Finance 2nd Edition Parrino Test Bank PDFDokumen35 halamanDwnload Full Fundamentals of Corporate Finance 2nd Edition Parrino Test Bank PDFpuddyshaunta100% (11)

- Case Study - Black Jack AntiquesDokumen5 halamanCase Study - Black Jack AntiquesJP LoredoBelum ada peringkat

- The Essentials of An Efficient Market - FinalDokumen30 halamanThe Essentials of An Efficient Market - FinalAnita Kedare100% (1)

- How Efficient Is Naive Portfolio Diversification? An Educational NoteDokumen18 halamanHow Efficient Is Naive Portfolio Diversification? An Educational NoteAhsan ZaidiBelum ada peringkat

- Announced Interest Rate Chart of The Scheduled Banks (Deposit Rate) (Percentage Per Annum)Dokumen2 halamanAnnounced Interest Rate Chart of The Scheduled Banks (Deposit Rate) (Percentage Per Annum)riyadeeeBelum ada peringkat

- Sample Final Exam Bbek4203 - 1Dokumen4 halamanSample Final Exam Bbek4203 - 1Marlissa Nur OthmanBelum ada peringkat

- Gafla ReviewDokumen2 halamanGafla Reviewsoumya_1990100% (1)

- The Value of Intraday Prices and Volume Using Volatility-Based Trading StrategiesDokumen40 halamanThe Value of Intraday Prices and Volume Using Volatility-Based Trading StrategiesSubrata BhattacherjeeBelum ada peringkat

- Sbi Bank Clerk 2008 Solved PaperDokumen33 halamanSbi Bank Clerk 2008 Solved PaperRamana Reddy100% (3)

- 12 Chapter 3Dokumen18 halaman12 Chapter 3penumudi233Belum ada peringkat

- Indian Financial SystemDokumen5 halamanIndian Financial SystemDurga Prasad NallaBelum ada peringkat

- Nse BseDokumen11 halamanNse BseRimi SharmaBelum ada peringkat

- Deemer On 4 Yr Cycle UpdateDokumen9 halamanDeemer On 4 Yr Cycle UpdatediannebBelum ada peringkat

- Bond Valuation SlidesDokumen26 halamanBond Valuation Slideslibison1Belum ada peringkat