Anda mungkin juga menyukai

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (399)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- ACCA AAA MJ19 Notes PDFDokumen156 halamanACCA AAA MJ19 Notes PDFOmer ZaheerBelum ada peringkat

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (73)

- The Atlas of Economic Indicators PDFDokumen123 halamanThe Atlas of Economic Indicators PDFswinki383% (6)

- Accounting for Derivatives and Hedging ActivitiesDokumen22 halamanAccounting for Derivatives and Hedging Activitiesswinki3Belum ada peringkat

- Lehman Brothers: Guide To Exotic Credit DerivativesDokumen60 halamanLehman Brothers: Guide To Exotic Credit DerivativesCrodoleBelum ada peringkat

- Bare Metal CPPDokumen199 halamanBare Metal CPPswinki3Belum ada peringkat

- Positional TradingDokumen69 halamanPositional TradingManoj Kumar0% (2)

- Ted Baker RedactedDokumen65 halamanTed Baker RedactedWaqar HassanBelum ada peringkat

- Convexity BiasDokumen26 halamanConvexity Biasswinki3Belum ada peringkat

- 1-LLIVAN - Alliance Lite 2-MDokumen15 halaman1-LLIVAN - Alliance Lite 2-Mveldanez100% (6)

- Tuca-Calibration of LMM - Comparison Between Separated and Approximated ApproachDokumen52 halamanTuca-Calibration of LMM - Comparison Between Separated and Approximated Approachswinki3Belum ada peringkat

- Calculating Convexity Adjustment for Interest Rates Using Martingale TheoryDokumen18 halamanCalculating Convexity Adjustment for Interest Rates Using Martingale Theoryswinki3Belum ada peringkat

- Tu-Is Regime Switching in Stock Returns Important in Portfolio DecisionsDokumen46 halamanTu-Is Regime Switching in Stock Returns Important in Portfolio Decisionsswinki3Belum ada peringkat

- How To Create An Operating SystemDokumen36 halamanHow To Create An Operating Systemecartman2100% (1)

- Shinada-Actual Factors To Determine Cross-Currency Basis Swaps An Empirical Study On US Dollar-Japanese Yen Basis Swap Rates From The Late 1990sDokumen14 halamanShinada-Actual Factors To Determine Cross-Currency Basis Swaps An Empirical Study On US Dollar-Japanese Yen Basis Swap Rates From The Late 1990sswinki3Belum ada peringkat

- Bonds Analysis ValuationDokumen52 halamanBonds Analysis Valuationswinki3Belum ada peringkat

- Major Challenges in Collateral ManagementDokumen22 halamanMajor Challenges in Collateral Managementswinki3Belum ada peringkat

- CPP Best PracticesDokumen45 halamanCPP Best Practicesswinki3Belum ada peringkat

- ISDA Section 10 Overview of Derivatives TechnologyDokumen35 halamanISDA Section 10 Overview of Derivatives Technologyswinki3Belum ada peringkat

- JPMorgan DerivativesDokumen55 halamanJPMorgan Derivativesswinki3Belum ada peringkat

- ISDA Section 03 Interest Rate and Currency DerivativesDokumen82 halamanISDA Section 03 Interest Rate and Currency Derivativesswinki3Belum ada peringkat

- ISDA Section 11 Hand NotesDokumen7 halamanISDA Section 11 Hand Notesswinki3Belum ada peringkat

- ISDA Section 08 Rate Sets and SettlementsDokumen21 halamanISDA Section 08 Rate Sets and Settlementsswinki3Belum ada peringkat

- Equity Derivatives OverviewDokumen15 halamanEquity Derivatives Overviewswinki3Belum ada peringkat

- ISDA Section 07 Trade CaptureDokumen14 halamanISDA Section 07 Trade Captureswinki3Belum ada peringkat

- ISDA Section 05 Swaps Global OperationsDokumen7 halamanISDA Section 05 Swaps Global Operationsswinki3Belum ada peringkat

- 2005 ISDA Conference Overview of Pay-As-YouDokumen5 halaman2005 ISDA Conference Overview of Pay-As-Youswinki3Belum ada peringkat

- ISDA Section 00 Table of ContentsDokumen3 halamanISDA Section 00 Table of Contentsswinki3Belum ada peringkat

- ISDA Section 04 Valuing Unwinding and Hedging SwapsDokumen81 halamanISDA Section 04 Valuing Unwinding and Hedging Swapsswinki3Belum ada peringkat

- ISDA Section 02 AgendaDokumen11 halamanISDA Section 02 Agendaswinki3Belum ada peringkat

