Anda mungkin juga menyukai

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5795)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1091)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- Best Trusts and Estates OutlineDokumen84 halamanBest Trusts and Estates OutlineJavi Luis100% (4)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- KISS Notes The World CommunicatesDokumen30 halamanKISS Notes The World CommunicatesJenniferBackhus100% (4)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- New Values of The Required Hydrophilic-LipophilicBalance For Oil in Water Emulsions of Solid Fatty Acids and AlcoholsDokumen4 halamanNew Values of The Required Hydrophilic-LipophilicBalance For Oil in Water Emulsions of Solid Fatty Acids and AlcoholsRicardo100% (3)

- Different Types of Speeches According To DeliveryDokumen18 halamanDifferent Types of Speeches According To DeliveryJoy Agustin100% (1)

- How To Reset AutoCAD To Defaults - AutoCAD 2019 - Autodesk Knowledge NetworkDokumen11 halamanHow To Reset AutoCAD To Defaults - AutoCAD 2019 - Autodesk Knowledge NetworkZina MorBelum ada peringkat

- Ieee - 2030 Smart GridDokumen26 halamanIeee - 2030 Smart GridarturoelectricaBelum ada peringkat

- Claudia Jones Nuclear TestingDokumen25 halamanClaudia Jones Nuclear TestingDaniel Lee Eisenberg JacobsBelum ada peringkat

- Continuity Change State of Process of Task ofDokumen1 halamanContinuity Change State of Process of Task ofDaniel Lee Eisenberg JacobsBelum ada peringkat

- Beta Anomaly An Ex-Ante Tail RiskDokumen104 halamanBeta Anomaly An Ex-Ante Tail RiskDaniel Lee Eisenberg JacobsBelum ada peringkat

- Theophilus Capital Against: Fisk Labor1Dokumen9 halamanTheophilus Capital Against: Fisk Labor1Daniel Lee Eisenberg Jacobs100% (1)

- Why The Euro Will Rival The Dollar PDFDokumen25 halamanWhy The Euro Will Rival The Dollar PDFDaniel Lee Eisenberg JacobsBelum ada peringkat

- 1st International: Djacobs November 2020Dokumen5 halaman1st International: Djacobs November 2020Daniel Lee Eisenberg JacobsBelum ada peringkat

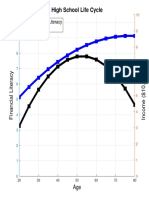

- High School Life Cycle: Financial Literacy IncomeDokumen1 halamanHigh School Life Cycle: Financial Literacy IncomeDaniel Lee Eisenberg JacobsBelum ada peringkat

- Conference Group For Central European History of The American Historical AssociationDokumen9 halamanConference Group For Central European History of The American Historical AssociationDaniel Lee Eisenberg JacobsBelum ada peringkat

- Karl Kautsky Republic and Social Democra PDFDokumen4 halamanKarl Kautsky Republic and Social Democra PDFDaniel Lee Eisenberg JacobsBelum ada peringkat

- Borel Sets PDFDokumen181 halamanBorel Sets PDFDaniel Lee Eisenberg Jacobs100% (1)

- Necessary and Sufficient Conditions For Dynamic OptimizationDokumen18 halamanNecessary and Sufficient Conditions For Dynamic OptimizationDaniel Lee Eisenberg JacobsBelum ada peringkat

- The Saving Behavior of Public Vocational High School Students of Business and Management Program in Semarang SitiDokumen8 halamanThe Saving Behavior of Public Vocational High School Students of Business and Management Program in Semarang SitiDaniel Lee Eisenberg JacobsBelum ada peringkat

- Individualization of Robo-AdviceDokumen8 halamanIndividualization of Robo-AdviceDaniel Lee Eisenberg JacobsBelum ada peringkat

- Cover FERCDokumen1 halamanCover FERCDaniel Lee Eisenberg JacobsBelum ada peringkat

- Teach-In: Government of The People, by The People, For The PeopleDokumen24 halamanTeach-In: Government of The People, by The People, For The PeopleDaniel Lee Eisenberg JacobsBelum ada peringkat

- Gpebook PDFDokumen332 halamanGpebook PDFDaniel Lee Eisenberg JacobsBelum ada peringkat

- Bank Loan Loss ProvisioningDokumen17 halamanBank Loan Loss ProvisioningDaniel Lee Eisenberg JacobsBelum ada peringkat

