Anda mungkin juga menyukai

- The FCA As A Tool in Business LitigationDokumen19 halamanThe FCA As A Tool in Business LitigationJonathan TyckoBelum ada peringkat

- Harvin's Reply BriefDokumen18 halamanHarvin's Reply BriefAl HarvinBelum ada peringkat

- Rights of The AccusedDokumen5 halamanRights of The AccusedDianalyn QuitebesBelum ada peringkat

- Findings of Fact - ProsecutionDokumen9 halamanFindings of Fact - ProsecutionIndiana Public Media NewsBelum ada peringkat

- TX Supreme Court - Eviction OrderDokumen3 halamanTX Supreme Court - Eviction OrderMark SchnyderBelum ada peringkat

- MTD Foreclosure or Definite StatementDokumen5 halamanMTD Foreclosure or Definite Statementkleua9053Belum ada peringkat

- Foreclosure Defense Document Requests - Set 1 - 2017-03-10Dokumen8 halamanForeclosure Defense Document Requests - Set 1 - 2017-03-10AnonymousBelum ada peringkat

- Arsenal: Federal Rules of Civil Procedure: Rule 4 SummonsDokumen12 halamanArsenal: Federal Rules of Civil Procedure: Rule 4 SummonsDevon Rae YorkBelum ada peringkat

- Uber Fair Credit Class ActionDokumen20 halamanUber Fair Credit Class Actionjeff_roberts881Belum ada peringkat

- Class Action Complaint: Bandago v. Mercedes-Benz USADokumen35 halamanClass Action Complaint: Bandago v. Mercedes-Benz USAChrisCassidyBelum ada peringkat

- UNITED STATES OF AMERICA'S MOTION TO DISMISS APPEAL AND STAY BRIEFING SCHEDULEdd.242731.5.0Dokumen12 halamanUNITED STATES OF AMERICA'S MOTION TO DISMISS APPEAL AND STAY BRIEFING SCHEDULEdd.242731.5.0D B Karron, PhDBelum ada peringkat

- DHS v. New York Motion To Lift or Modify StayDokumen261 halamanDHS v. New York Motion To Lift or Modify StayWashington Free BeaconBelum ada peringkat

- Order Generic Justice Court FillableDokumen2 halamanOrder Generic Justice Court FillableAhtashamBelum ada peringkat

- U.S. v. Rosicki Complaint-In-Intervention 0Dokumen29 halamanU.S. v. Rosicki Complaint-In-Intervention 0TimesreviewBelum ada peringkat

- Stefanie Goldblatt, CFPB Senior Litigation Counsel Re Case 140304-000750Dokumen102 halamanStefanie Goldblatt, CFPB Senior Litigation Counsel Re Case 140304-000750Neil GillespieBelum ada peringkat

- Plaintiff's Response To Motion To Strike Cross MotionDokumen7 halamanPlaintiff's Response To Motion To Strike Cross MotionSue Reynolds ReidBelum ada peringkat

- Motion in Limine: Preclude Unfair EvidenceDokumen3 halamanMotion in Limine: Preclude Unfair EvidenceCharlesBelum ada peringkat

- f01c 0808781Dokumen72 halamanf01c 0808781Dylan SavageBelum ada peringkat

- Debtors (Rebecca Fleury's) Response To Motion To Dismiss-Fleury Chapter 7 BankruptcyDokumen4 halamanDebtors (Rebecca Fleury's) Response To Motion To Dismiss-Fleury Chapter 7 Bankruptcyarsmith718Belum ada peringkat

- Taylor Complaint Disbarment/Prosecution To WASHINGTON STATE BAR ASSOCIATIONDokumen45 halamanTaylor Complaint Disbarment/Prosecution To WASHINGTON STATE BAR ASSOCIATIONDawn MorganBelum ada peringkat

- FOIA FormDokumen1 halamanFOIA FormJoshua Muench100% (1)

- Response Brief of Quality Loan Service CorpDokumen24 halamanResponse Brief of Quality Loan Service CorpLee Perry100% (1)

- 17-15217 - Opening Brief PDFDokumen116 halaman17-15217 - Opening Brief PDFMadhuriBelum ada peringkat

- State of Georgia Liability Incident Report Form: Accident Information - General LiabilityDokumen4 halamanState of Georgia Liability Incident Report Form: Accident Information - General Liabilityjoe100% (1)

