Anda mungkin juga menyukai

- Textbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingDari EverandTextbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingBelum ada peringkat

- Analysis of Balance Sheet-As Per 31 March 2010,2011 - (Vertical Format)Dokumen2 halamanAnalysis of Balance Sheet-As Per 31 March 2010,2011 - (Vertical Format)Megha ShahBelum ada peringkat

- IGNOU MBA MS - 04 Solved Assignment 2011Dokumen16 halamanIGNOU MBA MS - 04 Solved Assignment 2011Kiran PattnaikBelum ada peringkat

- IGNOU MBA MS - 04 Solved Assignment 2011Dokumen12 halamanIGNOU MBA MS - 04 Solved Assignment 2011Nazif LcBelum ada peringkat

- Financial Management IIBMDokumen5 halamanFinancial Management IIBMcarnowalt100% (1)

- Projected Financial StatementsDokumen2 halamanProjected Financial StatementsAcademic StuffBelum ada peringkat

- Sources of FundsDokumen6 halamanSources of FundsNeetika KalyaniBelum ada peringkat

- Coles GroupDokumen9 halamanColes GroupSubash UpadhyayBelum ada peringkat

- FM Theory Meaning of Financial ManagementDokumen10 halamanFM Theory Meaning of Financial ManagementDarshan MoreBelum ada peringkat

- Topic 4 Tutorial SolutionsDokumen10 halamanTopic 4 Tutorial SolutionsKitty666Belum ada peringkat

- PSPC Activist Shareholders Group: Presentation of Demands To The ManagementDokumen19 halamanPSPC Activist Shareholders Group: Presentation of Demands To The Managementανατολή και πετύχετεBelum ada peringkat

- Business Finance Assgn.Dokumen7 halamanBusiness Finance Assgn.Lesley DenisBelum ada peringkat

- 9 Framework For Preparation - Presentation of Financial StatementsDokumen13 halaman9 Framework For Preparation - Presentation of Financial StatementssmartshivenduBelum ada peringkat

- Chapter 8Dokumen6 halamanChapter 8Nor AzuraBelum ada peringkat

- AEV A17Q Q2Jun2012 (3oct2012)Dokumen42 halamanAEV A17Q Q2Jun2012 (3oct2012)cuonghienBelum ada peringkat

- Full Download Solution Manual For Financial Accounting Libby Libby Short 8th Edition PDF Full ChapterDokumen36 halamanFull Download Solution Manual For Financial Accounting Libby Libby Short 8th Edition PDF Full Chapterunwill.eadishvj8p100% (21)

- Objectives of Financial PlanningDokumen9 halamanObjectives of Financial Planning220479Belum ada peringkat

- Fund Flow StatementDokumen16 halamanFund Flow StatementRavi RajputBelum ada peringkat

- Chapter 9Dokumen9 halamanChapter 9Kristelle Joy Pascual100% (1)

- Ashok Leyland - Financial Analysis 2006-07Dokumen44 halamanAshok Leyland - Financial Analysis 2006-07Apoorv BajajBelum ada peringkat

- Solution Manual For Financial Accounting 6th Canadian Edition by LibbyDokumen29 halamanSolution Manual For Financial Accounting 6th Canadian Edition by Libbya84964899475% (4)

- Afm Module 3 - IDokumen26 halamanAfm Module 3 - IABOOBAKKERBelum ada peringkat

- FM GroupDokumen6 halamanFM GroupRekik SolomonBelum ada peringkat

- Assignment FAR 2Dokumen12 halamanAssignment FAR 2Aikal HakimBelum ada peringkat

- MB0045 - Mba 2 SemDokumen19 halamanMB0045 - Mba 2 SemacorneleoBelum ada peringkat

- 14 Misc. Topic (Theory)Dokumen4 halaman14 Misc. Topic (Theory)Aakshi SharmaBelum ada peringkat

- Company ReviewDokumen12 halamanCompany ReviewKharyle Vianca PullidoBelum ada peringkat

- FAR 4309 Investment in Debt Securities 2Dokumen6 halamanFAR 4309 Investment in Debt Securities 2ATHALIAH LUNA MERCADEJASBelum ada peringkat