- Simple BeamerDokumen25 halamanSimple BeamerDaniel Lee Eisenberg JacobsBelum ada peringkat

- Product Manual 85018V2 (Revision F) : 505E Digital Governor For Extraction Steam TurbinesDokumen160 halamanProduct Manual 85018V2 (Revision F) : 505E Digital Governor For Extraction Steam Turbinesrahilshah100Belum ada peringkat

- Machine Learning and Iot For Prediction and Detection of StressDokumen5 halamanMachine Learning and Iot For Prediction and Detection of StressAjj PatelBelum ada peringkat

- Recount TextDokumen17 halamanRecount TextalunaBelum ada peringkat

- Jones Rural School - 300555Dokumen13 halamanJones Rural School - 300555Roland Acob Del Rosario Jr.100% (1)

- Polytechnic University of The Philippines Basketball Athletes' Superstitious Rituals and Its Effects in Their Game PerformanceDokumen25 halamanPolytechnic University of The Philippines Basketball Athletes' Superstitious Rituals and Its Effects in Their Game PerformanceJewo CanterasBelum ada peringkat

- Test 04 AnswerDokumen16 halamanTest 04 AnswerCửu KhoaBelum ada peringkat

- Mission: Children'SDokumen36 halamanMission: Children'SWillian A. Palacio MurilloBelum ada peringkat

- Child and Adolescent Psychiatry ST1Dokumen6 halamanChild and Adolescent Psychiatry ST1danielBelum ada peringkat

- Intersection of Psychology With Architecture Final ReportDokumen22 halamanIntersection of Psychology With Architecture Final Reportmrunmayee pandeBelum ada peringkat

- Manila Trading & Supply Co. v. Manila Trading Labor Assn (1953)Dokumen2 halamanManila Trading & Supply Co. v. Manila Trading Labor Assn (1953)Zan BillonesBelum ada peringkat

- How The Tortoise Got Its ScarsDokumen3 halamanHow The Tortoise Got Its ScarsAngelenwBelum ada peringkat

- RB September 2014 The One Thing Kekuatan Fokus Untuk Mendorong ProduktivitasDokumen2 halamanRB September 2014 The One Thing Kekuatan Fokus Untuk Mendorong ProduktivitasRifat TaopikBelum ada peringkat

- Sample Legal Advice Problems and AnswersDokumen4 halamanSample Legal Advice Problems and AnswersJake Bryson DancelBelum ada peringkat

- Survey Questionnaire FsDokumen6 halamanSurvey Questionnaire FsHezell Leah ZaragosaBelum ada peringkat

- Conference Diplomacy: After Kenya's Independence in 1963, A Secession Movement Begun inDokumen3 halamanConference Diplomacy: After Kenya's Independence in 1963, A Secession Movement Begun inPeter KBelum ada peringkat

- Section 22 Knapsack CipherDokumen9 halamanSection 22 Knapsack CipherchitrgBelum ada peringkat

- Kutuzov A Life in War and Peace Alexander Mikaberidze 2 Full ChapterDokumen67 halamanKutuzov A Life in War and Peace Alexander Mikaberidze 2 Full Chapterjanice.brooks978100% (6)

- 5 Methods: Mark Bevir Jason BlakelyDokumen21 halaman5 Methods: Mark Bevir Jason BlakelyGiulio PalmaBelum ada peringkat

- Dina Iordanova - Women in Balkan Cinema, Surviving On The MarginsDokumen17 halamanDina Iordanova - Women in Balkan Cinema, Surviving On The MarginsimparatulverdeBelum ada peringkat

- Weathering Week 2 Lesson PlanDokumen2 halamanWeathering Week 2 Lesson Planapi-561672151Belum ada peringkat

- Review Paper On Three Phase Fault AnalysisDokumen6 halamanReview Paper On Three Phase Fault AnalysisPritesh Singh50% (2)

- Notes Ilw1501 Introduction To LawDokumen11 halamanNotes Ilw1501 Introduction To Lawunderstand ingBelum ada peringkat

- R15 Aerodynamics Notes PDFDokumen61 halamanR15 Aerodynamics Notes PDFRahil MpBelum ada peringkat

- Spa IpoDokumen2 halamanSpa IpoJeff E. DatingalingBelum ada peringkat