Anda mungkin juga menyukai

- Ipology: The Science of the Initial Public OfferingDari EverandIpology: The Science of the Initial Public OfferingPenilaian: 5 dari 5 bintang5/5 (1)

- Grow Business External Resources Franchising Joint VenturesDokumen25 halamanGrow Business External Resources Franchising Joint Venturesshmaim tansenBelum ada peringkat

- MGT368.4 - L15 (1-Slide Per Page)Dokumen24 halamanMGT368.4 - L15 (1-Slide Per Page)Shamim TansenBelum ada peringkat

- Initial Public Offerings (Ipos)Dokumen15 halamanInitial Public Offerings (Ipos)Nitisha SinghBelum ada peringkat

- Initial Public OfferDokumen31 halamanInitial Public OfferfhhvBelum ada peringkat

- Stock Exchange Listing Mechanism On Main Board, SME Exchange & ITP (Institutional Trading Platform)Dokumen39 halamanStock Exchange Listing Mechanism On Main Board, SME Exchange & ITP (Institutional Trading Platform)Pranav KhannaBelum ada peringkat

- Informal Risk and Venture CapitalDokumen15 halamanInformal Risk and Venture CapitalZoofi ShanBelum ada peringkat

- IPO / Listing Planning: Affan Sajjad - ACADokumen35 halamanIPO / Listing Planning: Affan Sajjad - ACAKhalid MahmoodBelum ada peringkat

- IPO PreparationDokumen4 halamanIPO Preparationdeshmukh_muzammil1917Belum ada peringkat

- Understanding the IPO ProcessDokumen17 halamanUnderstanding the IPO ProcessAbhilash GehlotBelum ada peringkat

- Initial Public Offerings (Ipos)Dokumen19 halamanInitial Public Offerings (Ipos)Shaikh TausifBelum ada peringkat

- 1 Corporate Finance IntroductionDokumen41 halaman1 Corporate Finance IntroductionPooja KaulBelum ada peringkat

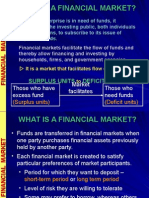

- What Is A Financial Market?Dokumen42 halamanWhat Is A Financial Market?Foram ChhedaBelum ada peringkat

- Presentation - Lahore (Final) 4th March 2011 PDFDokumen52 halamanPresentation - Lahore (Final) 4th March 2011 PDFsweetkanwal61Belum ada peringkat

- Corporate Finance - IntroDokumen21 halamanCorporate Finance - IntroNiharika AgarwalBelum ada peringkat

- Venture Capital FinancingDokumen41 halamanVenture Capital FinancingRíshãbh JåíñBelum ada peringkat

- Restaurant Feasibility StudyDokumen55 halamanRestaurant Feasibility StudyAdarsh ShrivastavaBelum ada peringkat

- Raising Long Term FinanceDokumen34 halamanRaising Long Term FinanceTiya AmuBelum ada peringkat

- Chapter 12 Informal Risk Capital Venture Capital and Going PublicDokumen43 halamanChapter 12 Informal Risk Capital Venture Capital and Going Publicmkahnum12Belum ada peringkat

- Chapter 12 Professional Venture CapitalDokumen26 halamanChapter 12 Professional Venture CapitalTrang TranBelum ada peringkat

- Informal Risk Capital & Venture CapitalDokumen18 halamanInformal Risk Capital & Venture CapitalsmaparnaBelum ada peringkat

- EP EXTRADokumen7 halamanEP EXTRAIsha ChughBelum ada peringkat

- Why ASHVA Qualifies for PPO Based on Regulations and Cost SavingsDokumen13 halamanWhy ASHVA Qualifies for PPO Based on Regulations and Cost SavingsKaran SoniBelum ada peringkat

- Involvement of Parties During Issuing of AnDokumen9 halamanInvolvement of Parties During Issuing of Anvimalprakash55Belum ada peringkat

- Merchant BankingDokumen6 halamanMerchant BankingRenu SimranBelum ada peringkat

- IPO Process: Listing NormsDokumen16 halamanIPO Process: Listing NormsraghuchanderjointBelum ada peringkat

