Anda mungkin juga menyukai

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5795)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- GO2Bank Template 2Dokumen5 halamanGO2Bank Template 2Roger kelly71% (14)

- 4 Memorandum of AssociationDokumen38 halaman4 Memorandum of Associationkhuranaamanpreet7gmailcom100% (1)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- Plaintiff's Statement of Undisputed Facts To QLSDokumen8 halamanPlaintiff's Statement of Undisputed Facts To QLSLee PerryBelum ada peringkat

- Draft Resolution For Society-TrustDokumen2 halamanDraft Resolution For Society-Trustammaiappar0% (2)

- Account Tariff Structure Basic Savings AccountDokumen1 halamanAccount Tariff Structure Basic Savings Accountgaddipati_ramuBelum ada peringkat

- Amortization & Sinking FundDokumen27 halamanAmortization & Sinking FundkimBelum ada peringkat

- Employee Details Payment & Working Days Details Location Details Nitu SinghDokumen1 halamanEmployee Details Payment & Working Days Details Location Details Nitu SinghRohit raagBelum ada peringkat

- PDICDokumen1 halamanPDICShyrine EjemBelum ada peringkat

- Success Solutions Care: WelcomeDokumen7 halamanSuccess Solutions Care: Welcomekhuranaamanpreet7gmailcomBelum ada peringkat

- Solved Long Division Problems With Step-By-Step Walkthrough: Solutions Are On Page 2Dokumen2 halamanSolved Long Division Problems With Step-By-Step Walkthrough: Solutions Are On Page 2khuranaamanpreet7gmailcomBelum ada peringkat

- 1 To 10 (All Subjects) +1, +2 Commerce, Arts (All Subjects)Dokumen1 halaman1 To 10 (All Subjects) +1, +2 Commerce, Arts (All Subjects)khuranaamanpreet7gmailcomBelum ada peringkat

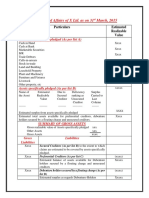

- Statement of AffairsDokumen2 halamanStatement of Affairskhuranaamanpreet7gmailcom100% (1)

- Statement of Affairs-1Dokumen5 halamanStatement of Affairs-1khuranaamanpreet7gmailcomBelum ada peringkat

- Holding and Subsidiary CompaniesDokumen33 halamanHolding and Subsidiary Companieskhuranaamanpreet7gmailcomBelum ada peringkat

- Amalgamantion and External ReconstructionDokumen67 halamanAmalgamantion and External Reconstructionkhuranaamanpreet7gmailcomBelum ada peringkat

- Shale Trading - Journal EntriesDokumen5 halamanShale Trading - Journal Entriessayali matkar100% (1)

- Simple and Compound Interest: Ryan Jeffrey P Curbano, PH.DDokumen35 halamanSimple and Compound Interest: Ryan Jeffrey P Curbano, PH.DPrince RiveraBelum ada peringkat

- Exercises (Time Value Money) 2022Dokumen2 halamanExercises (Time Value Money) 2022wstBelum ada peringkat

- Know Your CustomerDokumen9 halamanKnow Your CustomerSudip HatiBelum ada peringkat

- Credit Authorisation SchemeDokumen6 halamanCredit Authorisation SchemeOngwang KonyakBelum ada peringkat

- Pib ApplyDokumen1 halamanPib ApplykrishkpeBelum ada peringkat

- Challan PrintDokumen2 halamanChallan PrintshraddhaBelum ada peringkat

- Fin103 COPY SWIFTDokumen1 halamanFin103 COPY SWIFTbenzainvestcorporateBelum ada peringkat

- SAN CARLOS V Bpi - DigestDokumen1 halamanSAN CARLOS V Bpi - DigestMirabel VidalBelum ada peringkat

- Exim Bank - General Banking ActivitiesDokumen69 halamanExim Bank - General Banking ActivitiesRazon Tariqul IslamBelum ada peringkat

- IA Q2 BondsDokumen4 halamanIA Q2 BondsJennifer RasonabeBelum ada peringkat

- Inspection - SoDokumen44 halamanInspection - SoK V Sridharan General Secretary P3 NFPEBelum ada peringkat

- Acct Statement XX3567 28112023Dokumen80 halamanAcct Statement XX3567 28112023hareshpadhiyar4646Belum ada peringkat

- Gmail - Paper Acceptance Notification For Paper ID - IJISRT20AUG355Dokumen2 halamanGmail - Paper Acceptance Notification For Paper ID - IJISRT20AUG355Dialson PaulusBelum ada peringkat

- Solved When A College Student Complained About A Particular Course TheDokumen1 halamanSolved When A College Student Complained About A Particular Course TheAnbu jaromiaBelum ada peringkat

- Negotiable Instruments-Asanka KarunaratnaDokumen19 halamanNegotiable Instruments-Asanka KarunaratnaLahiru ChathurangaBelum ada peringkat

- NPA Recognition 12 Nov RBI CircularDokumen30 halamanNPA Recognition 12 Nov RBI CircularNarayani TripathiBelum ada peringkat

- Tax Invoice: TIN#: 1000145GST501Dokumen1 halamanTax Invoice: TIN#: 1000145GST501aishathBelum ada peringkat

- Pragathi Krishna Gramin BANKDokumen47 halamanPragathi Krishna Gramin BANKSachin Kumar Sakri100% (3)

- A Project Report OnDokumen86 halamanA Project Report OnDevangi PatelBelum ada peringkat

- Why Banks FailDokumen12 halamanWhy Banks FailpatrickBelum ada peringkat

- HLB BSDokumen6 halamanHLB BSanisBelum ada peringkat

- MORIGINADokumen7 halamanMORIGINAatishBelum ada peringkat