Anda mungkin juga menyukai

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

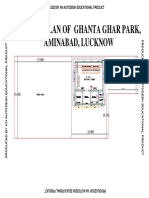

- Layout Plan of Ghanta Ghar Park, Aminabad, Lucknow: Produced by An Autodesk Educational ProductDokumen1 halamanLayout Plan of Ghanta Ghar Park, Aminabad, Lucknow: Produced by An Autodesk Educational ProductAnshuman PandeyBelum ada peringkat

- 26.51200 N 1 6 5 Gps Coordinates For Plantation in Bahru Forest AreaDokumen1 halaman26.51200 N 1 6 5 Gps Coordinates For Plantation in Bahru Forest AreaAnshuman PandeyBelum ada peringkat

- Railway EstimateDokumen2 halamanRailway EstimateAnshuman PandeyBelum ada peringkat

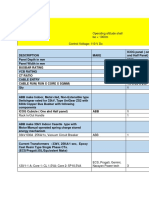

- Est Cable Trench - 900x1100Dokumen3 halamanEst Cable Trench - 900x1100Anshuman PandeyBelum ada peringkat

- Price List of Isi Hdpe Pipes: KELVIN BRAND HDPE PIPE IS:4984:1995, PE-63 (RS/MTR)Dokumen1 halamanPrice List of Isi Hdpe Pipes: KELVIN BRAND HDPE PIPE IS:4984:1995, PE-63 (RS/MTR)Anshuman Pandey100% (1)

- 33 KV IocgDokumen2 halaman33 KV IocgAnshuman PandeyBelum ada peringkat

- Data Sheet 630kva 33kv Cu F 90 Ip23Dokumen2 halamanData Sheet 630kva 33kv Cu F 90 Ip23Anshuman PandeyBelum ada peringkat

- 33 KV VCBDokumen3 halaman33 KV VCBAnshuman PandeyBelum ada peringkat

- 33 KV Bus GantryDokumen1 halaman33 KV Bus GantryAnshuman PandeyBelum ada peringkat

- 33 KV La & IsolatorDokumen1 halaman33 KV La & IsolatorAnshuman PandeyBelum ada peringkat

- CostDataBook2016 pdf3162016123929PMDokumen60 halamanCostDataBook2016 pdf3162016123929PMAnshuman Pandey100% (1)

- L3 LTI SystemsDokumen28 halamanL3 LTI SystemsAnshuman PandeyBelum ada peringkat

- UPPCS Prelims Exam 2013 General Studies Paper IIDokumen15 halamanUPPCS Prelims Exam 2013 General Studies Paper IIAnshuman PandeyBelum ada peringkat

- DWG Cable Trench - 850x800Dokumen1 halamanDWG Cable Trench - 850x800Anshuman PandeyBelum ada peringkat

- DWG Cable Trench - 850x800 PDFDokumen1 halamanDWG Cable Trench - 850x800 PDFAnshuman Pandey100% (1)

- Hindi Book-Himalaya-Ka-Yogi PDFDokumen428 halamanHindi Book-Himalaya-Ka-Yogi PDFAnshuman PandeyBelum ada peringkat

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (74)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- Master Fee AgreementDokumen5 halamanMaster Fee Agreementmeeshelz81450% (2)

- Assignment - Sources of CapitalDokumen14 halamanAssignment - Sources of Capitalabayomi abayomiBelum ada peringkat

- A View From The Trenches: Toronto, Sunday, May 5, 2013Dokumen8 halamanA View From The Trenches: Toronto, Sunday, May 5, 2013dan4everBelum ada peringkat

- Johnson & Johnson Deferred Prosecution AgreementDokumen38 halamanJohnson & Johnson Deferred Prosecution AgreementMike Koehler100% (1)

- AR Receivable Interview QuestionsDokumen5 halamanAR Receivable Interview QuestionsKrishna Victory100% (1)

- 2023 WSO IB Working Conditions SurveyDokumen46 halaman2023 WSO IB Working Conditions SurveyHaiyun ChenBelum ada peringkat

