Anda mungkin juga menyukai

- Bookkeeping In Quickbooks Online (Bookkeeping & Accounting)Dari EverandBookkeeping In Quickbooks Online (Bookkeeping & Accounting)Belum ada peringkat

- Calculate Cash BudgetDokumen4 halamanCalculate Cash BudgetArul Ambalavanan ThenappenBelum ada peringkat

- Fixed Income Analytics: Pricing And Risk ManagementDari EverandFixed Income Analytics: Pricing And Risk ManagementBelum ada peringkat

- Working Capital ManagementDokumen32 halamanWorking Capital ManagementrutikaBelum ada peringkat

- Takt Time - Understanding the Core Principle of Lean Manufacturing: Toyota Production System ConceptsDari EverandTakt Time - Understanding the Core Principle of Lean Manufacturing: Toyota Production System ConceptsPenilaian: 5 dari 5 bintang5/5 (1)

- Profit Planning Budgets ExplainedDokumen80 halamanProfit Planning Budgets ExplainedAliya UmairBelum ada peringkat

- 1S5 Tarea Set B FinzsDokumen8 halaman1S5 Tarea Set B Finzsnelson gymBelum ada peringkat

- WORKING CAPITAL ManagementDokumen22 halamanWORKING CAPITAL ManagementPrajwal BhattBelum ada peringkat

- AFN0005Dokumen4 halamanAFN0005AiDLoBelum ada peringkat

- Working Capital Management PDFDokumen46 halamanWorking Capital Management PDFNizar AhamedBelum ada peringkat

- Working Capital Management - 131218Dokumen39 halamanWorking Capital Management - 131218bhumika manwaniBelum ada peringkat

- Working Capital ProblemsDokumen3 halamanWorking Capital ProblemsSayonarababayBelum ada peringkat

- Working Capital ManagementDokumen16 halamanWorking Capital ManagementdhruvBelum ada peringkat

- Unit 7 Working Capital ManagementDokumen36 halamanUnit 7 Working Capital ManagementNabin JoshiBelum ada peringkat

- Working CapitalDokumen14 halamanWorking CapitalLavi VermaBelum ada peringkat

- FM5.5 Estimating WC RequirementDokumen18 halamanFM5.5 Estimating WC RequirementAbdulraqeeb AlareqiBelum ada peringkat

- UNIT-4 Working Capital ManagementDokumen13 halamanUNIT-4 Working Capital ManagementChandanN81Belum ada peringkat

- Working Capital CycleDokumen2 halamanWorking Capital CycleManish Kumar MasramBelum ada peringkat

- Cost II Chap3Dokumen11 halamanCost II Chap3abelBelum ada peringkat

- Working Capital ManagementDokumen32 halamanWorking Capital ManagementAkash RanjanBelum ada peringkat

- Aggregate PlanningDokumen19 halamanAggregate PlanningPiyush MathurBelum ada peringkat

- Management Accounting Problem Unit 3Dokumen17 halamanManagement Accounting Problem Unit 3princeBelum ada peringkat

- Lec 28Dokumen20 halamanLec 28Aman PotdarBelum ada peringkat

- Working CapitalDokumen61 halamanWorking CapitalSharmistha Banerjee100% (1)

- Working Capital RequirementDokumen20 halamanWorking Capital RequirementKrishnakant Mishra100% (1)

- Financial Analysis & Management: NPV, IRR, Profitability, LiquidityDokumen9 halamanFinancial Analysis & Management: NPV, IRR, Profitability, LiquiditySanch TursunovBelum ada peringkat

- Working Capital PlanningDokumen4 halamanWorking Capital PlanningAkshata ShrivastavaBelum ada peringkat

- Working Capital RequirementDokumen20 halamanWorking Capital Requirementflashsd3000Belum ada peringkat

- Estimation ProcessDokumen33 halamanEstimation ProcessMd. Mokbul HossainBelum ada peringkat

- Corporate FinanceDokumen6 halamanCorporate Financejayesh jhaBelum ada peringkat

- Chapter 3 - Financial Statement AnalysisDokumen22 halamanChapter 3 - Financial Statement AnalysisReyes JonahBelum ada peringkat

- Working Capital ManagementDokumen2 halamanWorking Capital ManagementShaikh GM33% (3)

