Anda mungkin juga menyukai

- Special Power of AttorneyDokumen3 halamanSpecial Power of AttorneypatriziaannfBelum ada peringkat

- Extrajudicial Settlement of Estate Rule 74, Section 1 ChecklistDokumen8 halamanExtrajudicial Settlement of Estate Rule 74, Section 1 ChecklistMsyang Ann Corbo DiazBelum ada peringkat

- Lecture 3 - Income Taxation (Corporate)Dokumen8 halamanLecture 3 - Income Taxation (Corporate)Lovenia Magpatoc50% (2)

- Halsbury's STAMP DUTIES AND STAMP DUTY RESERVE TAX (VOLUME 44Dokumen564 halamanHalsbury's STAMP DUTIES AND STAMP DUTY RESERVE TAX (VOLUME 44Minister100% (1)

- How To Process Land Transfer in The PhilippinesDokumen9 halamanHow To Process Land Transfer in The PhilippinesRonald O.Belum ada peringkat

- Documentary Stamp Tax - Bureau of Internal RevenueDokumen12 halamanDocumentary Stamp Tax - Bureau of Internal RevenueJenny Amante-BesasBelum ada peringkat

- Corporate Income TaxationDokumen39 halamanCorporate Income TaxationVinz G. VizBelum ada peringkat

- Full Assignment Tax RPGTDokumen19 halamanFull Assignment Tax RPGTVasant SriudomBelum ada peringkat

- Establishing A Business in PortugalDokumen30 halamanEstablishing A Business in Portugaldaniel francoBelum ada peringkat

- Cir VS Traders Royal BankDokumen4 halamanCir VS Traders Royal BankGLORILYN MONTEJOBelum ada peringkat

- Contract To SellDokumen2 halamanContract To SellPaolo Gabriel Sid Decena100% (2)

- Advanced Zimbabwe Tax Module 2011 PDFDokumen125 halamanAdvanced Zimbabwe Tax Module 2011 PDFCosmas Takawira88% (24)

- Facts:: H. Tambunting Pawnshop, Inc. v. Commissioner of Internal RevenueDokumen1 halamanFacts:: H. Tambunting Pawnshop, Inc. v. Commissioner of Internal RevenueKriselBelum ada peringkat

- Tax Planning - Intro NotesDokumen7 halamanTax Planning - Intro NotesBest How To StudioBelum ada peringkat

- Thailand Corporate Income TaxDokumen31 halamanThailand Corporate Income TaxPrincessJoyGinezFlorentinBelum ada peringkat

- Japan Tax Profile: Produced in Conjunction With The KPMG Asia Pacific Tax CentreDokumen15 halamanJapan Tax Profile: Produced in Conjunction With The KPMG Asia Pacific Tax CentreKris MehtaBelum ada peringkat

- Corporate Income Taxes and Tax RatesDokumen38 halamanCorporate Income Taxes and Tax RatesShaheen ShahBelum ada peringkat

- 05 Corporate Tax Planning and ManagementDokumen34 halaman05 Corporate Tax Planning and ManagementHimanshu SharmaBelum ada peringkat

- International Tax: India Highlights 2018Dokumen7 halamanInternational Tax: India Highlights 2018Prince VamsiBelum ada peringkat

- Taxation ProjectDokumen14 halamanTaxation ProjectrahulkoduvanBelum ada peringkat

- KPMG - Indonesian TaxDokumen13 halamanKPMG - Indonesian Taxbang bebetBelum ada peringkat

- Chapter 3. CITDokumen57 halamanChapter 3. CITKhuất Thanh HuếBelum ada peringkat

- The Philippines Income TaxDokumen8 halamanThe Philippines Income TaxmendozaivanrichmondBelum ada peringkat

- Hari Income Tax Department - Do CXDokumen12 halamanHari Income Tax Department - Do CXNelluri Surendhar ChowdaryBelum ada peringkat

- Corporate Tax: Residency of CompaniesDokumen2 halamanCorporate Tax: Residency of CompaniesLimpho Teddy PhateBelum ada peringkat

- India Tax Profile: Produced in Conjunction With The KPMG Asia Pacific Tax CentreDokumen24 halamanIndia Tax Profile: Produced in Conjunction With The KPMG Asia Pacific Tax CentreUday MunjalBelum ada peringkat

- Heads of IncomeDokumen6 halamanHeads of Incomevijay kumarBelum ada peringkat

- Business Tax in Viet NamDokumen3 halamanBusiness Tax in Viet NamLinh ĐỗBelum ada peringkat

