Anda mungkin juga menyukai

- Tajikistan: Promoting Export Diversification and GrowthDari EverandTajikistan: Promoting Export Diversification and GrowthBelum ada peringkat

- A Study of Relationship Between FDI Inflow and Economic Growth in IndiaDokumen6 halamanA Study of Relationship Between FDI Inflow and Economic Growth in IndiaSubrat JainBelum ada peringkat

- Various Countries Foreign Direct Investment (Fdi) in India and Its Impact On Gross Domestic Production (GDP) of IndiaDokumen11 halamanVarious Countries Foreign Direct Investment (Fdi) in India and Its Impact On Gross Domestic Production (GDP) of IndiaIAEME PublicationBelum ada peringkat

- A Study of Foreign Direct Investment (FDI) On Manufacturing Industry in India: An Emerging Economic Opportunity of GDP Growth and ChallengesDokumen4 halamanA Study of Foreign Direct Investment (FDI) On Manufacturing Industry in India: An Emerging Economic Opportunity of GDP Growth and ChallengesPranathi DivakarBelum ada peringkat

- Foreign Direct Investment and The Make in India Initiative: A Comprehensive Analysis of The Impact On India'S Economy and Industrial SectorsDokumen5 halamanForeign Direct Investment and The Make in India Initiative: A Comprehensive Analysis of The Impact On India'S Economy and Industrial SectorsYashaswi KumarBelum ada peringkat

- What Is Today'S Topic? 0P6Qik9CDokumen23 halamanWhat Is Today'S Topic? 0P6Qik9CAshish kumar NairBelum ada peringkat

- Advantages and Disadvantages of FdiDokumen10 halamanAdvantages and Disadvantages of Fdibiswarup deyBelum ada peringkat

- v10n1 Paper05Dokumen3 halamanv10n1 Paper05Mrudula R GowdaBelum ada peringkat

- The Role of Foreign Direct Investment (FDI) in India-An OverviewDokumen10 halamanThe Role of Foreign Direct Investment (FDI) in India-An OverviewLikesh Kumar MNBelum ada peringkat

- An Analysisof Employmentand Investment Opportunitiesin Various Indian Statesin IndiaDokumen12 halamanAn Analysisof Employmentand Investment Opportunitiesin Various Indian Statesin IndiaRAJENDRA BALOTIYABelum ada peringkat

- Performance of Fdi in Automobile Sector - 1Dokumen6 halamanPerformance of Fdi in Automobile Sector - 1Vibin VibinBelum ada peringkat

- 1 PBDokumen8 halaman1 PBArefin karimBelum ada peringkat

- Fdi in IndiaDokumen10 halamanFdi in IndiaROHITH S 22MIB051Belum ada peringkat

- Foreign Direct Investment in IndiaDokumen6 halamanForeign Direct Investment in IndiaIOSRjournalBelum ada peringkat

- IJCRT2208295Dokumen5 halamanIJCRT2208295Ashraaf AhmadBelum ada peringkat

- Authors: 1. Dr. Parimal Kr. SenDokumen8 halamanAuthors: 1. Dr. Parimal Kr. SenDebojyoti DasBelum ada peringkat

- An Empirical Study On Fdi Inflows in Indian It and Ites SectorDokumen8 halamanAn Empirical Study On Fdi Inflows in Indian It and Ites SectorTJPRC PublicationsBelum ada peringkat

- 1.time Series Analysis of Inward Foreign Direct Investment Function in MalaysiaDokumen7 halaman1.time Series Analysis of Inward Foreign Direct Investment Function in MalaysiaAzan RasheedBelum ada peringkat

- Impact of FDIDokumen8 halamanImpact of FDIAnonymous mzuRnewGBelum ada peringkat

- Foreign Direct Investment (FDI) in India: A Review: January 2019Dokumen14 halamanForeign Direct Investment (FDI) in India: A Review: January 2019Kaushal NahataBelum ada peringkat