- Carrie Mars v. Spartanburg Chrysler Plymouth, Inc. and First National Bank of South Carolina, 713 F.2d 65, 1st Cir. (1983)Dokumen4 halamanCarrie Mars v. Spartanburg Chrysler Plymouth, Inc. and First National Bank of South Carolina, 713 F.2d 65, 1st Cir. (1983)Scribd Government DocsBelum ada peringkat

- Diversity and Alienage Jurisdiction ExplainedDokumen28 halamanDiversity and Alienage Jurisdiction ExplainedCherifa Ben AouichaBelum ada peringkat

- Motion To Change Judge and Venue Brunetti 9-17-18Dokumen8 halamanMotion To Change Judge and Venue Brunetti 9-17-18Conflict GateBelum ada peringkat

- 2016-11-28 - Robert Wallace - Lis Pendens Fed CTDokumen4 halaman2016-11-28 - Robert Wallace - Lis Pendens Fed CTapi-339692598Belum ada peringkat

- (20-22398 24) Defendants' Motion For Rehearing and To Vacate Judgment DE 131Dokumen4 halaman(20-22398 24) Defendants' Motion For Rehearing and To Vacate Judgment DE 131larry-612445Belum ada peringkat

- JQC Complaint No. No 12385 Judge Claudia Rickert IsomDokumen165 halamanJQC Complaint No. No 12385 Judge Claudia Rickert IsomNeil GillespieBelum ada peringkat

- QT Complaint NO Exhibits 62nd AveDokumen14 halamanQT Complaint NO Exhibits 62nd AveCheryl WhelestBelum ada peringkat

- 2011-08-03 ASFR NOD Response Letter TemplateDokumen17 halaman2011-08-03 ASFR NOD Response Letter TemplateNeil StierhoffBelum ada peringkat

- Torts Cases ChartDokumen24 halamanTorts Cases ChartskjdnaskdjnBelum ada peringkat

- C C C CCCCCCC CC CDokumen4 halamanC C C CCCCCCC CC CAdriana Paola GuerreroBelum ada peringkat

- Answer and CounterclaimDokumen16 halamanAnswer and CounterclaimPicon Press Media LLCBelum ada peringkat

- Original Petition Request For Declatory Judgment and Request For Equitable ReliefDokumen576 halamanOriginal Petition Request For Declatory Judgment and Request For Equitable ReliefTrey Trainor100% (1)

- Hospital's Legal Opinion On Chapter 55ADokumen8 halamanHospital's Legal Opinion On Chapter 55AEmily Featherston GrayTvBelum ada peringkat

- JAT Wheels v. DB Motoring - Request For Default JudgmentDokumen36 halamanJAT Wheels v. DB Motoring - Request For Default JudgmentSarah BursteinBelum ada peringkat

- Case in Point - Foreclosure Mills, Judicial Fraud, Consumer ExploitationDokumen2 halamanCase in Point - Foreclosure Mills, Judicial Fraud, Consumer ExploitationBarbara Ann JacksonBelum ada peringkat

- 5 - 23!5!26 California Finance Lenders LawDokumen5 halaman5 - 23!5!26 California Finance Lenders Lawkeith2438Belum ada peringkat

- Ui OverpaymentDokumen6 halamanUi OverpaymentDavid MartinBelum ada peringkat

- Susan Clickner Chapter 13 Bankruptcy 2004Dokumen59 halamanSusan Clickner Chapter 13 Bankruptcy 2004mannylulzBelum ada peringkat

- Morgan V Ocwen, MERSDokumen15 halamanMorgan V Ocwen, MERSForeclosure Fraud100% (2)

- LocalRules BK S CADokumen144 halamanLocalRules BK S CARobert Salzano100% (1)

- Khadr - D - 068 Motion To Dismiss Speedy TrialDokumen46 halamanKhadr - D - 068 Motion To Dismiss Speedy TrialfasttrackenergydrinkBelum ada peringkat

- US Copyright Office: LawDokumen17 halamanUS Copyright Office: LawUSA_CopyrightOfficeBelum ada peringkat

- Florida's Legal MafiaDokumen10 halamanFlorida's Legal MafiaDavid Arthur Walters100% (1)

- SUDDENLY APPEARING ENDORSEMENTS USED BY BANK-TRUSTEES IN FORECLOSURES - Housing JusticeDokumen27 halamanSUDDENLY APPEARING ENDORSEMENTS USED BY BANK-TRUSTEES IN FORECLOSURES - Housing JusticecloudedtitlesBelum ada peringkat

