Anda mungkin juga menyukai

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- DBMS MCQsDokumen14 halamanDBMS MCQsgurusodhiiBelum ada peringkat

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- Os MCQDokumen21 halamanOs MCQgurusodhiiBelum ada peringkat

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- Searching and Sorting ProgramsDokumen11 halamanSearching and Sorting ProgramsgurusodhiiBelum ada peringkat

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- V21 ExerciseMast PDFDokumen328 halamanV21 ExerciseMast PDFgurusodhiiBelum ada peringkat

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- Solved MCQs On Computer NetworkingDokumen10 halamanSolved MCQs On Computer NetworkinggurusodhiiBelum ada peringkat

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- Wrapper ClassDokumen6 halamanWrapper ClassgurusodhiiBelum ada peringkat

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- Solved Mcqs On SQLDokumen11 halamanSolved Mcqs On SQLgurusodhiiBelum ada peringkat

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- MS Word 2007 Practical Notes - 08!09!2014Dokumen21 halamanMS Word 2007 Practical Notes - 08!09!2014gurusodhiiBelum ada peringkat

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- Wrapper ClassDokumen6 halamanWrapper ClassgurusodhiiBelum ada peringkat

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (74)

- How To Access Google Sheet Data Using The Python API and Convert To Pandas DataframeDokumen5 halamanHow To Access Google Sheet Data Using The Python API and Convert To Pandas DataframegurusodhiiBelum ada peringkat

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- Relational Algebra NewDokumen42 halamanRelational Algebra NewgurusodhiiBelum ada peringkat

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Usbvirusfolderundelete 111110021717 Phpapp02 PDFDokumen2 halamanUsbvirusfolderundelete 111110021717 Phpapp02 PDFgurusodhiiBelum ada peringkat

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- SM Tutorial Sheet-2Dokumen2 halamanSM Tutorial Sheet-2gurusodhii0% (1)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- SM Tutorial Sheet-1Dokumen1 halamanSM Tutorial Sheet-1gurusodhiiBelum ada peringkat

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (345)

- Ms Excel MCQDokumen25 halamanMs Excel MCQgurusodhiiBelum ada peringkat

- Emails From Financial Ombudsman Service Patrick Hurley in Service Complaint About Steve Thomas To The Chief ExecutiveDokumen4 halamanEmails From Financial Ombudsman Service Patrick Hurley in Service Complaint About Steve Thomas To The Chief Executivesol3k0Belum ada peringkat

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- Os9 Bab60 1a SoftwDokumen80 halamanOs9 Bab60 1a Softwgarysun585Belum ada peringkat

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

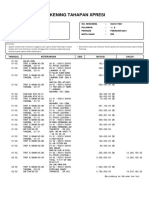

- Rekening Tahapan Xpresi: No. Rekening: 0541317821 Halaman: Periode: Februari 2021 Mata Uang: IDRDokumen6 halamanRekening Tahapan Xpresi: No. Rekening: 0541317821 Halaman: Periode: Februari 2021 Mata Uang: IDRRifaLutfiHabibiBelum ada peringkat

- Nokia Unicast GuideDokumen282 halamanNokia Unicast GuideDibyam baralBelum ada peringkat

- K300 ML1400 Indexing Example v1 - 0Dokumen7 halamanK300 ML1400 Indexing Example v1 - 0Emanuel Falcon100% (1)

- Addons Mozilla Org Fa Firefox Addon Save As PDFDokumen4 halamanAddons Mozilla Org Fa Firefox Addon Save As PDFHamid hamidBelum ada peringkat

- IoT Chap2Dokumen15 halamanIoT Chap2Yahya BouslimiBelum ada peringkat

- ControlRepeater Panel M 4 - 3Dokumen4 halamanControlRepeater Panel M 4 - 3georgeBelum ada peringkat

- SECURE10LGDokumen150 halamanSECURE10LGAzzafirBelum ada peringkat

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- CorrectivePreventive Action Request (CPAR) RegistryDokumen7 halamanCorrectivePreventive Action Request (CPAR) RegistryManz ManingoBelum ada peringkat

- AzureDokumen19 halamanAzureEdgar Orlando Bermudez Aljuri100% (1)

- CISSP SG Telecommunications and Network SecurityDokumen120 halamanCISSP SG Telecommunications and Network Securitydkdel0046Belum ada peringkat

- 1d04d Compal LA-8392P (Satellite P850 P855)Dokumen51 halaman1d04d Compal LA-8392P (Satellite P850 P855)albugBelum ada peringkat

- How To Identify and Diagnose Fan Failures On Sun SPARC Enterprise T5120/T5140/T5220/T5240/T5440 and Netra T5220/T5440Dokumen4 halamanHow To Identify and Diagnose Fan Failures On Sun SPARC Enterprise T5120/T5140/T5220/T5240/T5440 and Netra T5220/T5440cresmakBelum ada peringkat

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- EN-User Manual of DS-8000-S Series Net DVR PDFDokumen161 halamanEN-User Manual of DS-8000-S Series Net DVR PDFsilictronicBelum ada peringkat

- Edu en Vsicm8 LabDokumen167 halamanEdu en Vsicm8 Labadsf1150Belum ada peringkat

- Computer ServicingDokumen30 halamanComputer ServicingJhon Keneth NamiasBelum ada peringkat

- 307usb Ti08Dokumen2 halaman307usb Ti08Salvador ZafraBelum ada peringkat

- BSR64K Instalation Guide PDFDokumen134 halamanBSR64K Instalation Guide PDFValerio BitontiBelum ada peringkat

- Tecnomatix System Maintenance GuideDokumen68 halamanTecnomatix System Maintenance GuideDomingo GarcíaBelum ada peringkat

- Configuring Clocking and TimingDokumen52 halamanConfiguring Clocking and Timingreza_azadBelum ada peringkat

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- HP Firmware PDFDokumen18 halamanHP Firmware PDFSubodh SaharanBelum ada peringkat

- Security System For DNS Using CryptographyDokumen7 halamanSecurity System For DNS Using CryptographyAbhinavSinghBelum ada peringkat

- Using ADS8410/13 in Daisy-Chain Mode: Application ReportDokumen36 halamanUsing ADS8410/13 in Daisy-Chain Mode: Application ReportBalan PalaniappanBelum ada peringkat

- Database Security AssignmentDokumen7 halamanDatabase Security AssignmentAamir Raza100% (2)

- Outline: Parallel Database SystemsDokumen48 halamanOutline: Parallel Database SystemsHarshini TataBelum ada peringkat

- Arduino MatterDokumen7 halamanArduino MatterChemudupati SunilBelum ada peringkat

- Towards Pentesting Automation Using The Metasploit FrameworkDokumen8 halamanTowards Pentesting Automation Using The Metasploit FrameworkYusuf KılıçBelum ada peringkat

- SQL User GuideDokumen176 halamanSQL User GuideStef EnigmeBelum ada peringkat

- Oce TDS 600 Ozalit MakinasiDokumen4 halamanOce TDS 600 Ozalit MakinasigenisformatBelum ada peringkat

- Laws of UX: Using Psychology to Design Better Products & ServicesDari EverandLaws of UX: Using Psychology to Design Better Products & ServicesPenilaian: 5 dari 5 bintang5/5 (9)