- Venture Capital 101Dokumen20 halamanVenture Capital 101jhmedvedBelum ada peringkat

- Primary Market FunctionsDokumen24 halamanPrimary Market FunctionsdanbrowndaBelum ada peringkat

- Regulation Equity Crowdfunding - FinalDokumen24 halamanRegulation Equity Crowdfunding - FinalCasey BarachBelum ada peringkat

- Securities Market: Dr. Rana Singh 9811828987Dokumen52 halamanSecurities Market: Dr. Rana Singh 9811828987Biswabhusan PradhanBelum ada peringkat

- FS Mod 7Dokumen35 halamanFS Mod 7sonaBelum ada peringkat

- Chapter 4 - Fund ManagementDokumen38 halamanChapter 4 - Fund Managementngannguyen.31221024512Belum ada peringkat

- Long-Term Financing in MalaysiaDokumen20 halamanLong-Term Financing in MalaysiaNurhikma Kurnia IsmailBelum ada peringkat

- Unit 3 Primary MarketDokumen29 halamanUnit 3 Primary MarkettiwariaradBelum ada peringkat

- The Initial Public Offering (Ipo)Dokumen38 halamanThe Initial Public Offering (Ipo)Onur YamukBelum ada peringkat

- Due DiligenceDokumen35 halamanDue DiligenceViplav HarmalkarBelum ada peringkat

- Baf 361 Introduction To Corporate Finance and Banking: Lecture 2-Financial Planning and Raising of FundsDokumen28 halamanBaf 361 Introduction To Corporate Finance and Banking: Lecture 2-Financial Planning and Raising of FundsRevivalist Arthur - GeomanBelum ada peringkat

- Basic Listing Requirements EquitiesDokumen5 halamanBasic Listing Requirements EquitiesHasina Binte HasanBelum ada peringkat

- Investment Banking: Presentation OnDokumen56 halamanInvestment Banking: Presentation OnPradeep BandiBelum ada peringkat

- VC FundsDokumen42 halamanVC FundsJogendra BeheraBelum ada peringkat

- Registration With SEBI As Merchant Banker and Other MaterialDokumen5 halamanRegistration With SEBI As Merchant Banker and Other Materialapi-3727090100% (3)

- Fund Raising & Overview of IPO: Sharing NTPC ExperienceDokumen38 halamanFund Raising & Overview of IPO: Sharing NTPC ExperienceSamBelum ada peringkat

- Venture CapitalDokumen105 halamanVenture CapitalDhruti BhatiaBelum ada peringkat

- Sources of Capital, Informal Risk Capital & Venture CapitalDokumen29 halamanSources of Capital, Informal Risk Capital & Venture CapitalDivyesh Gandhi0% (1)

- VC & Managing GrowthDokumen51 halamanVC & Managing GrowthSarvar PathanBelum ada peringkat

- Caiib Fmmodbacs Nov08Dokumen91 halamanCaiib Fmmodbacs Nov08monirba48Belum ada peringkat

- CAIIB-Financial Management-Module B Study of Financial StatementsDokumen91 halamanCAIIB-Financial Management-Module B Study of Financial StatementsDeepak RathoreBelum ada peringkat

- Entrepreneurship Chapter 12 - Informal Risk CapitalDokumen3 halamanEntrepreneurship Chapter 12 - Informal Risk CapitalSoledad Perez75% (4)

- Chapter 23BBDokumen27 halamanChapter 23BBTaVuKieuNhi100% (1)

- IPO & Its RequirmentsDokumen38 halamanIPO & Its RequirmentsAnuj GosaiBelum ada peringkat

- Financial System Assignment 3Dokumen7 halamanFinancial System Assignment 3Pooja GyawaliBelum ada peringkat

- Module 8: Understanding Financial Statements and Evaluating Investment OpportunitiesDokumen43 halamanModule 8: Understanding Financial Statements and Evaluating Investment Opportunitiesrandyblanza2014Belum ada peringkat

