Anda mungkin juga menyukai

- International Financial Management PgapteDokumen25 halamanInternational Financial Management PgapterameshmbaBelum ada peringkat

- Nature and Measurement of Exposure and RiskDokumen10 halamanNature and Measurement of Exposure and RiskkomalBelum ada peringkat

- International Financial Management VillafloresDokumen36 halamanInternational Financial Management VillafloresSebastian M.VBelum ada peringkat

- Risk Reduction Through HedgingDokumen22 halamanRisk Reduction Through Hedgingtushar1daveBelum ada peringkat

- Exchange Rate Risk HedgingDokumen16 halamanExchange Rate Risk HedgingMehul DubeyBelum ada peringkat

- Foreign Exchange ExposuresDokumen34 halamanForeign Exchange ExposuresPrince LandichoBelum ada peringkat

- 9 DRM Risk ManagementDokumen15 halaman9 DRM Risk ManagementPrasanjit BiswasBelum ada peringkat

- Transaction ExposureDokumen28 halamanTransaction ExposureMai LiênBelum ada peringkat

- Foreign Exchange ExposureDokumen29 halamanForeign Exchange ExposurebhargaviBelum ada peringkat

- FX Risk Management Transaction Exposure: Slide 1Dokumen55 halamanFX Risk Management Transaction Exposure: Slide 1prakashputtuBelum ada peringkat

- P7-Exchange Risk-Managing and ProtectionDokumen31 halamanP7-Exchange Risk-Managing and Protectionenacengic99Belum ada peringkat

- Transaction Exposure: Management: South-Western/Thomson Learning © 2006Dokumen30 halamanTransaction Exposure: Management: South-Western/Thomson Learning © 2006Adi PhasaBelum ada peringkat

- Topic 2: Foreign Exchange Risk ManagementDokumen36 halamanTopic 2: Foreign Exchange Risk ManagementCenith CheeBelum ada peringkat

- RAROC Models ExplainedDokumen27 halamanRAROC Models ExplainedA. Saeed KhawajaBelum ada peringkat

- Investment ConceptsDokumen54 halamanInvestment Conceptsmarine19.vedelBelum ada peringkat

- Foreign Exchange Risk and ExposureDokumen77 halamanForeign Exchange Risk and ExposureRammohanreddy RajidiBelum ada peringkat

- Risk Management Through Forex Derivatives: Presented ByDokumen31 halamanRisk Management Through Forex Derivatives: Presented ByRoma ManwaniBelum ada peringkat

- International Financial ManagementDokumen14 halamanInternational Financial ManagementOona NiallBelum ada peringkat

- FIN4003 - Lecture02 - Mechanisms - of - Futures 16 Mar 2018Dokumen27 halamanFIN4003 - Lecture02 - Mechanisms - of - Futures 16 Mar 2018Who Am iBelum ada peringkat

- FX Exposure Risks & Hedging Strategies for Multinational FirmsDokumen15 halamanFX Exposure Risks & Hedging Strategies for Multinational FirmsAbilash ReddyBelum ada peringkat

- Chapter No.2: Risk Management and Basics of DerivativesDokumen21 halamanChapter No.2: Risk Management and Basics of DerivativesSantosh SarojBelum ada peringkat

- FX Risk Management: Hedging Foreign Exchange Transaction ExposureDokumen55 halamanFX Risk Management: Hedging Foreign Exchange Transaction Exposurethensuresh100% (1)

- Forex Exposure and Exposure Transaction Management: Nageeta Tata Rosa, MBADokumen11 halamanForex Exposure and Exposure Transaction Management: Nageeta Tata Rosa, MBAIndri setia PutriBelum ada peringkat

- Managing Transaction ExposureDokumen30 halamanManaging Transaction ExposureImtiaz MasroorBelum ada peringkat

- Chapter - 9 and 10: International FinanceDokumen35 halamanChapter - 9 and 10: International FinanceRiddhi BhattBelum ada peringkat

- Thanh Toan QT Nhom 4Dokumen24 halamanThanh Toan QT Nhom 4Phan ThọBelum ada peringkat

- Foreign Exchange Risk Management StrategiesDokumen13 halamanForeign Exchange Risk Management Strategieskenedy simwingaBelum ada peringkat

- Foreign Exchange Risk&ExposureDokumen16 halamanForeign Exchange Risk&ExposureNimesh_Belum ada peringkat

- Accounting For Derivatives and Hedging-TransactionsDokumen40 halamanAccounting For Derivatives and Hedging-TransactionsJoshua Sto Domingo100% (3)

- Final FX Risk & Exposure ManagementDokumen33 halamanFinal FX Risk & Exposure ManagementkarunaksBelum ada peringkat

- Managing Exchange Rate ExposureDokumen20 halamanManaging Exchange Rate ExposureJam MajBelum ada peringkat

- Currency FuturesDokumen37 halamanCurrency Futuresshambhu.1976Belum ada peringkat

