Anda mungkin juga menyukai

- Yct Neetjee Main Physics Chapter-Wise Solved Papers Volume-IIDokumen800 halamanYct Neetjee Main Physics Chapter-Wise Solved Papers Volume-IIcoaching materialBelum ada peringkat

- Presentation MD NGC Developent of Gas Infrastrucure26March2008Dokumen20 halamanPresentation MD NGC Developent of Gas Infrastrucure26March2008emodeye kennethBelum ada peringkat

- FOCUS REPORT: U.S. Shale Gale under Threat from Oil Price PlungeDari EverandFOCUS REPORT: U.S. Shale Gale under Threat from Oil Price PlungePenilaian: 2 dari 5 bintang2/5 (1)

- Method Statement For Precommissioning & Commissioning of Distribution Boards - DB'sDokumen4 halamanMethod Statement For Precommissioning & Commissioning of Distribution Boards - DB'svin ssBelum ada peringkat

- High Performance VAV Single Duct SystemDokumen6 halamanHigh Performance VAV Single Duct Systemraghuragoo100% (1)

- Stx-Engine 121074 Voogvr-sYpl25EDokumen252 halamanStx-Engine 121074 Voogvr-sYpl25EGyeTaeBae100% (1)

- A Guideline For A Feasibility Study For The Development Domestic Gas Market Utilizing A FRSUDokumen319 halamanA Guideline For A Feasibility Study For The Development Domestic Gas Market Utilizing A FRSUKivuti Nyagah100% (1)

- Wiring Diagram - MV Switch Gear BPA - CUADokumen30 halamanWiring Diagram - MV Switch Gear BPA - CUAAdetunji Taiwo100% (1)

- LNG & LPG Shipping Fundamentals PDFDokumen15 halamanLNG & LPG Shipping Fundamentals PDFRafi Algawi100% (1)

- Slide Set 3 - Role of LNG, GTL, CNGDokumen71 halamanSlide Set 3 - Role of LNG, GTL, CNGRAJIB DEBNATHBelum ada peringkat

- Waste - To - Energy - Concepts For Efficient Power PlantsDokumen150 halamanWaste - To - Energy - Concepts For Efficient Power PlantsNuyul FaizahBelum ada peringkat

- Latam OIL AND GASDokumen30 halamanLatam OIL AND GASandresBelum ada peringkat

- Shale Gas SlidesDokumen8 halamanShale Gas SlidesMasoud ManeBelum ada peringkat

- Opportunities in Colombia, Ecuador, Venezuela Full Energy SpectrumDokumen50 halamanOpportunities in Colombia, Ecuador, Venezuela Full Energy SpectrumandresBelum ada peringkat

- 2012 Operations Review - FEDokumen9 halaman2012 Operations Review - FEzpippizBelum ada peringkat

- Regional Offshore MarketsDokumen28 halamanRegional Offshore MarketsGeertBelum ada peringkat

- Overview of Gas Resources 2018Dokumen31 halamanOverview of Gas Resources 2018Akib ImtihanBelum ada peringkat

- Ascertain The Future Fuel TrendsDokumen33 halamanAscertain The Future Fuel TrendsTanmay Meera MishraBelum ada peringkat

- Informe CanadaDokumen11 halamanInforme Canadajairo moralesBelum ada peringkat

- Slidex - Tips - Nigerian Gas Company Nigerian Downstream Gas Business Structure Opportunities and Reforms Issues S o NdukweDokumen23 halamanSlidex - Tips - Nigerian Gas Company Nigerian Downstream Gas Business Structure Opportunities and Reforms Issues S o Ndukweimma cover100% (1)

- Encana - Lara Conrad PresentationDokumen47 halamanEncana - Lara Conrad PresentationСергей СтояновBelum ada peringkat

- Twinza Oil 2017Dokumen19 halamanTwinza Oil 2017millotBelum ada peringkat

- MOL Pakistan - CORA DirectorateDokumen18 halamanMOL Pakistan - CORA DirectorateAsad IrfanBelum ada peringkat

- Diluent Outlook 2013Dokumen34 halamanDiluent Outlook 2013Meisy RadhistaBelum ada peringkat

- British Columbia'S Oil and Natural Gas Industry: LNG Job CreationDokumen4 halamanBritish Columbia'S Oil and Natural Gas Industry: LNG Job CreationseanBelum ada peringkat

- Carbon IntensityDokumen10 halamanCarbon IntensitySirPojiBelum ada peringkat

- G 014 027 NWDokumen28 halamanG 014 027 NWArmin MnBelum ada peringkat

- US NGL Supply Outlook: Exports To Balance: Darryl Rogers Managing Director, Midstream Oil & NGL +1 832 679 7265Dokumen14 halamanUS NGL Supply Outlook: Exports To Balance: Darryl Rogers Managing Director, Midstream Oil & NGL +1 832 679 7265Via Siti MasluhahBelum ada peringkat