- GRP 10 Project FinalDokumen31 halamanGRP 10 Project Finalfatmaiffat111Belum ada peringkat

- Necessity of Domestic Institutional Investors (DIIS) in Indian Stock MarketDokumen4 halamanNecessity of Domestic Institutional Investors (DIIS) in Indian Stock MarketAniket SenBelum ada peringkat

- DOI: Http://ijmer - In.doi./2021/10.07.122 Article Received: 4 July Publication Date:30 July 2021Dokumen7 halamanDOI: Http://ijmer - In.doi./2021/10.07.122 Article Received: 4 July Publication Date:30 July 2021Sayyed Mustafa Kalaam RazviBelum ada peringkat

- GRP 10 ProjectDokumen31 halamanGRP 10 Projectfatmaiffat111Belum ada peringkat

- (Approved by AICTE, New Delhi & Affiliated To Rajasthan Technical University, KotaDokumen13 halaman(Approved by AICTE, New Delhi & Affiliated To Rajasthan Technical University, KotaNeelu Tuteja NikhanjBelum ada peringkat

- SECTORWISEINFLOWOFFOREIGNDIRECTINVESTMENTININDIA1Dokumen9 halamanSECTORWISEINFLOWOFFOREIGNDIRECTINVESTMENTININDIA1Aditi KulkarniBelum ada peringkat

- GBR - Saileja SsDokumen17 halamanGBR - Saileja Ssrohan mohapatraBelum ada peringkat

- Ijcrt 192619Dokumen11 halamanIjcrt 192619Yashaswi KumarBelum ada peringkat

- Sectorwise Investment in IndiaDokumen10 halamanSectorwise Investment in IndiadinuindiaBelum ada peringkat

- Does Inward FDI Lead To Export Performance in India? An Empirical InvestigationDokumen16 halamanDoes Inward FDI Lead To Export Performance in India? An Empirical InvestigationRamya PichiBelum ada peringkat

- Determinates of Foreign Direct Investment: An Empirical Study On IndiaDokumen9 halamanDeterminates of Foreign Direct Investment: An Empirical Study On IndiaMilind Kumar SinghBelum ada peringkat

- Impact of Foreign Direct Investment On Indian Economy: December 2013Dokumen6 halamanImpact of Foreign Direct Investment On Indian Economy: December 2013pandurang parkarBelum ada peringkat

- Tourism Investments 2013-2021-Ver.2 FinalDokumen11 halamanTourism Investments 2013-2021-Ver.2 FinalDr. George M. JonesBelum ada peringkat

- A Study On Impact of Make in India On Employment, G.D.P Growth and Eodb IndexDokumen11 halamanA Study On Impact of Make in India On Employment, G.D.P Growth and Eodb Indexthega leesanBelum ada peringkat

- Impact of Foreign Direct Investment On Industrial Growth of IndiaDokumen6 halamanImpact of Foreign Direct Investment On Industrial Growth of IndiaCLIND MBBelum ada peringkat

- Fdi in India - CimDokumen49 halamanFdi in India - CimVivek RathodBelum ada peringkat

- To Identify The Challenges and Opportunities Faced by Startups in IndiaDokumen10 halamanTo Identify The Challenges and Opportunities Faced by Startups in IndiaYash JaiswalBelum ada peringkat

- Research Paper On Fdi in IndiaDokumen8 halamanResearch Paper On Fdi in Indiantjjkmrhf100% (1)

- Impact of FDI On Performance of Banks in India: R.V.NaveenanDokumen5 halamanImpact of FDI On Performance of Banks in India: R.V.NaveenanR.v. NaveenanBelum ada peringkat

- Project 1Dokumen20 halamanProject 1pandurang parkarBelum ada peringkat

- A Study On Impact of Make in India' Initiative On Fdi Inflows in IndiaDokumen7 halamanA Study On Impact of Make in India' Initiative On Fdi Inflows in IndiabablujsrBelum ada peringkat

