Anda mungkin juga menyukai

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- 5 Moments Pocket-LeafletDokumen2 halaman5 Moments Pocket-LeafletIrul AnwarBelum ada peringkat

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- dm2020 0202 PDFDokumen6 halamandm2020 0202 PDFcode4saleBelum ada peringkat

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- Ph020en PDFDokumen30 halamanPh020en PDFcode4saleBelum ada peringkat

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- Instructions For Hospital Workers When Treating Ebola PatientsDokumen3 halamanInstructions For Hospital Workers When Treating Ebola PatientsKERANewsBelum ada peringkat

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

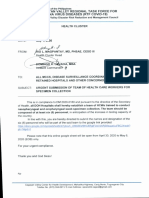

- CVRIATF MEMO - 2020-0020 Urgent Submission of Team of Health Care Workers For Specimen CollectionDokumen1 halamanCVRIATF MEMO - 2020-0020 Urgent Submission of Team of Health Care Workers For Specimen Collectioncode4saleBelum ada peringkat

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- Leaflet Resmi Who Cuci Tangan Dengan Handwash Dan Handrub PDFDokumen1 halamanLeaflet Resmi Who Cuci Tangan Dengan Handwash Dan Handrub PDFRaniBelum ada peringkat

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- Scripps Hospital Patient Visitor Policy PDFDokumen2 halamanScripps Hospital Patient Visitor Policy PDFcode4saleBelum ada peringkat

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Certificate of Appearance: Regional Trial Court Branch 01Dokumen1 halamanCertificate of Appearance: Regional Trial Court Branch 01code4saleBelum ada peringkat

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- Patient Rights and ResponsibilitiesDokumen6 halamanPatient Rights and Responsibilitiescode4saleBelum ada peringkat

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- I Love YouDokumen1 halamanI Love Youcode4saleBelum ada peringkat

- Counter AffidavitDokumen5 halamanCounter Affidavitcode4saleBelum ada peringkat

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- I Love You 123455432156789Dokumen1 halamanI Love You 123455432156789code4saleBelum ada peringkat

- Tell Me Your DreamDokumen2 halamanTell Me Your Dreamcode4saleBelum ada peringkat

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- LaborDokumen29 halamanLaborAnastasha ArchangelBelum ada peringkat

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (73)

- (2019) Smuggled Notes - Dimaampao Lecture On Tax Principles and Remedies PDFDokumen58 halaman(2019) Smuggled Notes - Dimaampao Lecture On Tax Principles and Remedies PDFSteph100% (8)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- I Love YouDokumen1 halamanI Love Youcode4saleBelum ada peringkat

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- Torts ReviewerDokumen121 halamanTorts ReviewerJingJing Romero100% (9)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- Professional Services, Inc. v. AganaDokumen11 halamanProfessional Services, Inc. v. Aganacode4saleBelum ada peringkat

- LUCAS Vs TUAÑO PDFDokumen39 halamanLUCAS Vs TUAÑO PDFcode4saleBelum ada peringkat

- TestDokumen1 halamanTestcode4saleBelum ada peringkat

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- Public AdministrationDokumen33 halamanPublic Administrationcode4sale100% (5)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- Labor Law SyllabusDokumen185 halamanLabor Law SyllabusptbattungBelum ada peringkat

- Other Percentage TaxesDokumen40 halamanOther Percentage TaxesKay Hanalee Villanueva NorioBelum ada peringkat

- 9 Solidum v. PeopleDokumen30 halaman9 Solidum v. PeopleMlaBelum ada peringkat

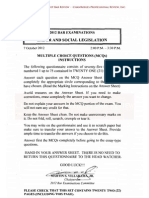

- Compilation of The Labor Law and Social Legislation Bar Examinations Questions and Suggested Answers (1994-2017)Dokumen374 halamanCompilation of The Labor Law and Social Legislation Bar Examinations Questions and Suggested Answers (1994-2017)Marefel Anora100% (20)

- Election Law CasesDokumen9 halamanElection Law Casescode4saleBelum ada peringkat

- Alitalia Airways, Inc v. CADokumen14 halamanAlitalia Airways, Inc v. CAJosiah DavidBelum ada peringkat

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- Astudillo Vs Manila Electric CompanyDokumen6 halamanAstudillo Vs Manila Electric Companycode4saleBelum ada peringkat

- Commissioner of Internal Revenue vs. Primetown Property Group, Inc.Dokumen11 halamanCommissioner of Internal Revenue vs. Primetown Property Group, Inc.Queenie SabladaBelum ada peringkat

- Alitalia Airways, Inc v. CADokumen14 halamanAlitalia Airways, Inc v. CAJosiah DavidBelum ada peringkat

- PVSRA (Price/Volume/S&R Analysis) : Is Part ofDokumen90 halamanPVSRA (Price/Volume/S&R Analysis) : Is Part ofonlylf28311Belum ada peringkat

- Manual For Internal Audit On India Railways: Ministry of Railways (Railway Board) Government of IndiaDokumen85 halamanManual For Internal Audit On India Railways: Ministry of Railways (Railway Board) Government of IndiaKannan Chakrapani100% (1)

- PWC Spectrum: Timing Is EverythingDokumen16 halamanPWC Spectrum: Timing Is EverythingEvan TindellBelum ada peringkat

- 2008 Hotel Management Agreement - SampleDokumen7 halaman2008 Hotel Management Agreement - SampleamolreddiwarBelum ada peringkat

- MCQ Accounting StandardDokumen13 halamanMCQ Accounting StandardNgân GiangBelum ada peringkat