- ISDA 2000 Board of DirectorsDokumen37 halamanISDA 2000 Board of Directorsswinki3Belum ada peringkat

- ISDA Conference On Structured Products CDSDokumen15 halamanISDA Conference On Structured Products CDSswinki3Belum ada peringkat

- 2005 ISDA Conference NovationsDokumen3 halaman2005 ISDA Conference Novationsswinki3Belum ada peringkat

- 2005 ISDA Conference Prime Brokerage As TheDokumen4 halaman2005 ISDA Conference Prime Brokerage As Theswinki3Belum ada peringkat

- 2005 ISDA Conference Netting and CollateralDokumen13 halaman2005 ISDA Conference Netting and Collateralswinki3Belum ada peringkat

- JPM Asia Pacific Equity 2011-07-07 624664Dokumen22 halamanJPM Asia Pacific Equity 2011-07-07 624664tommyphyuBelum ada peringkat

- 861 EvidenceDokumen5 halaman861 Evidencelegalmatters100% (1)

- Press Release: Arwade Infrastructure Limited D-U-N-S® Number: 86-414-9519Dokumen4 halamanPress Release: Arwade Infrastructure Limited D-U-N-S® Number: 86-414-9519Ravi BabuBelum ada peringkat

- A Brief History of BankingDokumen42 halamanA Brief History of Bankingtasaduq70% (1)

- RevenueDokumen105 halamanRevenueanbugobiBelum ada peringkat

- 3 Accounting Cycle UDDokumen13 halaman3 Accounting Cycle UDERICK MLINGWABelum ada peringkat

- Audit Risk FactorsDokumen4 halamanAudit Risk Factorsmariko1234Belum ada peringkat

- 2Dokumen3 halaman2Ruth TenajerosBelum ada peringkat

- La Demanda Contra Loma NegraDokumen30 halamanLa Demanda Contra Loma NegraGuillermo Pereira PoizónBelum ada peringkat

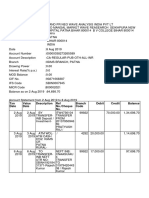

- TXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceDokumen3 halamanTXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceNishi GuptaBelum ada peringkat

- BISMACDokumen2 halamanBISMACCharles Mclin TejeroBelum ada peringkat

- Diminishing MusharakahDokumen45 halamanDiminishing MusharakahIbn Bashir Ar-Raisi0% (1)

- F 4506Dokumen2 halamanF 4506kittie_86Belum ada peringkat

- CLEANSING PROCESS FOR DIVIDENDS AND GAINSDokumen2 halamanCLEANSING PROCESS FOR DIVIDENDS AND GAINSAbdul Aziz MuhammadBelum ada peringkat

- MAS-06 Operational BudgetingDokumen7 halamanMAS-06 Operational BudgetingKrizza MaeBelum ada peringkat

- ProjectDokumen79 halamanProjectvishwajit bhoir100% (1)

- MCWQS For All XamsDokumen97 halamanMCWQS For All Xamsvini_anj3980Belum ada peringkat

- BWN JC 110112 (Init)Dokumen28 halamanBWN JC 110112 (Init)Ana WesselBelum ada peringkat

- FORM 10-K: United States Securities and Exchange CommissionDokumen55 halamanFORM 10-K: United States Securities and Exchange CommissionJerome PadillaBelum ada peringkat

- New Form No 15GDokumen4 halamanNew Form No 15GDevang PatelBelum ada peringkat

- Philippine Legal Guide - Tax Case Digest - CIR v. Isabela Cultural Corp. (2007)Dokumen3 halamanPhilippine Legal Guide - Tax Case Digest - CIR v. Isabela Cultural Corp. (2007)Fymgem AlbertoBelum ada peringkat

- Epicor ERP 10 Malaysia Country Specific Functionality Guide 10.0.700Dokumen30 halamanEpicor ERP 10 Malaysia Country Specific Functionality Guide 10.0.700nerz8830Belum ada peringkat

- HCI 2007 Prelim H2 P2 QN PaperDokumen2 halamanHCI 2007 Prelim H2 P2 QN PaperFang Wen LimBelum ada peringkat

- I FHMHFMDokumen1 halamanI FHMHFMRaghuraman NarasimmaluBelum ada peringkat

- Invoice Artech010723 Artech Alliance Owners Association Artech RealtorsDokumen2 halamanInvoice Artech010723 Artech Alliance Owners Association Artech RealtorsPrasad SBelum ada peringkat

- Importance of TaxDokumen6 halamanImportance of Taxmahabalu123456789Belum ada peringkat