- Master BudgetingDokumen89 halamanMaster BudgetingDeep AroraBelum ada peringkat

- Unit II - CFDokumen26 halamanUnit II - CFuser 02Belum ada peringkat

- A Budgetary Control Systems Accounting EssayDokumen9 halamanA Budgetary Control Systems Accounting EssayHND Assignment HelpBelum ada peringkat

- Estimating working capital requirementsDokumen21 halamanEstimating working capital requirementsLakhan Sharma100% (1)

- 21444working CapitalDokumen8 halaman21444working CapitalSaurabh JohriBelum ada peringkat

- Managing Cash, Receivables and InventoryDokumen4 halamanManaging Cash, Receivables and InventoryEduardo Jr. LleveBelum ada peringkat

- AcctgDokumen6 halamanAcctgJulien Elisse Santiago DullasBelum ada peringkat

- Prepare Cash Budget and Flexible BudgetDokumen6 halamanPrepare Cash Budget and Flexible BudgetShridhara ShriBelum ada peringkat

- Working Capital ManagementDokumen98 halamanWorking Capital ManagementGanesh PatashalaBelum ada peringkat

- Financial Decision AnalysisDokumen10 halamanFinancial Decision AnalysisGyanendra SinghBelum ada peringkat

- Cost Accounting Assignment QuestionsDokumen8 halamanCost Accounting Assignment Questionspritika mishraBelum ada peringkat

- 4 FM AssignmentDokumen3 halaman4 FM AssignmentGorav BhallaBelum ada peringkat

- Working CapitalDokumen22 halamanWorking CapitalASHWINI SINHABelum ada peringkat

- Operating CycleDokumen2 halamanOperating CyclemsiskatemwaBelum ada peringkat

- Master Budgeting Guide for BeginnersDokumen8 halamanMaster Budgeting Guide for BeginnersMon RamBelum ada peringkat

- Document 8Dokumen3 halamanDocument 8Ashish AgarwalBelum ada peringkat

- Estimating Working CapitalDokumen36 halamanEstimating Working CapitalKylaa Angelica de LeonBelum ada peringkat

- Seminar 11answer Group 11Dokumen115 halamanSeminar 11answer Group 11Shweta SridharBelum ada peringkat

- Profit Planning, Activity-Based Budgeting and E-Budgeting: Mcgraw-Hill/IrwinDokumen71 halamanProfit Planning, Activity-Based Budgeting and E-Budgeting: Mcgraw-Hill/IrwinSambit DashBelum ada peringkat

- Dibin K K Assistant ProfessorDokumen69 halamanDibin K K Assistant ProfessorKartika Bhuvaneswaran NairBelum ada peringkat

- Chap 009 Managerial Accounting HiltonDokumen50 halamanChap 009 Managerial Accounting Hiltonkaseb100% (1)

- Module 4 - Working Capital ManagementDokumen23 halamanModule 4 - Working Capital Managementhats300972Belum ada peringkat

- Lesson 10 Improving Cash FlowDokumen38 halamanLesson 10 Improving Cash FlowPaulinaBelum ada peringkat

- Working Capital NumericalsDokumen3 halamanWorking Capital NumericalsShriya SajeevBelum ada peringkat

- Aggregate ProductionDokumen5 halamanAggregate ProductionAlfania FrimaBelum ada peringkat

- Group Incentive PlansDokumen3 halamanGroup Incentive PlansAnukrati BagherwalBelum ada peringkat

- Working Capital Management: Amity Business SchoolDokumen26 halamanWorking Capital Management: Amity Business SchoolRitika SharmaBelum ada peringkat

- Working Capital Manageme NTDokumen66 halamanWorking Capital Manageme NTcmsundaram82Belum ada peringkat

- Techno India Group Public School, Jalpaiguri List of Prescribed Books Class - IDokumen11 halamanTechno India Group Public School, Jalpaiguri List of Prescribed Books Class - ISimul MondalBelum ada peringkat

- 100 Fruits and Veggies PDFDokumen4 halaman100 Fruits and Veggies PDFAnonymous HXLczq3Belum ada peringkat

- Https WWW - Drishtiias.com Daily-Updates Daily-News-Analysis Acharya-Prafulla-Chandra-Ray Print ManuallyDokumen3 halamanHttps WWW - Drishtiias.com Daily-Updates Daily-News-Analysis Acharya-Prafulla-Chandra-Ray Print ManuallySimul MondalBelum ada peringkat