- Appellant's Opening Brief Before The Ninth Circuit in Garcia v. Santa AnaDokumen12 halamanAppellant's Opening Brief Before The Ninth Circuit in Garcia v. Santa AnaDan EscamillaBelum ada peringkat

- Kroger Lawsuit Order Denying Motion To DismissDokumen10 halamanKroger Lawsuit Order Denying Motion To Dismisspaula christianBelum ada peringkat

- Rojas-Lozano v. Google - CAPTCHA Privacy OpinionDokumen22 halamanRojas-Lozano v. Google - CAPTCHA Privacy OpinionMark JaffeBelum ada peringkat

- Fiction Versus RealityDokumen6 halamanFiction Versus RealityKara HearleyBelum ada peringkat

- SAC - RevisedDokumen57 halamanSAC - RevisedLarry Brennan100% (4)

- California Oath of OfficeDokumen2 halamanCalifornia Oath of Officesilverbull8Belum ada peringkat

- Quo WarrantoDokumen35 halamanQuo WarrantoJan-Lawrence OlacoBelum ada peringkat

- CRJ Report MOTION TO REOPEN and RECONSIDER MOTION of Forma PauperisDokumen10 halamanCRJ Report MOTION TO REOPEN and RECONSIDER MOTION of Forma PauperisCody Robert Judy100% (1)

- Complaint RICO Case Against JP Morgan-Chase - LINDA ZIMMERMAN V JPMORGAN CHASE BANK NA Foreclosure Fraud - Fighting Foreclosure Fraud by Sharing The KnowledgeDokumen16 halamanComplaint RICO Case Against JP Morgan-Chase - LINDA ZIMMERMAN V JPMORGAN CHASE BANK NA Foreclosure Fraud - Fighting Foreclosure Fraud by Sharing The Knowledgefreddiefletcher24830% (1)

- Petition for Certiorari – Patent Case 01-438 - Federal Rule of Civil Procedure 52(a)Dari EverandPetition for Certiorari – Patent Case 01-438 - Federal Rule of Civil Procedure 52(a)Belum ada peringkat

- Constitution of the State of Minnesota — Republican VersionDari EverandConstitution of the State of Minnesota — Republican VersionBelum ada peringkat

- The Truth About Defamation in Workplace Terminations - LexologyDokumen3 halamanThe Truth About Defamation in Workplace Terminations - LexologyNewDay2013Belum ada peringkat

- Soil Volume Chart For Geopot Fabric PotsDokumen2 halamanSoil Volume Chart For Geopot Fabric PotsNewDay2013Belum ada peringkat

- Vegetable Crop Yields, Plants Per Person, and Crop Spacing - Harvest To TableDokumen15 halamanVegetable Crop Yields, Plants Per Person, and Crop Spacing - Harvest To TableNewDay2013Belum ada peringkat

- Basulto v. Ialeah Automotive - FindlawDokumen9 halamanBasulto v. Ialeah Automotive - FindlawNewDay2013Belum ada peringkat

- Summary of OMB Circular A-122Dokumen3 halamanSummary of OMB Circular A-122NewDay2013Belum ada peringkat

- How To Grow Turnips in Containers - Home Guides - SF Gate PDFDokumen1 halamanHow To Grow Turnips in Containers - Home Guides - SF Gate PDFNewDay2013Belum ada peringkat

- Homeowners Composting GuideDokumen8 halamanHomeowners Composting GuideNewDay2013Belum ada peringkat

- CFPB - Laws and Regulations - Tila Combined June 2013 PDFDokumen170 halamanCFPB - Laws and Regulations - Tila Combined June 2013 PDFNewDay2013Belum ada peringkat

- Canning Lentils - Special RecipesDokumen3 halamanCanning Lentils - Special RecipesNewDay2013Belum ada peringkat

- FFC Assignment Reassignment Rev 4.3.17 FillableDokumen1 halamanFFC Assignment Reassignment Rev 4.3.17 FillableNewDay2013Belum ada peringkat

- Uscourts MDD 8 - 05 CV 02403 0 Predatory LoanDokumen7 halamanUscourts MDD 8 - 05 CV 02403 0 Predatory LoanNewDay2013Belum ada peringkat

- Statutes & Constitution - View Statutes - Online SunshineDokumen11 halamanStatutes & Constitution - View Statutes - Online SunshineNewDay2013Belum ada peringkat

