Anda mungkin juga menyukai

- By Bakampa Brian Baryaguma : Real Property, 5 Ed, Stevens & Sons LTD, p.913)Dokumen11 halamanBy Bakampa Brian Baryaguma : Real Property, 5 Ed, Stevens & Sons LTD, p.913)Real TrekstarBelum ada peringkat

- Statement of Financial PositionDokumen24 halamanStatement of Financial Positionheart lelim73% (11)

- Investment Leadership and Portfolio Management: The Path to Successful Stewardship for Investment FirmsDari EverandInvestment Leadership and Portfolio Management: The Path to Successful Stewardship for Investment FirmsBelum ada peringkat

- Charles Wild Smith and Keenans Company Law, 14th Edition PDFDokumen609 halamanCharles Wild Smith and Keenans Company Law, 14th Edition PDFFehmida ZafarBelum ada peringkat

- Closing the Gap: A Model for Commercial UnderwritingDari EverandClosing the Gap: A Model for Commercial UnderwritingBelum ada peringkat

- The 401(K) Owner’S Manual: Preparing Participants, Protecting FiduciariesDari EverandThe 401(K) Owner’S Manual: Preparing Participants, Protecting FiduciariesBelum ada peringkat

- FIN 3138 - Credit and Collection - SyllabusDokumen9 halamanFIN 3138 - Credit and Collection - SyllabusLorey Joy Idong100% (6)

- Real Estate AppraiserDokumen2 halamanReal Estate Appraiserapi-77241843Belum ada peringkat

- Security Analysis and Portfolio Management Mba Project Report PDFDokumen31 halamanSecurity Analysis and Portfolio Management Mba Project Report PDFvishnupriya0% (1)

- 2009 CFA Level 1 Mock Exam MorningDokumen38 halaman2009 CFA Level 1 Mock Exam MorningForrest100% (1)

- Buy or Lease - Mas ReportDokumen24 halamanBuy or Lease - Mas ReportEvangeline WongBelum ada peringkat

- Capital Structure Decisions: Evaluating Risk and UncertaintyDari EverandCapital Structure Decisions: Evaluating Risk and UncertaintyBelum ada peringkat

- Mutual Funds in India: Structure, Performance and UndercurrentsDari EverandMutual Funds in India: Structure, Performance and UndercurrentsBelum ada peringkat

- Coaching Senior Hires: Transitioning Potential Into Performance Quickly!Dari EverandCoaching Senior Hires: Transitioning Potential Into Performance Quickly!Belum ada peringkat

- Summer Internship of MBA in WEALTH MANAGEMENTDokumen74 halamanSummer Internship of MBA in WEALTH MANAGEMENTvarun100% (9)

- Comparative Study of Various Alternatives Available in The Market For Wealth Management PDFDokumen68 halamanComparative Study of Various Alternatives Available in The Market For Wealth Management PDFHenal Jhaveri100% (1)

- Financial ManagementDokumen86 halamanFinancial ManagementSanjeev SoniBelum ada peringkat

- Funds Flow AnalysisDokumen105 halamanFunds Flow AnalysisAmjad Khan100% (2)

- Show Me the Money: How to Determine ROI in People, Projects, and ProgramsDari EverandShow Me the Money: How to Determine ROI in People, Projects, and ProgramsPenilaian: 4 dari 5 bintang4/5 (13)

- Agile and Business Analysis: Practical guidance for IT professionalsDari EverandAgile and Business Analysis: Practical guidance for IT professionalsBelum ada peringkat

- The Drive of Business: Strategies for Creating Business AnglesDari EverandThe Drive of Business: Strategies for Creating Business AnglesBelum ada peringkat

- Divyanshi Project Report HRDokumen86 halamanDivyanshi Project Report HRNageshwar singh0% (1)

- Adopting Service Governance: Governing Portfolio Value for Sound Corporate CitzenshipDari EverandAdopting Service Governance: Governing Portfolio Value for Sound Corporate CitzenshipBelum ada peringkat

- Management SOPDokumen12 halamanManagement SOPsparkle shresthaBelum ada peringkat

- Project On Mutual Fund Akhilesh MishraDokumen142 halamanProject On Mutual Fund Akhilesh Mishramishra.akhilesh459737983% (262)

- AXIS-BANKWealth-management - EDIT G9Dokumen119 halamanAXIS-BANKWealth-management - EDIT G9AnupBelum ada peringkat

- Balram Project Report NN PDFDokumen70 halamanBalram Project Report NN PDFnageshwar singhBelum ada peringkat