- Fin 413 - Risk ManagementDokumen56 halamanFin 413 - Risk Managementanujalives1Belum ada peringkat

- Unit 4 Derivatives Part 1Dokumen19 halamanUnit 4 Derivatives Part 1UnathiBelum ada peringkat

- Theory and Practice of International Financial Management: Foreign Exchange Risk ManagementDokumen44 halamanTheory and Practice of International Financial Management: Foreign Exchange Risk ManagementBabalss MishraBelum ada peringkat

- Exposure Management: Sonal Shirude-152 Gunit Jain - 119 Raj Avlani - 144 Sunil Patel - 153 Chandan Jagtap - 113Dokumen29 halamanExposure Management: Sonal Shirude-152 Gunit Jain - 119 Raj Avlani - 144 Sunil Patel - 153 Chandan Jagtap - 113Rucha ModiBelum ada peringkat

- Investment Analysis & Portfolio ManagementDokumen40 halamanInvestment Analysis & Portfolio ManagementShuhab KhosoBelum ada peringkat

- Currency Risk Management: Chapter Learning ObjectivesDokumen25 halamanCurrency Risk Management: Chapter Learning ObjectivesDINEO PRUDENCE NONGBelum ada peringkat

- Topic 11 - DerivativesDokumen38 halamanTopic 11 - DerivativesNur AsyiqinBelum ada peringkat

- FN 605: International Business FinanceDokumen32 halamanFN 605: International Business FinancelekokoBelum ada peringkat

- Chapter 4 Advanced Financial Accounting PDFDokumen39 halamanChapter 4 Advanced Financial Accounting PDFAddis FikruBelum ada peringkat

- Introduction To Market RiskDokumen140 halamanIntroduction To Market RiskSaurabhBelum ada peringkat

- UNIT 5 ForexDokumen13 halamanUNIT 5 Forexraj kumarBelum ada peringkat

- DRM CH 2 - Futures Markets and Central Counterparties PDFDokumen35 halamanDRM CH 2 - Futures Markets and Central Counterparties PDFNeha SinghBelum ada peringkat

- Strategic Financial Planning Lec 2Dokumen62 halamanStrategic Financial Planning Lec 2MALIK WASEEM JANBelum ada peringkat

- Chapter 6: Foreign Exchange Risk Management TechniquesDokumen18 halamanChapter 6: Foreign Exchange Risk Management TechniquesJuana BoresBelum ada peringkat

- Basics of Derivatives Prof. Naveen BhatiaDokumen103 halamanBasics of Derivatives Prof. Naveen BhatiaJay ShahBelum ada peringkat

- Topic 1 DerivativesDokumen12 halamanTopic 1 DerivativesMaría Delgado GonzálezBelum ada peringkat

- Currency RiskDokumen65 halamanCurrency RiskBilal AhmadBelum ada peringkat

- Hedging Strategies ExplainedDokumen28 halamanHedging Strategies ExplainedNadeem AhmadBelum ada peringkat

- Short Term Financial Management in a Multinational CorporationDokumen46 halamanShort Term Financial Management in a Multinational Corporationhaidersyed060% (2)

- FX Risk ManagementDokumen27 halamanFX Risk ManagementSMO979Belum ada peringkat

- Foreign Exchange Risk ManagementDokumen17 halamanForeign Exchange Risk ManagementPraseem KulshresthaBelum ada peringkat

- Basic 11Dokumen34 halamanBasic 11Wynn MaiBelum ada peringkat

- BFN 814BDokumen29 halamanBFN 814BQUADRI YUSUFBelum ada peringkat

- Multinational Corporations and Global Financial Environment: Facilities in More Than One CountryDokumen11 halamanMultinational Corporations and Global Financial Environment: Facilities in More Than One CountryANH NGUYEN DANG QUEBelum ada peringkat

- Updated LECTURE 2 - Risk Quantification (Basic Concepts)Dokumen47 halamanUpdated LECTURE 2 - Risk Quantification (Basic Concepts)Ajid Ur Rehman100% (1)

- Commodities ExchangeDokumen59 halamanCommodities ExchangesherazhassannBelum ada peringkat

- Risk Management: An Introduction To Financial Engineering: Mcgraw-Hill/IrwinDokumen29 halamanRisk Management: An Introduction To Financial Engineering: Mcgraw-Hill/IrwinSeptian AbdiansyahBelum ada peringkat

- Diaz, Rony V. - at War's End An ElegyDokumen6 halamanDiaz, Rony V. - at War's End An ElegyIan Rosales CasocotBelum ada peringkat

- Relatório ESG Air GalpDokumen469 halamanRelatório ESG Air GalpIngrid Camilo dos SantosBelum ada peringkat

- Aldecoa v. Insular GovtDokumen1 halamanAldecoa v. Insular Govtowenalan buenaventuraBelum ada peringkat