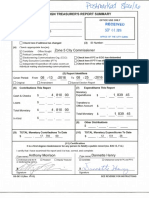

- Dannette Henry Campaign Treasurers Reports (PDFS) Zone 5 CommissionerDokumen44 halamanDannette Henry Campaign Treasurers Reports (PDFS) Zone 5 CommissionerNewDay2013Belum ada peringkat

- Redacted Gmail - Fordham Complaint To The Florida Social Media Copy Election Commission Regarding Rep - Redacted PDFDokumen5 halamanRedacted Gmail - Fordham Complaint To The Florida Social Media Copy Election Commission Regarding Rep - Redacted PDFNewDay2013Belum ada peringkat

- 15 Top Skills Project Managers Need - PM BlogDokumen5 halaman15 Top Skills Project Managers Need - PM BlogNewDay2013Belum ada peringkat

- Johnson v. Versar, Inc., 2011 Va. Cir. LEXIS 139Dokumen8 halamanJohnson v. Versar, Inc., 2011 Va. Cir. LEXIS 139NewDay2013Belum ada peringkat

- The Florida Elections Commission Email Regarding Rep. Patrick Henry and Gina Wells ComplaintDokumen1 halamanThe Florida Elections Commission Email Regarding Rep. Patrick Henry and Gina Wells ComplaintNewDay2013Belum ada peringkat

- Redacted Gmail - Fordham Complaint To The Florida Social Media Copy Election Commission Regarding Rep - Redacted PDFDokumen5 halamanRedacted Gmail - Fordham Complaint To The Florida Social Media Copy Election Commission Regarding Rep - Redacted PDFNewDay2013Belum ada peringkat

- The Kingdom and BigotryDokumen2 halamanThe Kingdom and BigotryNewDay2013Belum ada peringkat

- Fordham Complaint To The Florida Election Commission Regarding Rep. Patrick Henry and Treasurer Gina Wells - Opengovernmentfla@gmail PDFDokumen1 halamanFordham Complaint To The Florida Election Commission Regarding Rep. Patrick Henry and Treasurer Gina Wells - Opengovernmentfla@gmail PDFNewDay2013Belum ada peringkat

- Dannette Henrys August 26, 2016 Payment To DLP Realty For Campaign OfficeDokumen6 halamanDannette Henrys August 26, 2016 Payment To DLP Realty For Campaign OfficeNewDay2013Belum ada peringkat

- Complaint To The Florida Elections Commission Regarding Rep. Patrick Henry and Treasurer Gina Wells - Opengovernmentfla@GmailDokumen1 halamanComplaint To The Florida Elections Commission Regarding Rep. Patrick Henry and Treasurer Gina Wells - Opengovernmentfla@GmailNewDay2013Belum ada peringkat

- City of Daytona Links For Dannette Henry's Campaign Treasury ReportDokumen2 halamanCity of Daytona Links For Dannette Henry's Campaign Treasury ReportNewDay2013Belum ada peringkat

- 15from Fathers HeartDokumen1 halaman15from Fathers HeartNewDay2013Belum ada peringkat

- Dwayne Taylor Bills Sponsored District 26 (Daytona, Deland, Orange City)Dokumen3 halamanDwayne Taylor Bills Sponsored District 26 (Daytona, Deland, Orange City)NewDay2013Belum ada peringkat

- Ron Kenoly - We Offer PraisesDokumen61 halamanRon Kenoly - We Offer PraisesAdbeel Gutiérrez100% (20)

- On October 11, 2016 Judge Tracie Hunter Files LawsuitDokumen10 halamanOn October 11, 2016 Judge Tracie Hunter Files LawsuitNewDay2013Belum ada peringkat

- Ohio Supreme Court Response To Judge Hunter's Pridemore ComplaintDokumen1 halamanOhio Supreme Court Response To Judge Hunter's Pridemore ComplaintNewDay2013Belum ada peringkat

- Judge Tracie Hunters Complaint Against Judge Dinkelacker 1-12-15Dokumen7 halamanJudge Tracie Hunters Complaint Against Judge Dinkelacker 1-12-15NewDay2013Belum ada peringkat

- 7 Chart Patterns That Consistently Make MoneyDokumen92 halaman7 Chart Patterns That Consistently Make Moneygeorgemtchua438593% (134)

- Mexico Payments SystemsDokumen35 halamanMexico Payments SystemsVelocity_PDBelum ada peringkat