- Foreign Direct InvestmentDokumen11 halamanForeign Direct InvestmentSuraj SinghBelum ada peringkat

- Foreign Direct Investment in India Research PaperDokumen6 halamanForeign Direct Investment in India Research Papergz8zw71w100% (1)

- Ijmss: Keywords: Balance Sheet, Profit and Loss Account, Financial RatiosDokumen7 halamanIjmss: Keywords: Balance Sheet, Profit and Loss Account, Financial RatiosAbhimanyu Narayan RaiBelum ada peringkat

- New FdiDokumen6 halamanNew FdiBhanu TejaBelum ada peringkat

- Fin542 - Group 2 - Assignment 1 - Rba2423aDokumen12 halamanFin542 - Group 2 - Assignment 1 - Rba2423aZAINOOR IKMAL MAISARAH MOHAMAD NOORBelum ada peringkat

- 7.Hum-A Study of Economics Implications of Foreign Direct Investment in IndiaDokumen10 halaman7.Hum-A Study of Economics Implications of Foreign Direct Investment in IndiaImpact JournalsBelum ada peringkat

- Special Economic Zones (SEZ) and Their Role and Impact On Indian EconomyDokumen12 halamanSpecial Economic Zones (SEZ) and Their Role and Impact On Indian Economypdc2121Belum ada peringkat

- Goel Et Al.Dokumen13 halamanGoel Et Al.dhruv khandelwalBelum ada peringkat

- International Business: Submitted To - Dr. Halaswamy DDokumen8 halamanInternational Business: Submitted To - Dr. Halaswamy DRohan KashyapBelum ada peringkat

- 5Dokumen15 halaman5balwantBelum ada peringkat

- Foreign Direct Investment Determinants in The Manufacturing Sectors in MalaysiaDokumen14 halamanForeign Direct Investment Determinants in The Manufacturing Sectors in MalaysiaGlobal Research and Development ServicesBelum ada peringkat

- IMPACT of FDI IN INDIADokumen17 halamanIMPACT of FDI IN INDIABharathyBelum ada peringkat

- Fdi in India Literature ReviewDokumen5 halamanFdi in India Literature Reviewgvyns594100% (1)

- Fdi in IndiaDokumen17 halamanFdi in IndiachaitanyaBelum ada peringkat

- Current Status of FdiDokumen9 halamanCurrent Status of FdiGrishma KothariBelum ada peringkat

- Impact of Macroeconomic Determinants On Economic Growth in India: An Empirical AssessmentDokumen6 halamanImpact of Macroeconomic Determinants On Economic Growth in India: An Empirical AssessmentManagement Journal for Advanced ResearchBelum ada peringkat

- Flowof Financetothe MSMEDokumen10 halamanFlowof Financetothe MSMEVikas RanaBelum ada peringkat

- Dissertation On Fdi in IndiaDokumen4 halamanDissertation On Fdi in IndiaWriteMyPaperOneDayCanada100% (1)

- Fdi ShortDokumen15 halamanFdi Shortaman vermaBelum ada peringkat

- Chap 3 MCDokumen29 halamanChap 3 MCIlyas SadvokassovBelum ada peringkat

- Cost AccountingDokumen2 halamanCost AccountingLouina YnciertoBelum ada peringkat

- L7 Cost Management PDFDokumen85 halamanL7 Cost Management PDFhalia bonjoBelum ada peringkat

- The Great South African Land ScandalDokumen158 halamanThe Great South African Land ScandalTinyiko S. MalulekeBelum ada peringkat

- Sbi Po QTN and AnsDokumen6 halamanSbi Po QTN and AnsMALOTH BABU RAOBelum ada peringkat

- Malabon AIP 2014+amendments PDFDokumen81 halamanMalabon AIP 2014+amendments PDFCorics HerbuelaBelum ada peringkat

- Adriana Cisneros and Gustavo Cisneros - Bloomberg InterviewDokumen5 halamanAdriana Cisneros and Gustavo Cisneros - Bloomberg InterviewAdriana CisnerosBelum ada peringkat