- Deepak SoniDokumen71 halamanDeepak SoniPoonam MahendruBelum ada peringkat

- Final Report Sakshi Bhotmange 18A2HP404 PDFDokumen38 halamanFinal Report Sakshi Bhotmange 18A2HP404 PDFSakshi BhotmangeBelum ada peringkat

- Karvy ReportDokumen51 halamanKarvy ReportAbhishek rajBelum ada peringkat

- Divyanshi Project Report HR 1Dokumen85 halamanDivyanshi Project Report HR 1nageshwar singhBelum ada peringkat

- Project Report Nishant SharmaDokumen59 halamanProject Report Nishant SharmaSubham PandeyBelum ada peringkat

- "Mutual Funds Is The Better Investments Plan": Master of Business AdmimistrationDokumen142 halaman"Mutual Funds Is The Better Investments Plan": Master of Business AdmimistrationM Deva RajuBelum ada peringkat

- Standerd Charted BankDokumen118 halamanStanderd Charted BanktosifjaibunBelum ada peringkat

- Project Report: "Study On Portfolio Management Services Strategies and Investors Awareness and Prefrence For It"Dokumen49 halamanProject Report: "Study On Portfolio Management Services Strategies and Investors Awareness and Prefrence For It"Nitesh BaglaBelum ada peringkat

- Mohammed Meraj Ul Haq TaquiDokumen60 halamanMohammed Meraj Ul Haq TaquiAmit KapoorBelum ada peringkat

- KarvyDokumen81 halamanKarvyAmit86% (7)

- Title of ProjectDokumen86 halamanTitle of ProjectSanjeev SoniBelum ada peringkat

- Project On Mutual FundDokumen142 halamanProject On Mutual Fundpriyanshu singhBelum ada peringkat

- Maharshi Arvind KailashDokumen141 halamanMaharshi Arvind Kailashrahulsogani123Belum ada peringkat

- Project On Portfolio Management 456Dokumen47 halamanProject On Portfolio Management 456Danish NaqviBelum ada peringkat

- Customer Perception Towards Mutual FundsDokumen80 halamanCustomer Perception Towards Mutual Fundsbharat sachdevaBelum ada peringkat

- Role of Potentially Mutual Funds BusinessDokumen85 halamanRole of Potentially Mutual Funds BusinessAKSHIT INDULKARBelum ada peringkat

- Axis Mutual Fund Project ReportDokumen37 halamanAxis Mutual Fund Project ReportVikas PabaleBelum ada peringkat

- A Project Report On "Analysis of Mutual Funds Schemes": KARVY Stock Broking LTDDokumen46 halamanA Project Report On "Analysis of Mutual Funds Schemes": KARVY Stock Broking LTDSnigdha SinghBelum ada peringkat

- A Summer Training Project On Study of Customer Satisfaction Toward The Product and Services in Axis BankDokumen45 halamanA Summer Training Project On Study of Customer Satisfaction Toward The Product and Services in Axis BankDoru HaagiBelum ada peringkat

- BBA-MBA Integrated (2020-25) Final Report of The Summer Internship Aditya Birla CapitalDokumen12 halamanBBA-MBA Integrated (2020-25) Final Report of The Summer Internship Aditya Birla CapitalRishitBelum ada peringkat

- VishnuDokumen76 halamanVishnuVishnu MantriBelum ada peringkat

- Kuldeep FinalDokumen94 halamanKuldeep FinalSHIVAM BHARDWAJBelum ada peringkat

- Final Project MIL LuckyI123456Dokumen77 halamanFinal Project MIL LuckyI123456mili98Belum ada peringkat

- HDFC SecuritiesDokumen85 halamanHDFC Securitiessuncancerian100% (1)

- Academic Qualification: Male, 26 Years - B.E - M.B.ADokumen1 halamanAcademic Qualification: Male, 26 Years - B.E - M.B.ARajgopal BalabhadruniBelum ada peringkat

- A Study On: Analiysis of Systematic Investment Plan Mutual FundsDokumen73 halamanA Study On: Analiysis of Systematic Investment Plan Mutual FundsNunna Baskar100% (1)

- Snehal Project FinalDokumen63 halamanSnehal Project Finalravi kangneBelum ada peringkat

- Parasram HoldingsDokumen67 halamanParasram HoldingsPunit BhalvalBelum ada peringkat

- 360 Degree Financial Planning (Bajaj Capital LTD)Dokumen47 halaman360 Degree Financial Planning (Bajaj Capital LTD)Asin Ganguly100% (1)

