Anda mungkin juga menyukai

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

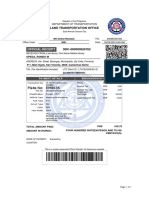

- Plate No: EM8635: Official ReceiptDokumen1 halamanPlate No: EM8635: Official ReceiptRomie Opeda67% (3)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (73)

- Celcom JanDokumen2 halamanCelcom JanThee Suh ShyanBelum ada peringkat

- THURONYI, Victor. Comparative Tax LawDokumen400 halamanTHURONYI, Victor. Comparative Tax LawChristiano Valente100% (1)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- View StatementDokumen2 halamanView StatementMarissa MBelum ada peringkat

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- On January 1 Pulse Recording Studio Prs Had The FollowingDokumen1 halamanOn January 1 Pulse Recording Studio Prs Had The FollowingLet's Talk With HassanBelum ada peringkat

- CoronaDokumen1 halamanCoronaAnoop MbBelum ada peringkat

- New Text DocumentDokumen10 halamanNew Text DocumentAnoop MbBelum ada peringkat

- Structural DynamicsDokumen4 halamanStructural DynamicsAnoop MbBelum ada peringkat

- New Text DocumentDokumen7 halamanNew Text DocumentAnoop MbBelum ada peringkat

- HygroDokumen4 halamanHygroAnoop MbBelum ada peringkat

- PaulDokumen1 halamanPaulAnoop MbBelum ada peringkat

- New Text DocumentDokumen4 halamanNew Text DocumentAnoop MbBelum ada peringkat

- ModalDokumen2 halamanModalAnoop MbBelum ada peringkat

- NonDokumen10 halamanNonAnoop MbBelum ada peringkat

- AdhesionDokumen7 halamanAdhesionAnoop MbBelum ada peringkat

- WedgeDokumen3 halamanWedgeAnoop MbBelum ada peringkat

- Concurrent EngineeringDokumen3 halamanConcurrent EngineeringAnoop MbBelum ada peringkat

- TrussDokumen7 halamanTrussAnoop MbBelum ada peringkat

- DiffractionDokumen10 halamanDiffractionAnoop MbBelum ada peringkat

- New Text DocumentDokumen4 halamanNew Text DocumentAnoop MbBelum ada peringkat

- FrictionDokumen12 halamanFrictionAnoop MbBelum ada peringkat

- Spark IgnitionDokumen9 halamanSpark IgnitionAnoop MbBelum ada peringkat

- New Text DocumentDokumen4 halamanNew Text DocumentAnoop MbBelum ada peringkat

- Bit CoinDokumen12 halamanBit CoinAnoop MbBelum ada peringkat

- Differential EquationDokumen7 halamanDifferential EquationAnoop MbBelum ada peringkat

- New Text DocumentDokumen14 halamanNew Text DocumentAnoop MbBelum ada peringkat

- New Text DocumentDokumen9 halamanNew Text DocumentAnoop MbBelum ada peringkat

- New Text DocumentDokumen4 halamanNew Text DocumentAnoop MbBelum ada peringkat

- CurrencyDokumen5 halamanCurrencyAnoop Mb0% (1)

- EngineDokumen11 halamanEngineAnoop MbBelum ada peringkat

- Sentance ArrangementDokumen43 halamanSentance ArrangementRabendraSharmaBelum ada peringkat

- EngineDokumen11 halamanEngineAnoop MbBelum ada peringkat

- HeatDokumen8 halamanHeatAnoop MbBelum ada peringkat

- PercentageDokumen16 halamanPercentageSindhu GunaBelum ada peringkat

- Vat Form 100Dokumen10 halamanVat Form 100Shoaib4804174Belum ada peringkat

- Gcash Transaction History: Date and Time Description Reference No. Debit Credit BalanceDokumen3 halamanGcash Transaction History: Date and Time Description Reference No. Debit Credit BalanceJessica CraveBelum ada peringkat

- ABM11 BussMath Q2 Wk4 Taxable-And-Nontaxable-BenefitsDokumen11 halamanABM11 BussMath Q2 Wk4 Taxable-And-Nontaxable-BenefitsArchimedes Arvie Garcia0% (1)

- Leoncio BIR CounterDokumen4 halamanLeoncio BIR CounterGerald HernandezBelum ada peringkat

- TFW Application Forms NEW - 20210809102815Dokumen5 halamanTFW Application Forms NEW - 20210809102815doney PhilipBelum ada peringkat

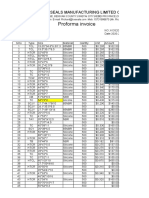

- Proforma Invoice: Xingtai Baixin Seals Manufacturing Limited CompayDokumen6 halamanProforma Invoice: Xingtai Baixin Seals Manufacturing Limited CompayMohammed Albadre AghilBelum ada peringkat

- Sample: Annual Escrow Account Statement Sample ONLYDokumen2 halamanSample: Annual Escrow Account Statement Sample ONLYjohnbombomBelum ada peringkat

- Ayesha SajjadDokumen1 halamanAyesha SajjadPak FFBelum ada peringkat

- InvoiceDokumen2 halamanInvoiceqwrhhemBelum ada peringkat

- Padasalai Ifhrms ManualDokumen14 halamanPadasalai Ifhrms ManualSivakumar MurugesanBelum ada peringkat

- 22 06 2023 - External Fund Transfer - AllDokumen17 halaman22 06 2023 - External Fund Transfer - Allmeliodas dragonBelum ada peringkat

- Hero 22734BD23V227Dokumen2 halamanHero 22734BD23V227hariBelum ada peringkat

- I 1065Dokumen55 halamanI 1065Monique ScottBelum ada peringkat

- PIONEER Current Account SOB Eff 1st Dec 2022Dokumen2 halamanPIONEER Current Account SOB Eff 1st Dec 2022Rajat AgarwalBelum ada peringkat

- Book A Cruise - Bruce Anchor CruisesDokumen2 halamanBook A Cruise - Bruce Anchor Cruisesjatin bholaBelum ada peringkat

- выписка месяцDokumen3 halamanвыписка месяцeskanderzunisbaevBelum ada peringkat

- Fs 2223Dokumen18 halamanFs 2223NIA ATALINBelum ada peringkat

- Tax 2 Reviewer Atty. Bolivar NotesDokumen66 halamanTax 2 Reviewer Atty. Bolivar NotesMaree BajamundeBelum ada peringkat

- In GMSDokumen1 halamanIn GMStarun.kushBelum ada peringkat

- Rulings2000 DigestDokumen21 halamanRulings2000 DigestArriane MartinezBelum ada peringkat

- 484b6 Impact Wrong Type of Tax Paid and Wrong Claim of ItcDokumen5 halaman484b6 Impact Wrong Type of Tax Paid and Wrong Claim of Itc15211 alok AnandBelum ada peringkat

- Appendix 32 BrgyDokumen4 halamanAppendix 32 BrgyJovelyn SeseBelum ada peringkat

- TERM PAPER of TaxationDokumen25 halamanTERM PAPER of TaxationBobasa S AhmedBelum ada peringkat

- Sales Tax Act, 1990Dokumen1 halamanSales Tax Act, 1990Talib HussainBelum ada peringkat

- Leases 2Dokumen3 halamanLeases 2John Patrick Lazaro Andres100% (1)