- Solution Manual For Financial Accounting 8th Edition by LibbyDokumen32 halamanSolution Manual For Financial Accounting 8th Edition by Libbya849648994100% (1)

- Financial Management Mb0045Dokumen5 halamanFinancial Management Mb0045Anonymous UFaC3TyiBelum ada peringkat

- BSBFIA402 Assessment 1 VF FinanzasDokumen10 halamanBSBFIA402 Assessment 1 VF FinanzasLiliana Cañon GomezBelum ada peringkat

- Accounting of Life Insurance Companies: Prakash VDokumen4 halamanAccounting of Life Insurance Companies: Prakash VSaurav RaiBelum ada peringkat

- Faca ShristiDokumen11 halamanFaca Shristishristi BaglaBelum ada peringkat

- Master of Business Administration-MBA Semester 2 MB0045 - Financial ManagementDokumen9 halamanMaster of Business Administration-MBA Semester 2 MB0045 - Financial ManagementGunjan BanerjeeBelum ada peringkat

- ADV2Dokumen3 halamanADV2Rommel RoyceBelum ada peringkat

- File MB0045 Financial Management SolvedDokumen28 halamanFile MB0045 Financial Management SolvedSebastian TaraoBelum ada peringkat

- Understanding Mutual Fund AccountingDokumen6 halamanUnderstanding Mutual Fund AccountingSwati MishraBelum ada peringkat

- Functions/Objectives of Financial ManagementDokumen7 halamanFunctions/Objectives of Financial ManagementRahul WaniBelum ada peringkat

- BhavinDokumen8 halamanBhavinBhavin_Shah_8217Belum ada peringkat

- Accounting of Life Insurance CompaniesDokumen4 halamanAccounting of Life Insurance CompaniesAnish ThomasBelum ada peringkat

- Financial Management 2iu3hudihDokumen10 halamanFinancial Management 2iu3hudihNageshwar singhBelum ada peringkat

- UNIT - 3:financial Decision: Prepared &presented Associate Professor, Dept. of Commerce&BS, CUSBDokumen71 halamanUNIT - 3:financial Decision: Prepared &presented Associate Professor, Dept. of Commerce&BS, CUSBswethaBelum ada peringkat

- BF-2 Assignment 1Dokumen8 halamanBF-2 Assignment 1sabya.rathoreBelum ada peringkat

- MB0045 Financial Management: C C C CDokumen10 halamanMB0045 Financial Management: C C C CDinesh Reghunath RBelum ada peringkat

- Financial ManagementDokumen9 halamanFinancial ManagementGogineni sai spandanaBelum ada peringkat

- Group 1 Pranav Shukla Kunal Jha Navdeep Sangwan Mansi Bharadwaj Nainika NarulaDokumen42 halamanGroup 1 Pranav Shukla Kunal Jha Navdeep Sangwan Mansi Bharadwaj Nainika NarulaDarek LinonBelum ada peringkat

- Goal of Profit Maximization. Maximization of Profits Is Generally Regarded AsDokumen5 halamanGoal of Profit Maximization. Maximization of Profits Is Generally Regarded AsSmita PriyadarshiniBelum ada peringkat

- Midterm - Finman Bsrem - MarkverzolaDokumen2 halamanMidterm - Finman Bsrem - MarkverzolaMavin .VerzolaBelum ada peringkat

- Conceptual FrameworkDokumen5 halamanConceptual FrameworkElla CunananBelum ada peringkat

- Ma Assignment # 7Dokumen18 halamanMa Assignment # 7Aeron Paul AntonioBelum ada peringkat

- Solution Manual For Financial Accounting 10th by LibbyDokumen33 halamanSolution Manual For Financial Accounting 10th by LibbyJenifer Collins100% (38)

- Midterm Review Term 3 2011 - 2012Dokumen4 halamanMidterm Review Term 3 2011 - 2012Milles ManginsayBelum ada peringkat

- Functions of Accounting Department: 1. BookkeepingDokumen3 halamanFunctions of Accounting Department: 1. BookkeepingMadhusudhan TantriBelum ada peringkat

- Free Cash FlowDokumen31 halamanFree Cash FlowKaranvir GuptaBelum ada peringkat

- MFDokumen6 halamanMFJS Gowri NandiniBelum ada peringkat

- Libby Financial Accounting Chapter14Dokumen7 halamanLibby Financial Accounting Chapter14Jie Bo TiBelum ada peringkat