- Venture Capital FinalDokumen69 halamanVenture Capital Finalviraj gadhiyaBelum ada peringkat

- Becoming A Strategic Business Leader: The Ultimate All-In-One ToolkitDari EverandBecoming A Strategic Business Leader: The Ultimate All-In-One ToolkitBelum ada peringkat

- Gateway Framework: A Governance Approach for Infrastructure Investment SustainabilityDari EverandGateway Framework: A Governance Approach for Infrastructure Investment SustainabilityBelum ada peringkat

- Small and Medium Enterprises’ Trend and Its Impact Towards Hrd: A Critical EvaluationDari EverandSmall and Medium Enterprises’ Trend and Its Impact Towards Hrd: A Critical EvaluationBelum ada peringkat

- Bid & Proposal Management Using AI: Winning Proposals From RFP’s to a Winning SolutionDari EverandBid & Proposal Management Using AI: Winning Proposals From RFP’s to a Winning SolutionBelum ada peringkat

- Investing for Better: Harnessing the Four Driving Forces of Asset Management to Build a Wealthier and More Equitable WorldDari EverandInvesting for Better: Harnessing the Four Driving Forces of Asset Management to Build a Wealthier and More Equitable WorldBelum ada peringkat

- PayslipDokumen1 halamanPayslipprathmeshBelum ada peringkat

- Pefindo'S Corporate Default and Rating Transition Study (1996 - 2010)Dokumen21 halamanPefindo'S Corporate Default and Rating Transition Study (1996 - 2010)Theo VladimirBelum ada peringkat

- Fintelum Opens Investment Into New Tokenisation Project KEEPPDokumen3 halamanFintelum Opens Investment Into New Tokenisation Project KEEPPPR.comBelum ada peringkat

- Core - 6 - Cash & Liquidity ManagementDokumen55 halamanCore - 6 - Cash & Liquidity ManagementShailjaBelum ada peringkat

- Question #1 of 25Dokumen15 halamanQuestion #1 of 25ALL ROUNDBelum ada peringkat

- Cross Country Comparison of Efficiency in Investment BankingDokumen26 halamanCross Country Comparison of Efficiency in Investment Bankingnehanazare15Belum ada peringkat

- RE - BOQ of Chilli IIDokumen17 halamanRE - BOQ of Chilli IIAnonymous AV90SAXa5VBelum ada peringkat

- Appendix I Specimen of Advice of Maturity Date To Term Deposit Account HoldersDokumen11 halamanAppendix I Specimen of Advice of Maturity Date To Term Deposit Account HoldersRuchi SharmaBelum ada peringkat

- EPS Bootstrapping Bootstrap Earnings e EctDokumen2 halamanEPS Bootstrapping Bootstrap Earnings e Ecthyba ben helalBelum ada peringkat

- LESSON 8 - Purpose of BanksDokumen5 halamanLESSON 8 - Purpose of BanksChirag HablaniBelum ada peringkat

- Evp6310009992783 - 2020 01 01 - 2021 09 16Dokumen184 halamanEvp6310009992783 - 2020 01 01 - 2021 09 16tunisiehyperBelum ada peringkat

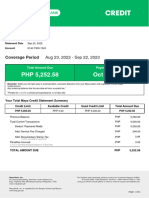

- MayaCredit SoA 2023SEPDokumen3 halamanMayaCredit SoA 2023SEPjepoy palaruanBelum ada peringkat

- Psak 72 10 Minutes PDFDokumen2 halamanPsak 72 10 Minutes PDFMentari AndiniBelum ada peringkat

- Entrepreneurship Simulation The Startup Game - Wharton University of PennsylvaniaDokumen46 halamanEntrepreneurship Simulation The Startup Game - Wharton University of PennsylvaniaMetin ReyhanogluBelum ada peringkat

- Accounting Standard 1Dokumen27 halamanAccounting Standard 1Sid2875% (4)

- Madhuban Bapudham SchemeDokumen3 halamanMadhuban Bapudham SchemerahulBelum ada peringkat

- Group 2 Section B PDFDokumen33 halamanGroup 2 Section B PDFShaikh Saifullah KhalidBelum ada peringkat

- Book4time 25.06.2020 PDFDokumen1 halamanBook4time 25.06.2020 PDFCira ShotadzeBelum ada peringkat

- 24.4 SebiDokumen30 halaman24.4 SebijashuramuBelum ada peringkat

- 1BRNEA2022002Dokumen64 halaman1BRNEA2022002Nguyễn Xuân ThượngBelum ada peringkat