Anda mungkin juga menyukai

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- Estrada vs. SandiganbayanDokumen47 halamanEstrada vs. SandiganbayanAira Mae P. LayloBelum ada peringkat

- People vs. CordovaDokumen30 halamanPeople vs. CordovaAira Mae P. LayloBelum ada peringkat

- People vs. TabusoDokumen9 halamanPeople vs. TabusoAira Mae P. LayloBelum ada peringkat

- Pana and Tiguman vs. PeopleDokumen13 halamanPana and Tiguman vs. PeopleAira Mae P. LayloBelum ada peringkat

- People vs. FloraDokumen15 halamanPeople vs. FloraAira Mae P. LayloBelum ada peringkat

- LRTA v. AlvarezDokumen16 halamanLRTA v. AlvarezAira Mae P. LayloBelum ada peringkat

- Coca Cola FEMSA v. Bacolod Sales ForceDokumen13 halamanCoca Cola FEMSA v. Bacolod Sales ForceAira Mae P. LayloBelum ada peringkat

- People vs. LandichoDokumen41 halamanPeople vs. LandichoAira Mae P. LayloBelum ada peringkat

- Philippine Transmarine Carriers vs. Norwegian CrewDokumen16 halamanPhilippine Transmarine Carriers vs. Norwegian CrewAira Mae P. LayloBelum ada peringkat

- SM SYSTEMS Corp vs. Oscar Camerino PDFDokumen12 halamanSM SYSTEMS Corp vs. Oscar Camerino PDFAira Mae P. LayloBelum ada peringkat

- SM SYSTEMS Corp vs. Oscar Camerino PDFDokumen12 halamanSM SYSTEMS Corp vs. Oscar Camerino PDFAira Mae P. LayloBelum ada peringkat

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5795)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (74)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1091)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

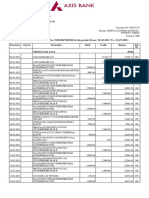

- AdvanceReceipt2021 08 01 09 13 31Dokumen8 halamanAdvanceReceipt2021 08 01 09 13 31Nimesh PatelBelum ada peringkat

- Robert Madsen Whistle-Blower CaseDokumen220 halamanRobert Madsen Whistle-Blower CaseDealBook100% (1)

- CA IPCC Accounting Guideline Answers May 2015Dokumen24 halamanCA IPCC Accounting Guideline Answers May 2015Prashant PandeyBelum ada peringkat

- ConsolidateStatement Mar 20Dokumen5 halamanConsolidateStatement Mar 20Coid CekBelum ada peringkat

- Advanced CollectionsDokumen11 halamanAdvanced CollectionsMd.Forhad HossainBelum ada peringkat

- Assignment On Foreign Exchange Market.Dokumen6 halamanAssignment On Foreign Exchange Market.Sadman Skib.0% (1)

- CHFS QuestionnaireDokumen102 halamanCHFS QuestionnaireNameBelum ada peringkat

- Off Balance Sheet Bank InstrumentsDokumen10 halamanOff Balance Sheet Bank Instrumentsphard2345Belum ada peringkat

- Revolut StatementDokumen2 halamanRevolut StatementSaàd Bouhssini100% (1)

- N D B Securities (PVT) LTD, 5 Floor, # 40, NDB Building, Nawam Mawatha, Colombo 02. Tel: +94 11 2131000 Fax: +9411 2314180Dokumen5 halamanN D B Securities (PVT) LTD, 5 Floor, # 40, NDB Building, Nawam Mawatha, Colombo 02. Tel: +94 11 2131000 Fax: +9411 2314180Randora LkBelum ada peringkat

- Challenges & OppDokumen7 halamanChallenges & OppmuruganvgBelum ada peringkat

- 5 6323590618891158440Dokumen61 halaman5 6323590618891158440Aveek ModakBelum ada peringkat

- Conference Details SunflowerDokumen16 halamanConference Details SunflowerSahil VoraBelum ada peringkat

- A Final Project ReportDokumen82 halamanA Final Project ReportTarun BishtBelum ada peringkat

- Atp 02 - Ap Fspec 66Dokumen18 halamanAtp 02 - Ap Fspec 66Gurushantha DoddamaniBelum ada peringkat

- Indusind BankDokumen19 halamanIndusind BankAarti GajulBelum ada peringkat

- Dutch-Bangla Bank Limited Bashundhara Branch K 3/1-C, Jogonnathpur Bashundhara Dhaka BangladeshDokumen2 halamanDutch-Bangla Bank Limited Bashundhara Branch K 3/1-C, Jogonnathpur Bashundhara Dhaka BangladeshNur NobiBelum ada peringkat

- Friedman v. Union Bank of SwitzerlandDokumen14 halamanFriedman v. Union Bank of SwitzerlandJon McFarlaneBelum ada peringkat

- English Learning Guide Competency 1 Unit 6: Financial Education Workshop 1 Centro de Servicios Financieros-CSFDokumen8 halamanEnglish Learning Guide Competency 1 Unit 6: Financial Education Workshop 1 Centro de Servicios Financieros-CSFHarol Armando González HigueraBelum ada peringkat

- Future of Southeast Asia Digital Financial ServicesDokumen52 halamanFuture of Southeast Asia Digital Financial ServicesMaria HanyBelum ada peringkat

- Swissquote-Research 4872bcb4 enDokumen14 halamanSwissquote-Research 4872bcb4 enaliffalniBelum ada peringkat

- Customer Application Form: Personal DetailsDokumen16 halamanCustomer Application Form: Personal DetailsSantosh creationsBelum ada peringkat

- NFC Based E-Money TechnologyDokumen4 halamanNFC Based E-Money TechnologyNagarajEEshwarappaBelum ada peringkat

- Rahma Indrawati Selvie Engeline: Data-Data Nasabah Wanita Nama No - Kartu BankDokumen144 halamanRahma Indrawati Selvie Engeline: Data-Data Nasabah Wanita Nama No - Kartu BankRachman MercyBelum ada peringkat

- 4 GKDC: Rule-Book 4 GKDC - Design Your DreamsDokumen34 halaman4 GKDC: Rule-Book 4 GKDC - Design Your DreamskevinBelum ada peringkat

- Customer Satisfaction With Regard To ATM ServicesDokumen75 halamanCustomer Satisfaction With Regard To ATM Servicesdinesh_v_0076945100% (2)

- BFI Topic 1 2 3Dokumen17 halamanBFI Topic 1 2 3Arnold LuayonBelum ada peringkat

- FREE NISM MOCK TEST - NISM Series VI Depository Operations Certification Examination Mock Test Free by PrepCafeDokumen14 halamanFREE NISM MOCK TEST - NISM Series VI Depository Operations Certification Examination Mock Test Free by PrepCafeNISM PrepCafe - FREE NISM Mock Tests, Free NISM Study Material Download and much more50% (2)

- BCC BR 107 152Dokumen12 halamanBCC BR 107 152lkamalBelum ada peringkat

- A Presentation On: Credit CardsDokumen26 halamanA Presentation On: Credit Cardsshweta.gdp100% (2)