- Real Estate Player in BangaloreDokumen20 halamanReal Estate Player in BangaloreAnkit GoelBelum ada peringkat

- Account Statement From 3 Nov 2020 To 3 May 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDokumen8 halamanAccount Statement From 3 Nov 2020 To 3 May 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceRajwinder SandhuBelum ada peringkat

- Viney - Financial Markets and InstitutionsDokumen37 halamanViney - Financial Markets and InstitutionsVilas ShenoyBelum ada peringkat

- Everything To Know About Customer Lifetime Value - Ebook PDFDokumen28 halamanEverything To Know About Customer Lifetime Value - Ebook PDFNishi GoyalBelum ada peringkat

- Forum Educacao Dakar 2000Dokumen78 halamanForum Educacao Dakar 2000Dulce CostaBelum ada peringkat

- September October LD Debate Kritik (Neg)Dokumen5 halamanSeptember October LD Debate Kritik (Neg)RhuiedianBelum ada peringkat

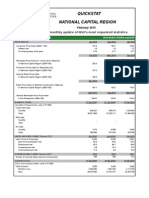

- Quickstat National Capital Region: A Monthly Update of NSO's Most Requested StatisticsDokumen3 halamanQuickstat National Capital Region: A Monthly Update of NSO's Most Requested StatisticsDaniel John Cañares LegaspiBelum ada peringkat

- T1 General PDFDokumen4 halamanT1 General PDFbatmanbittuBelum ada peringkat

- Foreign Trade: Ricardian ModelDokumen11 halamanForeign Trade: Ricardian Modelellenam23Belum ada peringkat

- Solution Manual For Macroeconomics For Today 10th Edition Irvin B TuckerDokumen6 halamanSolution Manual For Macroeconomics For Today 10th Edition Irvin B TuckerKelly Pena100% (31)

- Social Integration Approaches and Issues, UNRISD Publication (1994)Dokumen16 halamanSocial Integration Approaches and Issues, UNRISD Publication (1994)United Nations Research Institute for Social DevelopmentBelum ada peringkat

- Globalization and The Sociology of Immanuel Wallerstein: A Critical AppraisalDokumen23 halamanGlobalization and The Sociology of Immanuel Wallerstein: A Critical AppraisalMario__7Belum ada peringkat

- Profile Guide: Corrugated Sheet & Foam FillersDokumen275 halamanProfile Guide: Corrugated Sheet & Foam FillersnguyenanhtuanbBelum ada peringkat

- Sinar Mas: Introduction To and Overview ofDokumen26 halamanSinar Mas: Introduction To and Overview ofBayuBelum ada peringkat

- Asian PaintsDokumen13 halamanAsian PaintsGOPS000Belum ada peringkat

- Bilo GraphyDokumen9 halamanBilo Graphyvimalvijayan89Belum ada peringkat

- Lec 3 Central Problems of Every Economic SocietyDokumen16 halamanLec 3 Central Problems of Every Economic SocietyJutt TheMagicianBelum ada peringkat

- Level 2 Los 2018Dokumen46 halamanLevel 2 Los 2018Loan HuynhBelum ada peringkat

- CBR ProcterGamble 06Dokumen2 halamanCBR ProcterGamble 06Kuljeet Kaur ThethiBelum ada peringkat

- Capital Weekly 018 OnlineDokumen20 halamanCapital Weekly 018 OnlineBelize ConsulateBelum ada peringkat

- IET Educational (Xiao-Ping Zhang)Dokumen17 halamanIET Educational (Xiao-Ping Zhang)Mayita ContrerasBelum ada peringkat

- Spot THE Error: Detai L Ed Expl Anati OnDokumen131 halamanSpot THE Error: Detai L Ed Expl Anati OnopprakasBelum ada peringkat

- 2023 Nigerian Capital Market UpdateDokumen13 halaman2023 Nigerian Capital Market Updatemay izinyonBelum ada peringkat

