Anda mungkin juga menyukai

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- Bhagya Viva ProjectDokumen13 halamanBhagya Viva ProjectBhagya sBelum ada peringkat

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- BIR Ruling No. 051 2000 PDFDokumen3 halamanBIR Ruling No. 051 2000 PDFVina CeeBelum ada peringkat

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- Tax Invoice: Smartschool Education PVT LTDDokumen1 halamanTax Invoice: Smartschool Education PVT LTDHarshit SuriBelum ada peringkat

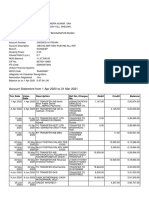

- Account Statement From 1 Apr 2020 To 31 Mar 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDokumen3 halamanAccount Statement From 1 Apr 2020 To 31 Mar 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceAbhay RajBelum ada peringkat

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- Chase Bank Account Rules and Regulations 12-31-08Dokumen34 halamanChase Bank Account Rules and Regulations 12-31-08wps013100% (1)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- 1 Tax Rev - CIR Vs Javier 199 Scra 824Dokumen8 halaman1 Tax Rev - CIR Vs Javier 199 Scra 824LucioJr Avergonzado100% (1)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- Develop Understanding of TaxationDokumen14 halamanDevelop Understanding of Taxationnatanme794Belum ada peringkat

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- User Manual: Intellect Core Banking System (CBS)Dokumen50 halamanUser Manual: Intellect Core Banking System (CBS)tempo100% (5)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- Navy Children School, Visakhapatnam Fee Structure (2023-24) For Existing StudentsDokumen1 halamanNavy Children School, Visakhapatnam Fee Structure (2023-24) For Existing StudentsPriyanka VermaBelum ada peringkat

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- Thesis On Electronic PaymentDokumen6 halamanThesis On Electronic Paymentgbvhhgpj100% (2)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- 1450 BTDokumen1 halaman1450 BTShahjada ShekhBelum ada peringkat

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- Windhoek Gymnasium 2022 School Fees Final Web Upload 01Dokumen3 halamanWindhoek Gymnasium 2022 School Fees Final Web Upload 01Janet NdakalakoBelum ada peringkat

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- Exercise 3: Bank of The Philippine IslandDokumen4 halamanExercise 3: Bank of The Philippine IslandKim FloresBelum ada peringkat

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (74)

- Offering Letter Ibu SintyaDokumen3 halamanOffering Letter Ibu Sintyamiaw87385Belum ada peringkat

- Bill Invoice PDFDokumen2 halamanBill Invoice PDFmandy0% (1)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- 01.04.2022 To 20.02.2023Dokumen22 halaman01.04.2022 To 20.02.2023PrashantBelum ada peringkat

- Hotel Booking PDFDokumen2 halamanHotel Booking PDFferuzbekBelum ada peringkat

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The Way The World PaysDokumen22 halamanThe Way The World Paysrainasanjeev_1Belum ada peringkat

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (345)

- Nilson ReportDokumen12 halamanNilson Reporttsc databaseBelum ada peringkat

- Spaze TowerDokumen1 halamanSpaze TowerShubhamvnsBelum ada peringkat

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- Lousianna Tax InstructionDokumen17 halamanLousianna Tax Instructionchuckhsu1248Belum ada peringkat

- Invoice - 1Dokumen1 halamanInvoice - 1Toney KurianBelum ada peringkat

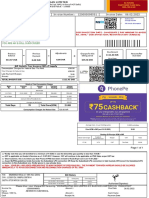

- C7021-22-2717923 30-03-2023 30-03-2023 Sold by (Pharmacy) Bill To / Ship To (Patient) Healthsaverz Medical LLP UshaDokumen1 halamanC7021-22-2717923 30-03-2023 30-03-2023 Sold by (Pharmacy) Bill To / Ship To (Patient) Healthsaverz Medical LLP UshaViraj DobriyalBelum ada peringkat

- New Anand PharmaDokumen1 halamanNew Anand PharmaShri Rani Sati officeBelum ada peringkat

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- Personal Banking: Consumer Pricing InformationDokumen5 halamanPersonal Banking: Consumer Pricing InformationSteph BryattBelum ada peringkat

- Abhi Gas BillDokumen1 halamanAbhi Gas Billritik chawlaBelum ada peringkat

- EBTax UAT Test Script ARDokumen2 halamanEBTax UAT Test Script ARchirag0% (1)

- Topic 14 - Income and Business TaxationDokumen71 halamanTopic 14 - Income and Business TaxationFrancez Anne Guanzon100% (1)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- TMC Vs CIRDokumen3 halamanTMC Vs CIREllaine BernardinoBelum ada peringkat

- What Are The Requirements of The ATMDokumen2 halamanWhat Are The Requirements of The ATMUvindu HarshanBelum ada peringkat

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)