- Official Website of the Department of Homeland Security STEM OPT ExtensionDokumen1 halamanOfficial Website of the Department of Homeland Security STEM OPT ExtensionTanishq SankaBelum ada peringkat

- Article Summary Assignment 2021Dokumen2 halamanArticle Summary Assignment 2021Mengyan XiongBelum ada peringkat

- Kina Finalan CHAPTER 1-5 LIVED EXPERIENCES OF STUDENT-ATHLETESDokumen124 halamanKina Finalan CHAPTER 1-5 LIVED EXPERIENCES OF STUDENT-ATHLETESDazel Dizon GumaBelum ada peringkat

- Annexure 2 Form 72 (Scope) Annexure IDokumen4 halamanAnnexure 2 Form 72 (Scope) Annexure IVaghasiyaBipinBelum ada peringkat

- Case Digest in Special ProceedingsDokumen42 halamanCase Digest in Special ProceedingsGuiller MagsumbolBelum ada peringkat

- Reading and Writing Skills: Quarter 4 - Module 1Dokumen16 halamanReading and Writing Skills: Quarter 4 - Module 1Ericka Marie AlmadoBelum ada peringkat

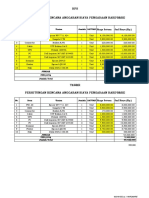

- HPS Perhitungan Rencana Anggaran Biaya Pengadaan Hardware: No. Item Uraian Jumlah SATUANDokumen2 halamanHPS Perhitungan Rencana Anggaran Biaya Pengadaan Hardware: No. Item Uraian Jumlah SATUANYanto AstriBelum ada peringkat

- Line GraphDokumen13 halamanLine GraphMikelAgberoBelum ada peringkat

- Teacher swap agreement for family reasonsDokumen4 halamanTeacher swap agreement for family reasonsKimber LeeBelum ada peringkat

- Revision Summary - Rainbow's End by Jane Harrison PDFDokumen47 halamanRevision Summary - Rainbow's End by Jane Harrison PDFchris100% (3)

- FE 405 Ps 3 AnsDokumen12 halamanFE 405 Ps 3 Anskannanv93Belum ada peringkat

- Lec 1 Modified 19 2 04102022 101842amDokumen63 halamanLec 1 Modified 19 2 04102022 101842amnimra nazimBelum ada peringkat

- Your Money Personality Unlock The Secret To A Rich and Happy LifeDokumen30 halamanYour Money Personality Unlock The Secret To A Rich and Happy LifeLiz Koh100% (1)

- Soil Mechanics: Principle of Effective Stress, Capillarity and Permeability On SoilDokumen54 halamanSoil Mechanics: Principle of Effective Stress, Capillarity and Permeability On SoilAwadhiBelum ada peringkat

- Feminism in Lucia SartoriDokumen41 halamanFeminism in Lucia SartoriRaraBelum ada peringkat

- ESG Module 2 1 32Dokumen33 halamanESG Module 2 1 32salamat lang akinBelum ada peringkat

- Training of Local Government Personnel PHDokumen5 halamanTraining of Local Government Personnel PHThea ConsBelum ada peringkat

- Perilaku Ramah Lingkungan Peserta Didik Sma Di Kota BandungDokumen11 halamanPerilaku Ramah Lingkungan Peserta Didik Sma Di Kota Bandungnurulhafizhah01Belum ada peringkat

- CA - Indonesia Digital Business Trend Final 2 Agust 2017Dokumen38 halamanCA - Indonesia Digital Business Trend Final 2 Agust 2017silver8700Belum ada peringkat

- Hospitality Marketing Management PDFDokumen642 halamanHospitality Marketing Management PDFMuhamad Armawaddin100% (6)

- BSD ReviewerDokumen17 halamanBSD ReviewerMagelle AgbalogBelum ada peringkat

- A Review Article On Integrator Circuits Using Various Active DevicesDokumen7 halamanA Review Article On Integrator Circuits Using Various Active DevicesRaja ChandruBelum ada peringkat

- Midland County Board of Commissioners Dec. 19, 2023Dokumen26 halamanMidland County Board of Commissioners Dec. 19, 2023Isabelle PasciollaBelum ada peringkat

- Climbing KnotsDokumen40 halamanClimbing KnotsIvan Vitez100% (11)

- The Wavy Tunnel: Trade Management Jody SamuelsDokumen40 halamanThe Wavy Tunnel: Trade Management Jody SamuelsPeter Nguyen100% (1)

- Jason Payne-James, Ian Wall, Peter Dean-Medicolegal Essentials in Healthcare (2004)Dokumen284 halamanJason Payne-James, Ian Wall, Peter Dean-Medicolegal Essentials in Healthcare (2004)Abdalmonem Albaz100% (1)

- ACCOUNTING FOR SPECIAL EDUCATION FUNDSDokumen12 halamanACCOUNTING FOR SPECIAL EDUCATION FUNDSIrdo KwanBelum ada peringkat