- Vaishnavi ProjectDokumen72 halamanVaishnavi ProjectAkshada DhapareBelum ada peringkat

- Assignment On Corporate Taxation in BangladeshDokumen9 halamanAssignment On Corporate Taxation in Bangladeshsalekin0070% (1)

- Sri Lanka 2018 PDFDokumen24 halamanSri Lanka 2018 PDFSoofi AthamBelum ada peringkat

- TaxDokumen11 halamanTaxmnoor13245mnBelum ada peringkat

- Direct Tax CodeDokumen8 halamanDirect Tax CodeImran HassanBelum ada peringkat

- Income Taxation Finals - CompressDokumen9 halamanIncome Taxation Finals - CompressElaiza RegaladoBelum ada peringkat

- Indian Taxation SystemDokumen15 halamanIndian Taxation SystemassatputeBelum ada peringkat

- TaxationDokumen3 halamanTaxationErwin MacaspacBelum ada peringkat

- International Tax: India Highlights 2019Dokumen8 halamanInternational Tax: India Highlights 2019AbcdBelum ada peringkat

- Summary of Thailand-Tax-Guide and LawsDokumen34 halamanSummary of Thailand-Tax-Guide and LawsPranav BhatBelum ada peringkat

- Value Added Tax Black Book 2 2332Dokumen47 halamanValue Added Tax Black Book 2 2332sanket yelaweBelum ada peringkat

- KoreaDokumen21 halamanKoreaChimgeeChmgeBelum ada peringkat

- CS Professional Programme Tax NotesDokumen47 halamanCS Professional Programme Tax NotesRajey Jain100% (2)

- Corporate Taxation in BangladeshDokumen8 halamanCorporate Taxation in Bangladeshskn092Belum ada peringkat

- BASICS OF TAXATION (Income Tax Ordinance, 1984) Updated Till Finance Act. 2013 by Prof. Mahbubur RahmanDokumen14 halamanBASICS OF TAXATION (Income Tax Ordinance, 1984) Updated Till Finance Act. 2013 by Prof. Mahbubur RahmansaadmansheedyBelum ada peringkat

- DTTL Tax Bangladeshhighlights 2023Dokumen10 halamanDTTL Tax Bangladeshhighlights 2023steveBelum ada peringkat

- Basic Concept of Income TaxDokumen4 halamanBasic Concept of Income TaxNaurah Atika DinaBelum ada peringkat

- Philippines Tax RatesDokumen7 halamanPhilippines Tax RatesJL GEN0% (1)

- Deloitte Tax Alert - Corporate Tax Rates Slashed and Fiscal Relief AnnouncedDokumen4 halamanDeloitte Tax Alert - Corporate Tax Rates Slashed and Fiscal Relief AnnouncedSunil GidwaniBelum ada peringkat

- TaxationDokumen10 halamanTaxationIshika ChauhanBelum ada peringkat

- Taxation System in IndiaDokumen5 halamanTaxation System in IndiaSiddharth NagarBelum ada peringkat

- MODULE 6 PREFERENTIAL TAX RATES of CORPORATIONSDokumen9 halamanMODULE 6 PREFERENTIAL TAX RATES of CORPORATIONSangclaire47Belum ada peringkat

- Philippines Income Tax RatesDokumen6 halamanPhilippines Income Tax RatesKristina AngelieBelum ada peringkat

- Individual Income TaxDokumen2 halamanIndividual Income TaxpojjaneeBelum ada peringkat

- MCIT ReportDokumen13 halamanMCIT ReportfebwinBelum ada peringkat

- U 5 TaxDokumen23 halamanU 5 TaxfsafwfBelum ada peringkat

- Business Tax Laws in The PhilippinesDokumen12 halamanBusiness Tax Laws in The PhilippinesEthel Joi Manalac MendozaBelum ada peringkat

- Inward 22Dokumen44 halamanInward 22CSBBelum ada peringkat

- Corporate Taxes in The PhilippinesDokumen2 halamanCorporate Taxes in The PhilippinesAike SadjailBelum ada peringkat

- India Tax SystemDokumen53 halamanIndia Tax SystemNiket DattaniBelum ada peringkat

- Income Tax in IndiaDokumen19 halamanIncome Tax in IndiaConcepts TreeBelum ada peringkat

- TaxDokumen6 halamanTaxKhánh LinhBelum ada peringkat

- Taxation System in IndiaDokumen35 halamanTaxation System in IndiaSaif UddinBelum ada peringkat

- Philippine Corporate TaxDokumen3 halamanPhilippine Corporate TaxRaymond FaeldoñaBelum ada peringkat