- Vonovia 9M2021 Presentation 20211118Dokumen76 halamanVonovia 9M2021 Presentation 20211118LorenzoBelum ada peringkat

- Topic 1: Financial Accounting Meaning Scope ImportanceDokumen78 halamanTopic 1: Financial Accounting Meaning Scope Importancerinkisingla100% (2)

- Relevant CostingDokumen6 halamanRelevant Costingzee abadillaBelum ada peringkat

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- ACCT 202: Managerial Accounting: Job Order CostingDokumen38 halamanACCT 202: Managerial Accounting: Job Order CostingHieu DamBelum ada peringkat

- Advanced Financial AccountingDokumen8 halamanAdvanced Financial AccountingEKI TEENEBelum ada peringkat

- Hola Kola Case SolutionDokumen8 halamanHola Kola Case Solutionsathya50% (8)

- Basic MathDokumen6 halamanBasic MathWarda MamasalagatBelum ada peringkat

- Zero Coupon BondDokumen5 halamanZero Coupon BondnauliBelum ada peringkat

- Preliminary Due Diligence ChecklistDokumen7 halamanPreliminary Due Diligence Checklistekatamadze1972Belum ada peringkat

- AE 25 Module 1 Lesson 1Dokumen99 halamanAE 25 Module 1 Lesson 1Queeny Mae Cantre ReutaBelum ada peringkat

- CH 7Dokumen41 halamanCH 7Abdulrahman AlotaibiBelum ada peringkat

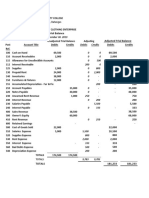

- Excel - 33 - 38Dokumen4 halamanExcel - 33 - 38api-259228049Belum ada peringkat

- NCL Industries Limited: Pay Slip For The Month of May - 2021Dokumen1 halamanNCL Industries Limited: Pay Slip For The Month of May - 2021Siva KrishnaBelum ada peringkat

- Accounting For ManagersDokumen61 halamanAccounting For ManagersSwapnil DeshpandeBelum ada peringkat

- Home Assignment 1Dokumen3 halamanHome Assignment 1AUBelum ada peringkat

- SolutionsDokumen11 halamanSolutionsRaghuveer ChandraBelum ada peringkat

- Managerial Econ - GroupDokumen2 halamanManagerial Econ - GroupQueenie Marie Obial AlasBelum ada peringkat

- Instructions: Including Instructions For Schedules A, B, C, D, E, F, J, and SEDokumen143 halamanInstructions: Including Instructions For Schedules A, B, C, D, E, F, J, and SEsterlingsilverrose1Belum ada peringkat

- Bonds and Their Valuation ExerciseDokumen42 halamanBonds and Their Valuation ExerciseLee Wong100% (1)

- Saln FormatDokumen3 halamanSaln FormatMaricrisBelum ada peringkat

- Quizlet PDFDokumen3 halamanQuizlet PDFPatriciaBelum ada peringkat

- Alvarez Vs GuingonaDokumen3 halamanAlvarez Vs GuingonaRaymond Roque100% (1)

- CIR V Acesite Hotel Corp.Dokumen4 halamanCIR V Acesite Hotel Corp.'mhariie-mhAriie TOotBelum ada peringkat

- Olmstead Corporation S Capital Structure Is As Follows The Following Additional InformationDokumen1 halamanOlmstead Corporation S Capital Structure Is As Follows The Following Additional InformationHassan JanBelum ada peringkat

- Strategic Cost Management Quiz No. 1Dokumen5 halamanStrategic Cost Management Quiz No. 1Alexandra Nicole IsaacBelum ada peringkat

- You Need a Budget: The Proven System for Breaking the Paycheck-to-Paycheck Cycle, Getting Out of Debt, and Living the Life You WantDari EverandYou Need a Budget: The Proven System for Breaking the Paycheck-to-Paycheck Cycle, Getting Out of Debt, and Living the Life You WantPenilaian: 4 dari 5 bintang4/5 (104)

- Personal Finance for Beginners - A Simple Guide to Take Control of Your Financial SituationDari EverandPersonal Finance for Beginners - A Simple Guide to Take Control of Your Financial SituationPenilaian: 4.5 dari 5 bintang4.5/5 (18)

- How To Budget And Manage Your Money In 7 Simple StepsDari EverandHow To Budget And Manage Your Money In 7 Simple StepsPenilaian: 5 dari 5 bintang5/5 (4)

- Budget Management for Beginners: Proven Strategies to Revamp Business & Personal Finance Habits. Stop Living Paycheck to Paycheck, Get Out of Debt, and Save Money for Financial Freedom.Dari EverandBudget Management for Beginners: Proven Strategies to Revamp Business & Personal Finance Habits. Stop Living Paycheck to Paycheck, Get Out of Debt, and Save Money for Financial Freedom.Penilaian: 5 dari 5 bintang5/5 (89)

- Financial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassDari EverandFinancial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassBelum ada peringkat

- How to Pay Zero Taxes, 2020-2021: Your Guide to Every Tax Break the IRS AllowsDari EverandHow to Pay Zero Taxes, 2020-2021: Your Guide to Every Tax Break the IRS AllowsBelum ada peringkat

- The Black Girl's Guide to Financial Freedom: Build Wealth, Retire Early, and Live the Life of Your DreamsDari EverandThe Black Girl's Guide to Financial Freedom: Build Wealth, Retire Early, and Live the Life of Your DreamsBelum ada peringkat