Anda mungkin juga menyukai

- Solvents: Northwest EuropeDokumen7 halamanSolvents: Northwest EuropegeorgevarsasBelum ada peringkat

- Solvents: Northwest EuropeDokumen9 halamanSolvents: Northwest EuropegeorgevarsasBelum ada peringkat

- KBF (E5.2) : Service ManualDokumen140 halamanKBF (E5.2) : Service ManualgeorgevarsasBelum ada peringkat

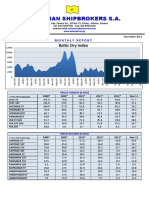

- Athenian Shipbrokers - Monthy Report - 13.11.15 PDFDokumen20 halamanAthenian Shipbrokers - Monthy Report - 13.11.15 PDFgeorgevarsas0% (1)

- Athenian Shipbrokers - Monthy Report - 13.12.15 PDFDokumen18 halamanAthenian Shipbrokers - Monthy Report - 13.12.15 PDFgeorgevarsasBelum ada peringkat

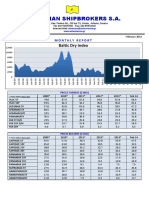

- Athenian Shipbrokers - Monthy Report - 14.02.15 PDFDokumen19 halamanAthenian Shipbrokers - Monthy Report - 14.02.15 PDFgeorgevarsasBelum ada peringkat

- Athenian Shipbrokers - Monthy Report - 14.01.15 PDFDokumen18 halamanAthenian Shipbrokers - Monthy Report - 14.01.15 PDFgeorgevarsasBelum ada peringkat

- C H S&P W B: Larkson Ellas Eekly UlletinDokumen3 halamanC H S&P W B: Larkson Ellas Eekly UlletingeorgevarsasBelum ada peringkat

- C H S&P W B: Larkson Ellas Eekly UlletinDokumen2 halamanC H S&P W B: Larkson Ellas Eekly UlletingeorgevarsasBelum ada peringkat

- C H S&P W B: Larkson Ellas Eekly UlletinDokumen2 halamanC H S&P W B: Larkson Ellas Eekly UlletingeorgevarsasBelum ada peringkat

- Athenian Shipbrokers - Monthy Report - 14.07.15 PDFDokumen18 halamanAthenian Shipbrokers - Monthy Report - 14.07.15 PDFgeorgevarsasBelum ada peringkat

- C H S&P W B: Larkson Ellas Eekly UlletinDokumen2 halamanC H S&P W B: Larkson Ellas Eekly UlletingeorgevarsasBelum ada peringkat

- Athenian Shipbrokers - Monthy Report - 14.08.15Dokumen17 halamanAthenian Shipbrokers - Monthy Report - 14.08.15georgevarsasBelum ada peringkat

- Athenian Shipbrokers S.A.: Baltic Dry IndexDokumen17 halamanAthenian Shipbrokers S.A.: Baltic Dry IndexgeorgevarsasBelum ada peringkat

- Advanced - Week 52 - 16.12.26 PDFDokumen9 halamanAdvanced - Week 52 - 16.12.26 PDFgeorgevarsasBelum ada peringkat

- Advanced - Week 12 - 16.03.18 PDFDokumen10 halamanAdvanced - Week 12 - 16.03.18 PDFgeorgevarsasBelum ada peringkat

- Advanced - Week 24 - 16.06.10Dokumen11 halamanAdvanced - Week 24 - 16.06.10georgevarsasBelum ada peringkat

- Athenian Shipbrokers - Monthy Report - 13.11.15 PDFDokumen20 halamanAthenian Shipbrokers - Monthy Report - 13.11.15 PDFgeorgevarsas0% (1)

- Advanced - Week 23 - 16.06.03 PDFDokumen11 halamanAdvanced - Week 23 - 16.06.03 PDFgeorgevarsasBelum ada peringkat

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (74)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- Reprinted: Danao - Consuelo, Camotes Departure: Sat, Apr 15, 2023 5:30 AmDokumen1 halamanReprinted: Danao - Consuelo, Camotes Departure: Sat, Apr 15, 2023 5:30 AmMary Jane MarfeBelum ada peringkat