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisDari EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisPenilaian: 5 dari 5 bintang5/5 (6)

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNDari Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNPenilaian: 4.5 dari 5 bintang4.5/5 (3)

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursDari EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursPenilaian: 4.5 dari 5 bintang4.5/5 (8)

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingDari EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingPenilaian: 4.5 dari 5 bintang4.5/5 (17)

- Finance Basics (HBR 20-Minute Manager Series)Dari EverandFinance Basics (HBR 20-Minute Manager Series)Penilaian: 4.5 dari 5 bintang4.5/5 (32)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaDari EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (14)

- The Caesars Palace Coup: How a Billionaire Brawl Over the Famous Casino Exposed the Power and Greed of Wall StreetDari EverandThe Caesars Palace Coup: How a Billionaire Brawl Over the Famous Casino Exposed the Power and Greed of Wall StreetPenilaian: 5 dari 5 bintang5/5 (2)

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelDari Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelBelum ada peringkat

- Ready, Set, Growth hack:: A beginners guide to growth hacking successDari EverandReady, Set, Growth hack:: A beginners guide to growth hacking successPenilaian: 4.5 dari 5 bintang4.5/5 (93)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialDari EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialPenilaian: 4.5 dari 5 bintang4.5/5 (32)

- The 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamDari EverandThe 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamBelum ada peringkat

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanDari EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanPenilaian: 4.5 dari 5 bintang4.5/5 (79)

- Financial Risk Management: A Simple IntroductionDari EverandFinancial Risk Management: A Simple IntroductionPenilaian: 4.5 dari 5 bintang4.5/5 (7)

- Venture Deals: Be Smarter Than Your Lawyer and Venture CapitalistDari EverandVenture Deals: Be Smarter Than Your Lawyer and Venture CapitalistPenilaian: 4 dari 5 bintang4/5 (32)

- Startup CEO: A Field Guide to Scaling Up Your Business (Techstars)Dari EverandStartup CEO: A Field Guide to Scaling Up Your Business (Techstars)Penilaian: 4.5 dari 5 bintang4.5/5 (4)

- Venture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistDari EverandVenture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistPenilaian: 4.5 dari 5 bintang4.5/5 (73)

- Private Equity and Venture Capital in Europe: Markets, Techniques, and DealsDari EverandPrivate Equity and Venture Capital in Europe: Markets, Techniques, and DealsPenilaian: 5 dari 5 bintang5/5 (1)

- Joy of Agility: How to Solve Problems and Succeed SoonerDari EverandJoy of Agility: How to Solve Problems and Succeed SoonerPenilaian: 4 dari 5 bintang4/5 (1)

- Value: The Four Cornerstones of Corporate FinanceDari EverandValue: The Four Cornerstones of Corporate FinancePenilaian: 4.5 dari 5 bintang4.5/5 (18)

- Investment Valuation: Tools and Techniques for Determining the Value of any Asset, University EditionDari EverandInvestment Valuation: Tools and Techniques for Determining the Value of any Asset, University EditionPenilaian: 5 dari 5 bintang5/5 (1)

- Creating Shareholder Value: A Guide For Managers And InvestorsDari EverandCreating Shareholder Value: A Guide For Managers And InvestorsPenilaian: 4.5 dari 5 bintang4.5/5 (8)

- How to Measure Anything: Finding the Value of Intangibles in BusinessDari EverandHow to Measure Anything: Finding the Value of Intangibles in BusinessPenilaian: 3.5 dari 5 bintang3.5/5 (4)

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursDari EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursPenilaian: 4.5 dari 5 bintang4.5/5 (34)

- Financial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityDari EverandFinancial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityPenilaian: 4.5 dari 5 bintang4.5/5 (4)

- Other People's Money: The Real Business of FinanceDari EverandOther People's Money: The Real Business of FinancePenilaian: 4 dari 5 bintang4/5 (34)