- Income Tax Note 02Dokumen4 halamanIncome Tax Note 02Hashani Anuttara AbeygunasekaraBelum ada peringkat

- Minimum Corporate Income TAXDokumen12 halamanMinimum Corporate Income TAXAra Bianca InofreBelum ada peringkat

- Chapter 5 - Final Income TaxationDokumen13 halamanChapter 5 - Final Income TaxationBisag AsaBelum ada peringkat

- Business Tax Laws (Phils)Dokumen15 halamanBusiness Tax Laws (Phils)Jean TanBelum ada peringkat

- Taxation System in IndiaDokumen30 halamanTaxation System in IndiaSwapnil Pisal-DeshmukhBelum ada peringkat

- Module 1: Income Tax PrinciplesDokumen18 halamanModule 1: Income Tax PrinciplesJun MagallonBelum ada peringkat

- Philippines Tax RatesDokumen7 halamanPhilippines Tax RatesRonel CacheroBelum ada peringkat

- Categories of Income and Tax RatesDokumen5 halamanCategories of Income and Tax RatesRonel CacheroBelum ada peringkat

- Share Gift Transfer 2Dokumen2 halamanShare Gift Transfer 2陳宣芳Belum ada peringkat

- Contract To Sell: (Note: Terms and Conditions Below Are Sample Only, Please Revise)Dokumen4 halamanContract To Sell: (Note: Terms and Conditions Below Are Sample Only, Please Revise)Charlene Gevela AndreoBelum ada peringkat

- Pre-Exam Marathon 3 - House Property, Capital Gains, IFOS, Salaries, PGBP, TDS, TCS, Advance Tax, PDFDokumen106 halamanPre-Exam Marathon 3 - House Property, Capital Gains, IFOS, Salaries, PGBP, TDS, TCS, Advance Tax, PDFParmeet NainBelum ada peringkat

- TAXATION - Full Text FinalsDokumen24 halamanTAXATION - Full Text FinalsJanine CastroBelum ada peringkat

- E Auction Process Document - Tender DocumentDokumen32 halamanE Auction Process Document - Tender DocumentKalyan YogBelum ada peringkat

- Bir Ruling Da 288 2005Dokumen4 halamanBir Ruling Da 288 2005Eunice SaavedraBelum ada peringkat

- Taxation in EthiopiaDokumen50 halamanTaxation in Ethiopiastrength, courage, and wisdom92% (12)

- PMK 242-03-2014 (English)Dokumen49 halamanPMK 242-03-2014 (English)Irka PlayingBelum ada peringkat

- Digitally Signed by DS ZERODHA 3 Date: 2018.04.16 23:23:22 IST Reason: "Regulatory" Location: "Zerodha, Bangalore"Dokumen4 halamanDigitally Signed by DS ZERODHA 3 Date: 2018.04.16 23:23:22 IST Reason: "Regulatory" Location: "Zerodha, Bangalore"Lokesh NABelum ada peringkat

- Investment Validation Guidelines 2020-1 PDFDokumen7 halamanInvestment Validation Guidelines 2020-1 PDFravi kumarBelum ada peringkat

- The Problems of Leasing in IndiaDokumen2 halamanThe Problems of Leasing in Indialyf of GhaganBelum ada peringkat

- Topic:-Direct and Indirect Taxes: Department of Electronics & Telecommunication EngineeringDokumen15 halamanTopic:-Direct and Indirect Taxes: Department of Electronics & Telecommunication EngineeringSakshi DewadeBelum ada peringkat

- 1.3registering Property Mumbai EoDBDokumen16 halaman1.3registering Property Mumbai EoDBgaaneshmujumdarBelum ada peringkat

- 136 - Doing Business in ERITREADokumen5 halaman136 - Doing Business in ERITREAEvan ComenBelum ada peringkat

- Types of TaxesDokumen3 halamanTypes of TaxesKynaat MirzaBelum ada peringkat

- Division "A" Section - A: Date:21.09.2020Dokumen16 halamanDivision "A" Section - A: Date:21.09.2020harsh jainBelum ada peringkat

- Karnataka Stamp Act As Amended in 2012 of 34 of 1957 (E)Dokumen111 halamanKarnataka Stamp Act As Amended in 2012 of 34 of 1957 (E)manunpBelum ada peringkat

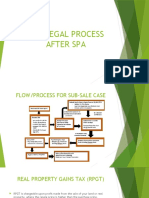

- The Legal Process After SpaDokumen16 halamanThe Legal Process After SpaIzat AmirBelum ada peringkat