- 5a. Overview of LNG Business - April 2016Dokumen13 halaman5a. Overview of LNG Business - April 2016Samuel JohnsonBelum ada peringkat

- Energy in LatamDokumen59 halamanEnergy in LatamandresBelum ada peringkat

- MI - NZFuel1.1Dokumen2 halamanMI - NZFuel1.1api-26972652Belum ada peringkat

- CNX Consol Energy Mar 2010 PresentationDokumen31 halamanCNX Consol Energy Mar 2010 PresentationAla BasterBelum ada peringkat

- ENB Day 2013 - Gas Transportation - Mark Maki - FINALDokumen16 halamanENB Day 2013 - Gas Transportation - Mark Maki - FINALjhon berez223344Belum ada peringkat

- Key Alberta Oil Sands ProjectsDokumen4 halamanKey Alberta Oil Sands Projectsmasoninman1Belum ada peringkat

- Kleenheat Presentation 2014Dokumen32 halamanKleenheat Presentation 2014scata1117Belum ada peringkat

- FactSheet OilSandsDokumen2 halamanFactSheet OilSands김도연Belum ada peringkat

- Emerging Feedstocks Olefin - JacobsDokumen32 halamanEmerging Feedstocks Olefin - JacobsUsama MalikBelum ada peringkat

- Bakken 2.0: Efficiencies in Production, Costs and Workforce: Kari Cutting, NDPC October 2018Dokumen28 halamanBakken 2.0: Efficiencies in Production, Costs and Workforce: Kari Cutting, NDPC October 2018Lindsey BondBelum ada peringkat

- British Columbia LNG Project Costs Rising Again - February 2023Dokumen21 halamanBritish Columbia LNG Project Costs Rising Again - February 2023Rahul PondBelum ada peringkat

- Coal - Bridge To The Hydrogen EconomyDokumen20 halamanCoal - Bridge To The Hydrogen EconomyNahid ParvezBelum ada peringkat

- Conversion Factors: Contact UsDokumen4 halamanConversion Factors: Contact Usthe CommissionBelum ada peringkat

- The Weyburn-Midale ProjectDokumen9 halamanThe Weyburn-Midale ProjectPutri SaidatinaBelum ada peringkat

- A Case For Midstream Energy: Listed InfrastructureDokumen8 halamanA Case For Midstream Energy: Listed Infrastructurejhon berez223344Belum ada peringkat

- 2 3 Sule - CCS2021Dokumen29 halaman2 3 Sule - CCS2021firman_SABelum ada peringkat

- The Changing Face of The Oil and Gas Industry in CanadaDokumen45 halamanThe Changing Face of The Oil and Gas Industry in CanadaJohnny RiverwalkBelum ada peringkat

- Nat Gas Export Development - CIBC - 11-2011Dokumen7 halamanNat Gas Export Development - CIBC - 11-2011tqswansonBelum ada peringkat

- Bowman 1986Dokumen17 halamanBowman 1986siaBelum ada peringkat

- Gas Flaring: An Industry Practice Faces Increasing Global AttentionDokumen12 halamanGas Flaring: An Industry Practice Faces Increasing Global AttentionjpvissottoBelum ada peringkat

- Sasol Coal-to-Liquids DevelopmentsDokumen43 halamanSasol Coal-to-Liquids DevelopmentsDertySulistyowatiBelum ada peringkat

- 2018-07-24-Wells Fargo Securiti-The Basin Book Supply vs. Takeaway-82461766 PDFDokumen5 halaman2018-07-24-Wells Fargo Securiti-The Basin Book Supply vs. Takeaway-82461766 PDFDavid SpilkinBelum ada peringkat

- Director's Cut: Lynn Helms NDIC Department of Mineral ResourcesDokumen2 halamanDirector's Cut: Lynn Helms NDIC Department of Mineral ResourcesbakkengeneralBelum ada peringkat

- Giignl 2021Dokumen68 halamanGiignl 2021Bibhu Ranjan MohantyBelum ada peringkat

- Giignl 2021 Annual Report Apr27Dokumen68 halamanGiignl 2021 Annual Report Apr27hananeBelum ada peringkat

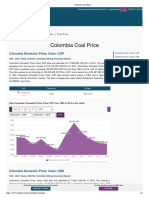

- Colombia Coal PriceDokumen6 halamanColombia Coal PriceAdam SmithBelum ada peringkat

- Director's Cut: Lynn Helms NDIC Department of Mineral ResourcesDokumen2 halamanDirector's Cut: Lynn Helms NDIC Department of Mineral ResourcesbakkengeneralBelum ada peringkat

- Coal Gasification: A PRB: OutlineDokumen13 halamanCoal Gasification: A PRB: Outlinetaufany99Belum ada peringkat

- Info On Axis Energy Nusantara - 2020Dokumen5 halamanInfo On Axis Energy Nusantara - 2020ErwinBelum ada peringkat