- Internship Report - 03 June 22Dokumen12 halamanInternship Report - 03 June 22Alina KujurBelum ada peringkat

- Introduction To Financial Accounting ProjectDokumen12 halamanIntroduction To Financial Accounting ProjectYannick HarveyBelum ada peringkat

- 2020 - PFRS For SEs NotesDokumen16 halaman2020 - PFRS For SEs NotesRodelLabor100% (1)

- ARTICLES OF PARTNERSHIP (Legal)Dokumen6 halamanARTICLES OF PARTNERSHIP (Legal)accounting probBelum ada peringkat

- RATIONALEDokumen2 halamanRATIONALEaccounting probBelum ada peringkat

- Joint Affidavit of Undertaking To Change NameDokumen1 halamanJoint Affidavit of Undertaking To Change Nameaccounting probBelum ada peringkat

- Articles of Partnership OF Lopez & Semblante CoDokumen4 halamanArticles of Partnership OF Lopez & Semblante Coaccounting probBelum ada peringkat

- Taxation Comprehensive Exam TosDokumen2 halamanTaxation Comprehensive Exam Tosaccounting probBelum ada peringkat

- ActivityDokumen1 halamanActivityaccounting probBelum ada peringkat

- Activity 1Dokumen1 halamanActivity 1accounting probBelum ada peringkat

- Managementdeci SI Ontools: R R R RDokumen29 halamanManagementdeci SI Ontools: R R R Raccounting probBelum ada peringkat

- Advanced Financial Accounting and ReportingDokumen5 halamanAdvanced Financial Accounting and Reportingaccounting prob100% (1)

- Projected Annual DemandDokumen3 halamanProjected Annual Demandaccounting probBelum ada peringkat

- A Proposed Study of Production of Polyester Fabric From Waste Plastic BottlesDokumen2 halamanA Proposed Study of Production of Polyester Fabric From Waste Plastic Bottlesaccounting probBelum ada peringkat

- Basic Accounting Quiz Part 2Dokumen3 halamanBasic Accounting Quiz Part 2accounting probBelum ada peringkat

- Semblante, Rhea Angelica D. Bsa 2 1-2 MWF January 20, 2017: BibliographiesDokumen2 halamanSemblante, Rhea Angelica D. Bsa 2 1-2 MWF January 20, 2017: Bibliographiesaccounting probBelum ada peringkat

- Axa PhilippinesDokumen3 halamanAxa Philippinesaccounting probBelum ada peringkat

- Adjusting Entry QuizDokumen3 halamanAdjusting Entry Quizaccounting probBelum ada peringkat

- Quiz BowlDokumen2 halamanQuiz Bowlaccounting probBelum ada peringkat

- Quizbowl With Answer KeyDokumen3 halamanQuizbowl With Answer Keyaccounting probBelum ada peringkat

- DocumentDokumen12 halamanDocumentaccounting probBelum ada peringkat

- The Original Buko PieDokumen3 halamanThe Original Buko Pieaccounting prob100% (2)

- Often Used in Developing New Systems - Sufficient To Details - Use Simple, User-Friendly Symbols (Unlike Flowcharts)Dokumen1 halamanOften Used in Developing New Systems - Sufficient To Details - Use Simple, User-Friendly Symbols (Unlike Flowcharts)accounting probBelum ada peringkat

- Assumption 5: Managers Need Only To Understand How To Use An Information SystemDokumen1 halamanAssumption 5: Managers Need Only To Understand How To Use An Information Systemaccounting probBelum ada peringkat

- Assumption 5: Managers Need Only To Understand How To Use An Information SystemDokumen4 halamanAssumption 5: Managers Need Only To Understand How To Use An Information Systemaccounting probBelum ada peringkat

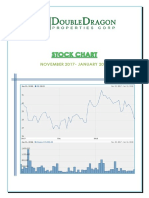

- Stock ChartDokumen1 halamanStock Chartaccounting probBelum ada peringkat

- Celltac MEK 6500Dokumen3 halamanCelltac MEK 6500RiduanBelum ada peringkat

- CASE 721F TIER 4 WHEEL LOADER Operator's Manual PDFDokumen17 halamanCASE 721F TIER 4 WHEEL LOADER Operator's Manual PDFfjskedmmsme0% (4)