- Certificate Program in Export-Import Management: (Online)Dokumen5 halamanCertificate Program in Export-Import Management: (Online)dollyBelum ada peringkat

- Airbus A380Dokumen21 halamanAirbus A380rpraj3135Belum ada peringkat

- Ism Form Follow SheetDokumen2 halamanIsm Form Follow SheetSelcuk UzunBelum ada peringkat

- Exxon Mobil MESC 2010 Rev1Dokumen55 halamanExxon Mobil MESC 2010 Rev1Anonymous 7z6OzoBelum ada peringkat

- Daraz Packaging GuidelinesDokumen22 halamanDaraz Packaging GuidelinesDaraz Seller Support80% (5)

- Sweet Lines v. TevesDokumen3 halamanSweet Lines v. TevesMaria Analyn100% (1)

- Industry Profile of Courier IndustryDokumen9 halamanIndustry Profile of Courier IndustryTharique Anwar100% (3)

- Century PlyDokumen36 halamanCentury PlyKuldeep Sharma0% (1)

- Inter Company InvoicingDokumen41 halamanInter Company InvoicingShanti BollinaBelum ada peringkat

- 外貿英語常用詞語和術語Dokumen5 halaman外貿英語常用詞語和術語Eng4ChineseBelum ada peringkat

- Clearance For Inspection Form (Initial) Rev 2Dokumen1 halamanClearance For Inspection Form (Initial) Rev 2Maria Angela A. CabunganBelum ada peringkat

- Kings of Air and Steam RulesDokumen20 halamanKings of Air and Steam RulesJonathanBelum ada peringkat

- RoroDokumen29 halamanRoroEko SuherBelum ada peringkat

- Uster OfferDokumen18 halamanUster OfferArif ApuBelum ada peringkat

- Gati LogisticDokumen12 halamanGati LogisticNaveen MootaBelum ada peringkat

- Bectochem Consultants & Engineers Pvt. LTD.: Junction Box FLP/ Weather Proof 240 Length 155 Width 100 HeightDokumen1 halamanBectochem Consultants & Engineers Pvt. LTD.: Junction Box FLP/ Weather Proof 240 Length 155 Width 100 HeightBhavin VoraBelum ada peringkat

- 14.30 Joel Grau Lara, ClarksonsDokumen7 halaman14.30 Joel Grau Lara, ClarksonsMohd AliBelum ada peringkat

- Inv190 PDFDokumen4 halamanInv190 PDFHitesh ThakkerBelum ada peringkat

- Company ProfileDokumen14 halamanCompany ProfileDinesh SharmaBelum ada peringkat

- l3 Carrying UnitDokumen43 halamanl3 Carrying Unitshuting2teohBelum ada peringkat

- 51 Modular PlantDokumen8 halaman51 Modular Plantdarra724Belum ada peringkat

- MIS Company ProfileDokumen12 halamanMIS Company ProfileEngDbtBelum ada peringkat

- Calcium CarbonateDokumen2 halamanCalcium CarbonatemohammadazraiBelum ada peringkat

- II08.240 Damage Survey ReportDokumen13 halamanII08.240 Damage Survey Reportapi-19624453100% (8)

- Lamb T.A Ship Design Proced - oct.1969.MTDokumen44 halamanLamb T.A Ship Design Proced - oct.1969.MTNunzioBestBelum ada peringkat

- State Bank Form e Part 1 PDFDokumen2 halamanState Bank Form e Part 1 PDFfaizan009Belum ada peringkat

- Passport: Please Fill in and Send ToDokumen5 halamanPassport: Please Fill in and Send ToRenzo TipianBelum ada peringkat

- JNPT Div A Group1Dokumen36 halamanJNPT Div A Group1Akanksha ShuklaBelum ada peringkat

- Ship Design - Main DimensionsDokumen10 halamanShip Design - Main DimensionsMuhammad Hafidz100% (5)