- EuroHedge Summit Brochure - April 2011Dokumen12 halamanEuroHedge Summit Brochure - April 2011Absolute ReturnBelum ada peringkat

- Quiz 1 AssuranceDokumen13 halamanQuiz 1 Assurancedarlenexjoyce100% (2)

- Aachi Spices and Foods Private Limited: Summary of Rated InstrumentDokumen6 halamanAachi Spices and Foods Private Limited: Summary of Rated Instrumentjaya_flareBelum ada peringkat

- Siemens Limited Annual Report 2013Dokumen95 halamanSiemens Limited Annual Report 2013Akshay UkeyBelum ada peringkat

- Case 35 Deluxe CorporationDokumen16 halamanCase 35 Deluxe CorporationSajjad Ahmad100% (1)

- NHPCDokumen418 halamanNHPCMohinish BhardwajBelum ada peringkat

- KKR Overview and Organizational SummaryDokumen73 halamanKKR Overview and Organizational SummaryRavi Chaurasia100% (3)

- Cusips: A Quick Guide For Issuers: The Official Source For Municipal Disclosures and Market DataDokumen12 halamanCusips: A Quick Guide For Issuers: The Official Source For Municipal Disclosures and Market Datajpes90% (10)

- 10 - Foreign Exchange Derivative MarketDokumen53 halaman10 - Foreign Exchange Derivative MarkethidaBelum ada peringkat

- Detailed Study On Hedging, Arbitrage and SpeculationDokumen247 halamanDetailed Study On Hedging, Arbitrage and SpeculationSumit NamdevBelum ada peringkat

- Customer Awareness Regarding Systematic Investment PlanDokumen37 halamanCustomer Awareness Regarding Systematic Investment PlanRaja kamal ChBelum ada peringkat

- Finance HWMDokumen5 halamanFinance HWMmobinil1Belum ada peringkat

- Beechy 7e Tif Ch09Dokumen20 halamanBeechy 7e Tif Ch09mashta04Belum ada peringkat

- TOPA (NOTES For Exam) PDFDokumen67 halamanTOPA (NOTES For Exam) PDFVivekBelum ada peringkat

- chemicals:-: Submitted To Dr. Pankaj K.Aggarwal Group-3 Section - D Submitted byDokumen6 halamanchemicals:-: Submitted To Dr. Pankaj K.Aggarwal Group-3 Section - D Submitted byAnonymous cXj9QhssBelum ada peringkat

- Strategic Alliance Development Corporation vs. Star Infrastructure Development Corporation Et Al. G.R. No. 187872 November 17, 2010 FactsDokumen7 halamanStrategic Alliance Development Corporation vs. Star Infrastructure Development Corporation Et Al. G.R. No. 187872 November 17, 2010 Factswmovies18Belum ada peringkat

- BIR Ruling DA-C-133 431-08Dokumen5 halamanBIR Ruling DA-C-133 431-08Lee Anne YabutBelum ada peringkat

- Mutual FundsDokumen34 halamanMutual FundsAmit PasiBelum ada peringkat

- Stock Exchange of IndiaDokumen23 halamanStock Exchange of IndiaAnirudh UbhanBelum ada peringkat

- Aui2601 Exam Pack 2016 1Dokumen57 halamanAui2601 Exam Pack 2016 1ricara alexia moodleyBelum ada peringkat

- Bab 6 Audit Responsibilities and ObjectivesDokumen6 halamanBab 6 Audit Responsibilities and ObjectivesAnonymous k7laSZOa0Belum ada peringkat

- Commodity AssignmentDokumen7 halamanCommodity Assignment05550Belum ada peringkat

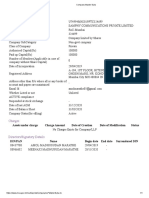

- Ministry of Corporate Affairs - MCA ServicesDokumen1 halamanMinistry of Corporate Affairs - MCA ServicesPranay ChauguleBelum ada peringkat