- U.S. Capital Advisors Common Terms and Abbreviations For More Information, Please Contact Becca Followill at 713-366-0557Dokumen1 halamanU.S. Capital Advisors Common Terms and Abbreviations For More Information, Please Contact Becca Followill at 713-366-0557Familia GonzalezBelum ada peringkat

- M 7 Monday 345 WaggenerDokumen37 halamanM 7 Monday 345 WaggenerIbrahim SalahudinBelum ada peringkat

- 2008 Q2 DevelopmentDokumen4 halaman2008 Q2 DevelopmentTimBarrowsBelum ada peringkat

- Carbonite - A New Carbon Based Energy FuelDokumen18 halamanCarbonite - A New Carbon Based Energy FuelJorge MadiasBelum ada peringkat

- Unconventional Reservoirs 5Dokumen46 halamanUnconventional Reservoirs 5ahouaBelum ada peringkat

- Japan Weekly Oil Analysis - 13 Mar 2024Dokumen9 halamanJapan Weekly Oil Analysis - 13 Mar 2024phang.zhaoying.darrenBelum ada peringkat

- FPX PresentationDokumen32 halamanFPX PresentationivokodzBelum ada peringkat

- Breakdown: The Pipeline Debate and the Threat to Canada's FutureDari EverandBreakdown: The Pipeline Debate and the Threat to Canada's FutureBelum ada peringkat

- Performance and Mathematical Model of Three-Phase Three-Winding Transformer Used in 2 Electric RailwayDokumen11 halamanPerformance and Mathematical Model of Three-Phase Three-Winding Transformer Used in 2 Electric RailwayGokul VenugopalBelum ada peringkat

- Electrical Power Transmission: Louiebert E. VirayDokumen30 halamanElectrical Power Transmission: Louiebert E. VirayCyrill Roi Domangcas BausoBelum ada peringkat

- Low Voltage DC Distribution 20 1 0.4 KV Systems PDFDokumen10 halamanLow Voltage DC Distribution 20 1 0.4 KV Systems PDFTTaanBelum ada peringkat

- Adv Work Energy Practice ProblemsDokumen11 halamanAdv Work Energy Practice ProblemsZanduarBelum ada peringkat

- Me66 Plate 4 CaseresDokumen17 halamanMe66 Plate 4 CaseresVan Eldridge Kyle CaseresBelum ada peringkat

- Liebert GXT MT CX User Manual PDFDokumen21 halamanLiebert GXT MT CX User Manual PDFBrian Boyle100% (2)

- EasyCan Brochure 2013Dokumen14 halamanEasyCan Brochure 2013nooruddinkhan1Belum ada peringkat

- Single Axis Solar Tracking System Using 555 ICDokumen19 halamanSingle Axis Solar Tracking System Using 555 ICSuresh KumarBelum ada peringkat

- Energies 14 05268 v2Dokumen28 halamanEnergies 14 05268 v2The Shameless AddictBelum ada peringkat

- RdsoDokumen7 halamanRdsoMrinmy ChakrabortyBelum ada peringkat

- Motor Parameters 03Dokumen2 halamanMotor Parameters 03Miguel eBelum ada peringkat

- Elmeasure Transducer CatalogDokumen1 halamanElmeasure Transducer CatalogSEO BDMBelum ada peringkat

- Report of Sampling and Analysis: Bara Energi Naga Sukses, PTDokumen1 halamanReport of Sampling and Analysis: Bara Energi Naga Sukses, PTSAHABAT GANJAR SULBARBelum ada peringkat

- Ishy CktsDokumen3 halamanIshy Cktsrhedmish0% (1)

- Oral Ques AnsDokumen182 halamanOral Ques AnsDheeranBelum ada peringkat

- Physics Research AssignmentDokumen7 halamanPhysics Research AssignmentMimi HuynhBelum ada peringkat

- Major Accident Hazard in Bioenergy ProductionDokumen10 halamanMajor Accident Hazard in Bioenergy ProductionFebriardy -Belum ada peringkat

- Sony Battery Charger BC-M50 Service ManualDokumen30 halamanSony Battery Charger BC-M50 Service ManualjorgeluismlimaBelum ada peringkat

- EV3200 EMERSON Door Control InverterDokumen59 halamanEV3200 EMERSON Door Control InverterRebecca DangBelum ada peringkat

- Final Project For Inno HubDokumen8 halamanFinal Project For Inno HubJohn Errol MergalBelum ada peringkat

- Capacitor Bank CataloguesDokumen36 halamanCapacitor Bank Cataloguessani priadiBelum ada peringkat

- Molecular Energy Levels NotesDokumen5 halamanMolecular Energy Levels Notesskrim2Belum ada peringkat

- 4 Power Supply System Installation GuideDokumen81 halaman4 Power Supply System Installation GuideAguinaldo Jesus de BritoBelum ada peringkat

- Profile of Engr. Md. Monirul Islam Profile of Engr. Md. Monirul IslamDokumen1 halamanProfile of Engr. Md. Monirul Islam Profile of Engr. Md. Monirul IslamBlue FinBelum ada peringkat