- M& A PDFDokumen78 halamanM& A PDFDevesh MauryaBelum ada peringkat

- Study of Financial StatementsDokumen39 halamanStudy of Financial Statementsagrawalrohit_228384Belum ada peringkat

- Chap12 MbaDokumen40 halamanChap12 MbaMehar Sheikh100% (1)

- Chapter 01 Long-Term Investing and Financial DecisionsDokumen30 halamanChapter 01 Long-Term Investing and Financial DecisionsdungphuongngoBelum ada peringkat

- Primary and Secondary MarketDokumen57 halamanPrimary and Secondary MarketRahul Shakya100% (1)

- Listing of SecuritiesDokumen18 halamanListing of SecuritiesSaurabh SumanBelum ada peringkat

- Question #3Dokumen1 halamanQuestion #3Shamim TansenBelum ada peringkat

- Chap 5 Identifying and Analyzing Domestic and International OpportunitiesDokumen33 halamanChap 5 Identifying and Analyzing Domestic and International Opportunitiesanilyram100% (1)

- Sabu HalaDokumen3 halamanSabu HalaShamim TansenBelum ada peringkat

- Jaf 154Dokumen5 halamanJaf 154Shamim Tansen100% (1)

- Sabu HalaDokumen3 halamanSabu HalaShamim TansenBelum ada peringkat

- MGT368.4 - L11 (1-Slide Per Page)Dokumen28 halamanMGT368.4 - L11 (1-Slide Per Page)Shamim TansenBelum ada peringkat

- Shamim Loyalty QusDokumen1 halamanShamim Loyalty QusShamim TansenBelum ada peringkat

- 1Dokumen1 halaman1Shamim TansenBelum ada peringkat

- BibliographyDokumen1 halamanBibliographyShamim TansenBelum ada peringkat

- Law 2Dokumen11 halamanLaw 2Shamim TansenBelum ada peringkat

- Question #3Dokumen1 halamanQuestion #3Shamim TansenBelum ada peringkat

- 1Dokumen1 halaman1Shamim TansenBelum ada peringkat

- Case StudyDokumen22 halamanCase StudyAbhishek SoniBelum ada peringkat

- Sample Real Estate Letter of IntentDokumen3 halamanSample Real Estate Letter of Intentanon_650868240100% (3)

- BPI V IACDokumen5 halamanBPI V IACjon_macasaetBelum ada peringkat

- Airline CodesDokumen26 halamanAirline CodesSavita PooniaBelum ada peringkat

- Profit and Loss AccountDokumen1 halamanProfit and Loss AccountmuazzampkBelum ada peringkat

- Trinidad and Tobaggo Corruption Ballah ReportDokumen132 halamanTrinidad and Tobaggo Corruption Ballah Reportsylodhi100% (1)

- Training and Development of Biman Bangladesh AirlineDokumen27 halamanTraining and Development of Biman Bangladesh AirlineSAEID RAHMAN100% (3)

- Corpo 6Dokumen2 halamanCorpo 6KLBelum ada peringkat

- Managing Interdependence: Social Responsibility and Ethics ch02Dokumen21 halamanManaging Interdependence: Social Responsibility and Ethics ch02diversified1Belum ada peringkat

- Wilmington - North Riverfront Marina and Hotel Park Riverwalk Swap Land DealDokumen51 halamanWilmington - North Riverfront Marina and Hotel Park Riverwalk Swap Land DealMichael D KaneBelum ada peringkat

- Signing Agreement for Loan Against SharesDokumen7 halamanSigning Agreement for Loan Against SharesAshish BangurBelum ada peringkat

- Budgeting CTRLDokumen9 halamanBudgeting CTRLJoseph PamaongBelum ada peringkat

- 200M HakaDokumen15 halaman200M HakaWinengku100% (4)

- Practice Test 1 KeyDokumen11 halamanPractice Test 1 KeyAshley Storey100% (1)

