Anda mungkin juga menyukai

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (119)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (587)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2219)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (894)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (73)

- Torts & Damages 2013 Case SummariesDokumen364 halamanTorts & Damages 2013 Case SummariesJose Roco100% (5)

- Note Purchase Agreement Template - 1Dokumen16 halamanNote Purchase Agreement Template - 1David Jay Mor100% (2)

- Accounting TransactionsDokumen28 halamanAccounting TransactionsPaolo100% (1)

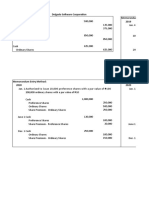

- Memorandum and Journal Entry Methods for Share Capital TransactionsDokumen3 halamanMemorandum and Journal Entry Methods for Share Capital TransactionsFeiya Liu100% (1)

- Bliss v. California Coop ProducersDokumen1 halamanBliss v. California Coop ProducersTrinca DiplomaBelum ada peringkat

- Epc Contracts in The Power SectorDokumen30 halamanEpc Contracts in The Power SectorIwan Anggara100% (2)

- Behavioral FinanceDokumen184 halamanBehavioral FinanceSatya ReddyBelum ada peringkat

- Chavez Vs PEA Case DigestDokumen3 halamanChavez Vs PEA Case Digestfjl_302711100% (5)

- Rules and regulations for electric power industry reformDokumen100 halamanRules and regulations for electric power industry reformBong PerezBelum ada peringkat

- Equitable PCI Bank Liable for Manager's CheckDokumen2 halamanEquitable PCI Bank Liable for Manager's CheckAntonJohnVincentFrias100% (2)

- Due - Diligence ChecklistDokumen4 halamanDue - Diligence ChecklistAndrew D. WalcottBelum ada peringkat

- 17 Measuring European Competitiveness Sectoral Level Collignon Esposito Web VersionDokumen143 halaman17 Measuring European Competitiveness Sectoral Level Collignon Esposito Web VersionChin TecsonBelum ada peringkat

- Exchange of Notes - MDBDokumen4 halamanExchange of Notes - MDBChin TecsonBelum ada peringkat

- Bankabilityandepccontractingmarch 20190021553008939620Dokumen45 halamanBankabilityandepccontractingmarch 20190021553008939620Chin TecsonBelum ada peringkat

- Mutual Defense Treaty Between The United States and The Republic of The Philippines August 30, 1951Dokumen1 halamanMutual Defense Treaty Between The United States and The Republic of The Philippines August 30, 1951Chin TecsonBelum ada peringkat

- HB5060 - National ID System PDFDokumen10 halamanHB5060 - National ID System PDFChin TecsonBelum ada peringkat

- 2013 Revised JV GuidelinesDokumen18 halaman2013 Revised JV GuidelinesChin TecsonBelum ada peringkat

- SiaHuatCatalogue2017 2018Dokumen350 halamanSiaHuatCatalogue2017 2018Chin TecsonBelum ada peringkat

- Land Titles Reviewer Chapter 10 13Dokumen29 halamanLand Titles Reviewer Chapter 10 13Chin TecsonBelum ada peringkat

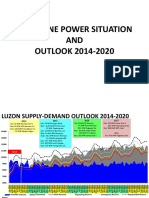

- Doe Power Outlook 10282014 LMP MindanaoDokumen31 halamanDoe Power Outlook 10282014 LMP MindanaoChin TecsonBelum ada peringkat

- Manager Managed Operating Agreement Long FormDokumen13 halamanManager Managed Operating Agreement Long FormChin TecsonBelum ada peringkat

- Comments On IMF Natural ResourcesDokumen9 halamanComments On IMF Natural ResourcesChin TecsonBelum ada peringkat

- Guidelines ITParksCentersDokumen11 halamanGuidelines ITParksCentersKim Roque-AquinoBelum ada peringkat

- EDD.1.I.003 - Tourism Economic ZoneDokumen1 halamanEDD.1.I.003 - Tourism Economic ZoneChin TecsonBelum ada peringkat