- Periodontology Question BankDokumen44 halamanPeriodontology Question BankVanshika Jain100% (6)

- Educational Facility Planning: Bsarch V-2 Arch. Rey GabitanDokumen20 halamanEducational Facility Planning: Bsarch V-2 Arch. Rey Gabitanidealistic03Belum ada peringkat

- Water TreatmentDokumen13 halamanWater TreatmentBayuBelum ada peringkat

- UBKV Ranking Proforma With Annexures 2018 PDFDokumen53 halamanUBKV Ranking Proforma With Annexures 2018 PDFSubinay Saha RoyBelum ada peringkat

- Little Ann and Other Poems by Ann Taylor and Jane TaylorDokumen41 halamanLittle Ann and Other Poems by Ann Taylor and Jane Tayloralexa alexaBelum ada peringkat

- Electronic Over Current Relay (EOCR)Dokumen2 halamanElectronic Over Current Relay (EOCR)BambangsBelum ada peringkat

- Eko Serbia A.D. Beograd Rules For The Purchase of Fuel Through AccountsDokumen2 halamanEko Serbia A.D. Beograd Rules For The Purchase of Fuel Through AccountsMarko Perovic PerkeBelum ada peringkat

- Carbo Hi DratDokumen11 halamanCarbo Hi DratILHAM BAGUS DARMA .NBelum ada peringkat

- B737-800 Air ConditioningDokumen7 halamanB737-800 Air ConditioningReynaldoBelum ada peringkat

- 1 SMDokumen10 halaman1 SMAnindita GaluhBelum ada peringkat

- Insulating Oil TestingDokumen6 halamanInsulating Oil TestingnasrunBelum ada peringkat

- Containers HandbookDokumen26 halamanContainers Handbookrishi vohraBelum ada peringkat

- IWCF Comb. Supv Equip. 01Dokumen25 halamanIWCF Comb. Supv Equip. 01andrzema100% (3)

- طبى 145Dokumen2 halamanطبى 145Yazan AbuFarhaBelum ada peringkat

- Material: Safety Data SheetDokumen3 halamanMaterial: Safety Data SheetMichael JoudalBelum ada peringkat

- Oral Rehydration SolutionDokumen22 halamanOral Rehydration SolutionAlkaBelum ada peringkat

- R. Nishanth K. VigneswaranDokumen20 halamanR. Nishanth K. VigneswaranAbishaTeslinBelum ada peringkat

- DTC P1602 Deterioration of Battery: DescriptionDokumen5 halamanDTC P1602 Deterioration of Battery: DescriptionEdy SudarsonoBelum ada peringkat

- Content Map PE & Health 12Dokumen12 halamanContent Map PE & Health 12RIZZA MEA DOLOSOBelum ada peringkat

- Top 6 Beginner Work Out MistakesDokumen4 halamanTop 6 Beginner Work Out MistakesMARYAM GULBelum ada peringkat

- Chemistry DemosDokumen170 halamanChemistry DemosStacey BensonBelum ada peringkat

- Baxshin LABORATORY: Diagnostic Test and AnalysisDokumen1 halamanBaxshin LABORATORY: Diagnostic Test and AnalysisJabary HassanBelum ada peringkat

- 351 UN 1824 Sodium Hydroxide SolutionDokumen8 halaman351 UN 1824 Sodium Hydroxide SolutionCharls DeimoyBelum ada peringkat

- Meditran SX Sae 15w 40 API CH 4Dokumen1 halamanMeditran SX Sae 15w 40 API CH 4Aam HudsonBelum ada peringkat

- G.R. No. 94523 ST - Theresita's Academy vs. NLRCDokumen3 halamanG.R. No. 94523 ST - Theresita's Academy vs. NLRCyetyetBelum ada peringkat

- Intraocular Pressure and Aqueous Humor DynamicsDokumen36 halamanIntraocular Pressure and Aqueous Humor DynamicsIntan EkarulitaBelum ada peringkat

- Allison Weech Final ResumeDokumen1 halamanAllison Weech Final Resumeapi-506177291Belum ada peringkat