- A Study of Impacts of Merger & Acquisition on Financial Performance of Indian Banking SectorDokumen163 halamanA Study of Impacts of Merger & Acquisition on Financial Performance of Indian Banking Sectorpatel243180% (10)

- BYEJOE Teaser FinalDokumen2 halamanBYEJOE Teaser FinalMayur BhoyarBelum ada peringkat

- Report Part 2 ProblemDokumen49 halamanReport Part 2 ProblemMd Khaled NoorBelum ada peringkat

- Disclose Act 2017 - One PagerDokumen1 halamanDisclose Act 2017 - One PagerMarkWarnerBelum ada peringkat

- 11 Accountancy TP Ch04 01 Ladger and Trial BalanceDokumen3 halaman11 Accountancy TP Ch04 01 Ladger and Trial Balancerenu bhattBelum ada peringkat

- TDS Challan 06-05-18Dokumen1 halamanTDS Challan 06-05-18sandipgargBelum ada peringkat

- pp16Dokumen64 halamanpp16Mousami BanerjeeBelum ada peringkat

- United Bank of India ResultsDokumen31 halamanUnited Bank of India ResultsGolla Vishwanath YadavBelum ada peringkat

- Nasipit V NLRC SCRADokumen20 halamanNasipit V NLRC SCRARenz R.Belum ada peringkat

- Chapter 7 Grand StrategiesDokumen73 halamanChapter 7 Grand StrategiesFarhan Badakshani100% (3)

- It Parks Developers PezaDokumen38 halamanIt Parks Developers PezaCurtney Jane Bullecer BalagulanBelum ada peringkat

- CGTMSEDokumen21 halamanCGTMSEakashBelum ada peringkat

- Financial Study Notes RBI Grade B Phase IIDokumen35 halamanFinancial Study Notes RBI Grade B Phase IIKapil MittalBelum ada peringkat

- Johor Corp 2008Dokumen209 halamanJohor Corp 2008khairulkamarudinBelum ada peringkat

- Competition: Airbus and BoeingDokumen15 halamanCompetition: Airbus and BoeingHenry DunaBelum ada peringkat

- IFRS 5 Non-Current Assets Held For Sale and Discontinued OperationsDokumen36 halamanIFRS 5 Non-Current Assets Held For Sale and Discontinued OperationsMariana MirelaBelum ada peringkat

- Scary Smart: The Future of Artificial Intelligence and How You Can Save Our WorldDari EverandScary Smart: The Future of Artificial Intelligence and How You Can Save Our WorldPenilaian: 4.5 dari 5 bintang4.5/5 (54)

- The Bitcoin Standard: The Decentralized Alternative to Central BankingDari EverandThe Bitcoin Standard: The Decentralized Alternative to Central BankingPenilaian: 4.5 dari 5 bintang4.5/5 (41)

- Alibaba: The House That Jack Ma BuiltDari EverandAlibaba: The House That Jack Ma BuiltPenilaian: 3.5 dari 5 bintang3.5/5 (29)

- Mastering Large Language Models: Advanced techniques, applications, cutting-edge methods, and top LLMs (English Edition)Dari EverandMastering Large Language Models: Advanced techniques, applications, cutting-edge methods, and top LLMs (English Edition)Belum ada peringkat

- Dealers of Lightning: Xerox PARC and the Dawn of the Computer AgeDari EverandDealers of Lightning: Xerox PARC and the Dawn of the Computer AgePenilaian: 4 dari 5 bintang4/5 (88)

- Digital Gold: Bitcoin and the Inside Story of the Misfits and Millionaires Trying to Reinvent MoneyDari EverandDigital Gold: Bitcoin and the Inside Story of the Misfits and Millionaires Trying to Reinvent MoneyPenilaian: 4 dari 5 bintang4/5 (51)

- The Corporate Startup: How established companies can develop successful innovation ecosystemsDari EverandThe Corporate Startup: How established companies can develop successful innovation ecosystemsPenilaian: 4 dari 5 bintang4/5 (6)

- The Infinite Machine: How an Army of Crypto-Hackers Is Building the Next Internet with EthereumDari EverandThe Infinite Machine: How an Army of Crypto-Hackers Is Building the Next Internet with EthereumPenilaian: 3 dari 5 bintang3/5 (12)