- Trigonometry: x y 1 y x sinθ + cosθ =, find sinθ - cosθ a b 2 b aDokumen1 halamanTrigonometry: x y 1 y x sinθ + cosθ =, find sinθ - cosθ a b 2 b aSimul MondalBelum ada peringkat

- Article Questions For SSC PDFDokumen6 halamanArticle Questions For SSC PDFWishbone DealBelum ada peringkat

- Trigonometry: 2tana 1 + Tan ADokumen2 halamanTrigonometry: 2tana 1 + Tan ASimul MondalBelum ada peringkat

- Selina Concise Geography Solutions Class 9 Chapter 6 RocksDokumen20 halamanSelina Concise Geography Solutions Class 9 Chapter 6 RocksSimul MondalBelum ada peringkat

- 100 Fruits and Veggies PDFDokumen4 halaman100 Fruits and Veggies PDFAnonymous HXLczq3Belum ada peringkat

- Selina Concise Geography Solutions Class 9 Chapter 8 EarthquakesDokumen9 halamanSelina Concise Geography Solutions Class 9 Chapter 8 EarthquakesSimul MondalBelum ada peringkat

- 1537177499-0llcomputer Applications ICSE 9th Answer PDFDokumen207 halaman1537177499-0llcomputer Applications ICSE 9th Answer PDFSonu Mishra100% (1)

- Class Ix Biology: SCIENCE Paper - 3Dokumen10 halamanClass Ix Biology: SCIENCE Paper - 3sharathBelum ada peringkat

- Online Grammar Test QuestionsDokumen129 halamanOnline Grammar Test QuestionsSimul Mondal100% (1)

- P44800781176512082021075630Dokumen1 halamanP44800781176512082021075630Simul MondalBelum ada peringkat

- English Worksheets Class 1 Nouns Plurals Verbs Adjectives and PunctuationDokumen6 halamanEnglish Worksheets Class 1 Nouns Plurals Verbs Adjectives and Punctuationbc140400424 Asma IqbalBelum ada peringkat

- 12 Money: Coins Currently in Use in IndiaDokumen6 halaman12 Money: Coins Currently in Use in IndiaSimul MondalBelum ada peringkat

- 9 Data Handling: Count The Shapes in The Above PictureDokumen2 halaman9 Data Handling: Count The Shapes in The Above PictureSimul MondalBelum ada peringkat

- 3 Addition: One MoreDokumen10 halaman3 Addition: One MoreDip KunduBelum ada peringkat

- Numbers From Twenty-One To Fifty: Fill in The BlanksDokumen5 halamanNumbers From Twenty-One To Fifty: Fill in The BlanksSimul MondalBelum ada peringkat

- Vocabulary and idioms with "blueDokumen10 halamanVocabulary and idioms with "blueSimul MondalBelum ada peringkat

- 100 Golden Rules of English GrammarDokumen23 halaman100 Golden Rules of English GrammarVenu GopalBelum ada peringkat

- English 2nd 17Dokumen8 halamanEnglish 2nd 17sharad dsouzaBelum ada peringkat

- Sl. No. Name of Examination Tier/Phase Date of Advt. Closing Date Date of ExamDokumen2 halamanSl. No. Name of Examination Tier/Phase Date of Advt. Closing Date Date of Examnl vinay kumarBelum ada peringkat

- Chapter3 PDFDokumen9 halamanChapter3 PDFAdithyan GowthamBelum ada peringkat

- RMHF 4 FormDokumen5 halamanRMHF 4 FormSimul MondalBelum ada peringkat

- NCERT Solutions For Class 4 EVS Chapter 2Dokumen9 halamanNCERT Solutions For Class 4 EVS Chapter 2Simul MondalBelum ada peringkat

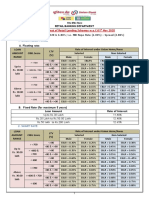

- ROI OnretaillendingschemesDokumen4 halamanROI OnretaillendingschemesNavdeep GoelBelum ada peringkat

- Tips and shortcuts for solving Linear equationsDokumen11 halamanTips and shortcuts for solving Linear equationsSimul MondalBelum ada peringkat

- Self Declaration From ShareholderDokumen2 halamanSelf Declaration From ShareholderSimul MondalBelum ada peringkat

- Mixture and Alligation: Yadav Sir"Dokumen11 halamanMixture and Alligation: Yadav Sir"Simul MondalBelum ada peringkat