- Dif Stan 3-11-3Dokumen31 halamanDif Stan 3-11-3Tariq RamzanBelum ada peringkat

- The 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamDari EverandThe 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamBelum ada peringkat

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialDari EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialBelum ada peringkat

- The Value of a Whale: On the Illusions of Green CapitalismDari EverandThe Value of a Whale: On the Illusions of Green CapitalismPenilaian: 5 dari 5 bintang5/5 (2)

- These Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaDari EverandThese Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaPenilaian: 3.5 dari 5 bintang3.5/5 (8)

- John D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthDari EverandJohn D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthPenilaian: 4 dari 5 bintang4/5 (20)

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNDari Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNPenilaian: 4.5 dari 5 bintang4.5/5 (3)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaDari EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (14)

- Ready, Set, Growth hack:: A beginners guide to growth hacking successDari EverandReady, Set, Growth hack:: A beginners guide to growth hacking successPenilaian: 4.5 dari 5 bintang4.5/5 (93)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialDari EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialPenilaian: 4.5 dari 5 bintang4.5/5 (32)

- Creating Shareholder Value: A Guide For Managers And InvestorsDari EverandCreating Shareholder Value: A Guide For Managers And InvestorsPenilaian: 4.5 dari 5 bintang4.5/5 (8)

- An easy approach to trading with bollinger bands: How to learn how to use Bollinger bands to trade online successfullyDari EverandAn easy approach to trading with bollinger bands: How to learn how to use Bollinger bands to trade online successfullyPenilaian: 3 dari 5 bintang3/5 (1)

- Corporate Finance Formulas: A Simple IntroductionDari EverandCorporate Finance Formulas: A Simple IntroductionPenilaian: 4 dari 5 bintang4/5 (8)

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingDari EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingPenilaian: 4.5 dari 5 bintang4.5/5 (17)

- The Wall Street MBA, Third Edition: Your Personal Crash Course in Corporate FinanceDari EverandThe Wall Street MBA, Third Edition: Your Personal Crash Course in Corporate FinancePenilaian: 4 dari 5 bintang4/5 (1)

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisDari EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisPenilaian: 5 dari 5 bintang5/5 (6)

- Mastering the VC Game: A Venture Capital Insider Reveals How to Get from Start-up to IPO on Your TermsDari EverandMastering the VC Game: A Venture Capital Insider Reveals How to Get from Start-up to IPO on Your TermsPenilaian: 4.5 dari 5 bintang4.5/5 (21)

- Value: The Four Cornerstones of Corporate FinanceDari EverandValue: The Four Cornerstones of Corporate FinancePenilaian: 5 dari 5 bintang5/5 (2)

- Product-Led Growth: How to Build a Product That Sells ItselfDari EverandProduct-Led Growth: How to Build a Product That Sells ItselfPenilaian: 5 dari 5 bintang5/5 (1)

- Warren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorDari EverandWarren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorBelum ada peringkat

- Finance Basics (HBR 20-Minute Manager Series)Dari EverandFinance Basics (HBR 20-Minute Manager Series)Penilaian: 4.5 dari 5 bintang4.5/5 (32)

- Financial Leadership for Nonprofit Executives: Guiding Your Organization to Long-Term SuccessDari EverandFinancial Leadership for Nonprofit Executives: Guiding Your Organization to Long-Term SuccessPenilaian: 4 dari 5 bintang4/5 (2)

- Mind over Money: The Psychology of Money and How to Use It BetterDari EverandMind over Money: The Psychology of Money and How to Use It BetterPenilaian: 4 dari 5 bintang4/5 (24)

- YouTube Marketing: Comprehensive Beginners Guide to Learn YouTube Marketing, Tips & Secrets to Growth Hacking Your Channel and Building Profitable Passive Income Business OnlineDari EverandYouTube Marketing: Comprehensive Beginners Guide to Learn YouTube Marketing, Tips & Secrets to Growth Hacking Your Channel and Building Profitable Passive Income Business OnlinePenilaian: 4.5 dari 5 bintang4.5/5 (2)

- The Illusion of Innovation: Escape "Efficiency" and Unleash Radical ProgressDari EverandThe Illusion of Innovation: Escape "Efficiency" and Unleash Radical ProgressBelum ada peringkat