- Artificial Intelligence: A Guide for Thinking HumansDari EverandArtificial Intelligence: A Guide for Thinking HumansPenilaian: 4.5 dari 5 bintang4.5/5 (30)

- Generative AI: The Insights You Need from Harvard Business ReviewDari EverandGenerative AI: The Insights You Need from Harvard Business ReviewPenilaian: 4.5 dari 5 bintang4.5/5 (2)

- AI Superpowers: China, Silicon Valley, and the New World OrderDari EverandAI Superpowers: China, Silicon Valley, and the New World OrderPenilaian: 4.5 dari 5 bintang4.5/5 (398)

- The Master Algorithm: How the Quest for the Ultimate Learning Machine Will Remake Our WorldDari EverandThe Master Algorithm: How the Quest for the Ultimate Learning Machine Will Remake Our WorldPenilaian: 4.5 dari 5 bintang4.5/5 (107)

- Blood, Sweat, and Pixels: The Triumphant, Turbulent Stories Behind How Video Games Are MadeDari EverandBlood, Sweat, and Pixels: The Triumphant, Turbulent Stories Behind How Video Games Are MadePenilaian: 4.5 dari 5 bintang4.5/5 (335)

- How to Do Nothing: Resisting the Attention EconomyDari EverandHow to Do Nothing: Resisting the Attention EconomyPenilaian: 4 dari 5 bintang4/5 (421)

- Who's Afraid of AI?: Fear and Promise in the Age of Thinking MachinesDari EverandWho's Afraid of AI?: Fear and Promise in the Age of Thinking MachinesPenilaian: 4.5 dari 5 bintang4.5/5 (12)

- Make Money with ChatGPT: Your Guide to Making Passive Income Online with Ease using AI: AI Wealth MasteryDari EverandMake Money with ChatGPT: Your Guide to Making Passive Income Online with Ease using AI: AI Wealth MasteryBelum ada peringkat

- Seo: The Ultimate Search Engine Optimization Guide for Marketers and EntrepreneursDari EverandSeo: The Ultimate Search Engine Optimization Guide for Marketers and EntrepreneursPenilaian: 4.5 dari 5 bintang4.5/5 (121)

- AI Money Machine: Unlock the Secrets to Making Money Online with AIDari EverandAI Money Machine: Unlock the Secrets to Making Money Online with AIBelum ada peringkat

- Data-ism: The Revolution Transforming Decision Making, Consumer Behavior, and Almost Everything ElseDari EverandData-ism: The Revolution Transforming Decision Making, Consumer Behavior, and Almost Everything ElsePenilaian: 3.5 dari 5 bintang3.5/5 (12)

- Artificial Intelligence: The Insights You Need from Harvard Business ReviewDari EverandArtificial Intelligence: The Insights You Need from Harvard Business ReviewPenilaian: 4.5 dari 5 bintang4.5/5 (104)

- Build: An Unorthodox Guide to Making Things Worth MakingDari EverandBuild: An Unorthodox Guide to Making Things Worth MakingPenilaian: 5 dari 5 bintang5/5 (121)

- The E-Myth Revisited: Why Most Small Businesses Don't Work andDari EverandThe E-Myth Revisited: Why Most Small Businesses Don't Work andPenilaian: 4.5 dari 5 bintang4.5/5 (707)

- Eric Ries’ The Lean Startup How Today's Entrepreneurs Use Continuous Innovation to Create Radically Successful Businesses SummaryDari EverandEric Ries’ The Lean Startup How Today's Entrepreneurs Use Continuous Innovation to Create Radically Successful Businesses SummaryPenilaian: 4.5 dari 5 bintang4.5/5 (11)

- 100+ Amazing AI Image Prompts: Expertly Crafted Midjourney AI Art Generation ExamplesDari Everand100+ Amazing AI Image Prompts: Expertly Crafted Midjourney AI Art Generation ExamplesBelum ada peringkat