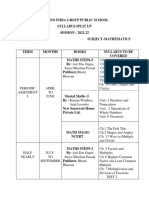

- Tech India Group Public School Maths Syllabus 2021-22Dokumen3 halamanTech India Group Public School Maths Syllabus 2021-22Simul MondalBelum ada peringkat

- Notes in Business CombinationDokumen5 halamanNotes in Business CombinationEllen BuenafeBelum ada peringkat

- Fundamental Equity Analysis - QMS Advisors HDAX FlexIndex 110Dokumen227 halamanFundamental Equity Analysis - QMS Advisors HDAX FlexIndex 110Q.M.S Advisors LLCBelum ada peringkat

- CPA Review School of the Philippines Final Pre-board ExaminationDokumen67 halamanCPA Review School of the Philippines Final Pre-board ExaminationCykee Hanna Quizo Lumongsod100% (1)

- Profitability of NBLDokumen56 halamanProfitability of NBLpavel108012Belum ada peringkat

- SEC 320 Midterm ExamDokumen3 halamanSEC 320 Midterm ExamDeVryHelpBelum ada peringkat

- 2019 Ncaa Eada Report Kent StateDokumen80 halaman2019 Ncaa Eada Report Kent StateMatt BrownBelum ada peringkat

- Avon Powerpoint PresentationDokumen22 halamanAvon Powerpoint PresentationOana TrutaBelum ada peringkat

- Cost of Goods Sold Problems PDF 1 3Dokumen3 halamanCost of Goods Sold Problems PDF 1 3Janine padronesBelum ada peringkat

- Chapter 7 (Pindyck)Dokumen31 halamanChapter 7 (Pindyck)Rahul SinhaBelum ada peringkat

- Three Main Reasons For PlanningDokumen28 halamanThree Main Reasons For PlanningXhaBelum ada peringkat

- Akanksha - Indirect Tax ProjectDokumen15 halamanAkanksha - Indirect Tax Projectakanksha singh0% (1)

- Your College Budget AssignmentDokumen8 halamanYour College Budget Assignmentlatorrem6457100% (1)

- Wild Wood Case StudyDokumen6 halamanWild Wood Case Studyaudrey gadayBelum ada peringkat

- Income Statement TutorialDokumen5 halamanIncome Statement TutorialKhiren MenonBelum ada peringkat

- Chart of Accounts: 1 1 - AssetsDokumen5 halamanChart of Accounts: 1 1 - AssetsSebastianDjoniBelum ada peringkat

- Project ReportDokumen2 halamanProject ReportTeja PalankiBelum ada peringkat

- ITC E-ChoupalDokumen23 halamanITC E-ChoupalRick Ganguly100% (1)

- Peligrino Vs PeopleDokumen15 halamanPeligrino Vs PeopleEj AquinoBelum ada peringkat

- Assignment 1Dokumen8 halamanAssignment 1Gerson GloreBelum ada peringkat

- 272 M S Q MDokumen2 halaman272 M S Q MAdnan AzizBelum ada peringkat

- Chapter-2 - Dividend DecisionsDokumen54 halamanChapter-2 - Dividend DecisionsRaunak YadavBelum ada peringkat

- Ravi Pay SlipsDokumen3 halamanRavi Pay SlipsAnonymous CsD87Y7Belum ada peringkat

- Jawaban Soal Uas AklDokumen13 halamanJawaban Soal Uas AklAnggari SaputraBelum ada peringkat

- Facebook Financial AnalysisDokumen12 halamanFacebook Financial AnalysisKennedy Gitonga ArithiBelum ada peringkat

- SITXFIN009 Assessment C Bistro Reports V1Dokumen3 halamanSITXFIN009 Assessment C Bistro Reports V1Sylovecy EXoBelum ada peringkat

- WalthamMotors CaseAnalysisDokumen9 halamanWalthamMotors CaseAnalysisabeeju100% (5)

- Dividend Policy Insights for Maximizing Firm ValueDokumen16 halamanDividend Policy Insights for Maximizing Firm Valuestillwinms100% (3)

- Version 2309Dokumen1 halamanVersion 2309kevin cosnerBelum ada peringkat

- Power and Process of Distrain-Final Version April 2017Dokumen73 halamanPower and Process of Distrain-Final Version April 2017Samuel Oyenitun100% (1)

- Problems Discontinued, Acctg Changes, Interim, Opseg, Correction of ErrorDokumen21 halamanProblems Discontinued, Acctg Changes, Interim, Opseg, Correction of ErrorMmBelum ada peringkat