- Trend-Identifying LRC IndicatorDokumen5 halamanTrend-Identifying LRC Indicatorsalinda pereraBelum ada peringkat

- Lecture 9, Part 1 Graphical Patterns AnalysisDokumen10 halamanLecture 9, Part 1 Graphical Patterns AnalysisHilmi AbdullahBelum ada peringkat

- Accounting For InvestmentDokumen29 halamanAccounting For InvestmentSyahrul AmirulBelum ada peringkat

- Liquidation of CompaniesDokumen34 halamanLiquidation of CompaniesShakthi p raiBelum ada peringkat

- CMA Part 2 External Financial ReportingDokumen990 halamanCMA Part 2 External Financial Reportingfrances71% (7)

- Property Case NotesDokumen136 halamanProperty Case NotesGerard Relucio OroBelum ada peringkat

- Chapter 1 - Statement of Financial PositionDokumen33 halamanChapter 1 - Statement of Financial PositionAbyel Nebur78% (9)

- Stock Portfolio Tracker (Blueprint)Dokumen76 halamanStock Portfolio Tracker (Blueprint)DansBelum ada peringkat

- Insurance Law-ContributionDokumen5 halamanInsurance Law-ContributionDavid FongBelum ada peringkat

- Ap 9401-2 SheDokumen6 halamanAp 9401-2 SheLuzviminda SaspaBelum ada peringkat

- International Organizations Immunities ActDokumen7 halamanInternational Organizations Immunities ActGuy RazerBelum ada peringkat

- 2 Chart Patterns PDFDokumen25 halaman2 Chart Patterns PDFChandraBelum ada peringkat

- Project List MbaDokumen9 halamanProject List MbaadsfdgfhgjhkBelum ada peringkat

- p91 PDFDokumen1 halamanp91 PDFpenelopegerhardBelum ada peringkat

- Financial Statement Analysis 11th Edition Subramanyam Solutions Manual 1Dokumen55 halamanFinancial Statement Analysis 11th Edition Subramanyam Solutions Manual 1shaina100% (31)

- (Trading) Signal Building An Automated End-Of-Day Stock Trading System Using Microsoft Excel (Lawrence H Klamecki, 2003, Venusunited)Dokumen8 halaman(Trading) Signal Building An Automated End-Of-Day Stock Trading System Using Microsoft Excel (Lawrence H Klamecki, 2003, Venusunited)amjr1001Belum ada peringkat

- ICICI Pru Savings SurakshaDokumen8 halamanICICI Pru Savings SurakshaRojan G JosephBelum ada peringkat

- As To Possibility (1183 P. 122 Jurado) ExamplesDokumen8 halamanAs To Possibility (1183 P. 122 Jurado) ExamplesMichaella Claire LayugBelum ada peringkat

- Acctstmt DDokumen4 halamanAcctstmt Dmaakabhawan26Belum ada peringkat

- Colgate's strategy to counter growing herbal toothpaste categoryDokumen6 halamanColgate's strategy to counter growing herbal toothpaste categoryShobhit SaxenaBelum ada peringkat

- Guide To Expert Options Trading: Advanced Strategies That Will Put You in The Money FastDokumen16 halamanGuide To Expert Options Trading: Advanced Strategies That Will Put You in The Money Fastemma0% (1)

- Portfolio Report PDFDokumen7 halamanPortfolio Report PDFAnonymous kjeBVVlobBelum ada peringkat

- Act No 2031 NILDokumen30 halamanAct No 2031 NILHp AmpsBelum ada peringkat

- Banking & Economy PDF 2019: Key UpdatesDokumen103 halamanBanking & Economy PDF 2019: Key UpdatesParvesh GargBelum ada peringkat

- Newcrest BMO Global Metals & Mining Conference - PresentationDokumen21 halamanNewcrest BMO Global Metals & Mining Conference - PresentationcantuscantusBelum ada peringkat

- (2013) Abdel-Kader - What Are Structural Policies PDFDokumen2 halaman(2013) Abdel-Kader - What Are Structural Policies PDF0treraBelum ada peringkat

- Jayakody Hardware Stores Trial Balance and Financial StatementsDokumen4 halamanJayakody Hardware Stores Trial Balance and Financial StatementsmonteBelum ada peringkat

- Dematerialisation of Securities Mba ProjectDokumen68 halamanDematerialisation of Securities Mba ProjectPriyankana Bose33% (3)