- Primer PDFDokumen81 halamanPrimer PDFAtty MglrtBelum ada peringkat

- Corporation Code of The PhilippinesDokumen64 halamanCorporation Code of The PhilippinesChin TecsonBelum ada peringkat

- The 2011 Investment Priorities PlanDokumen10 halamanThe 2011 Investment Priorities PlanChin TecsonBelum ada peringkat

- Financial Regulation 01 Introduction Notes 20170818 Parab PDFDokumen15 halamanFinancial Regulation 01 Introduction Notes 20170818 Parab PDFNisarg SavlaBelum ada peringkat

- Adani EnterprisesDokumen1 halamanAdani EnterprisesDebjit SenguptaBelum ada peringkat

- 08 Risk Management QuestionnaireDokumen7 halaman08 Risk Management QuestionnaireBhupendra ThakurBelum ada peringkat

- English For BusinessDokumen40 halamanEnglish For BusinessSyavina Haidar AlatasBelum ada peringkat

- L1R41 - Annotated - LiveDokumen52 halamanL1R41 - Annotated - LiveAlex PaulBelum ada peringkat

- Blackbook Project On Ipo in India 163420179Dokumen153 halamanBlackbook Project On Ipo in India 163420179Saad HamidaniBelum ada peringkat

- SRSAcquiom 2023 Deal Terms StudyDokumen112 halamanSRSAcquiom 2023 Deal Terms StudyDan XiangBelum ada peringkat

- Quiz Chapter 1 Introduction To Corporate FinanceDokumen16 halamanQuiz Chapter 1 Introduction To Corporate FinanceRosiana TharobBelum ada peringkat

- Issue of FCCBs and Ordinary Shares Scheme 1993Dokumen11 halamanIssue of FCCBs and Ordinary Shares Scheme 1993shashasyBelum ada peringkat

- Real Estate Weekly Newsletter Highlights Key Industry UpdatesDokumen27 halamanReal Estate Weekly Newsletter Highlights Key Industry UpdatesAayushi AroraBelum ada peringkat

- Valuation PPT 2Dokumen8 halamanValuation PPT 2vinay.rathore.che21Belum ada peringkat

- Money Supply - IndiaDokumen20 halamanMoney Supply - IndiaShrey SampatBelum ada peringkat

- Advanced Corporate Finance Module-Student EditionDokumen60 halamanAdvanced Corporate Finance Module-Student EditionDavid Mavodo100% (2)

- Assignment AFMDokumen13 halamanAssignment AFMKibrom GmichaelBelum ada peringkat

- Why I Am Leaving Goldman Sachs EthicsDokumen3 halamanWhy I Am Leaving Goldman Sachs EthicsChan CkBelum ada peringkat

- Copy of Summer Internship Project ReportDokumen28 halamanCopy of Summer Internship Project ReportSandeep SharmaBelum ada peringkat

- Case StudyDokumen7 halamanCase StudyPatricia TabalonBelum ada peringkat

- Chapter Two The Financial System2 - Eco551Dokumen25 halamanChapter Two The Financial System2 - Eco551Hafiz akbarBelum ada peringkat

- Mergers Acquisitions in IndiaDokumen162 halamanMergers Acquisitions in Indiashivam_2607Belum ada peringkat

- Capital Budgeting TechniquesDokumen2 halamanCapital Budgeting TechniquesmananipratikBelum ada peringkat

- LATAM AIRLINES GROUP S A 09-2012 (Inglés)Dokumen172 halamanLATAM AIRLINES GROUP S A 09-2012 (Inglés)chequeadoBelum ada peringkat

- Money Monster (Reaction Paper)Dokumen1 halamanMoney Monster (Reaction Paper)Kersteen JoyBelum ada peringkat

- Entepreneurship 5 Business ImplementationDokumen12 halamanEntepreneurship 5 Business ImplementationErick John ChicoBelum ada peringkat