Anda mungkin juga menyukai

- Solution Manual for an Introduction to Equilibrium ThermodynamicsDari EverandSolution Manual for an Introduction to Equilibrium ThermodynamicsBelum ada peringkat

- Week 2 LectureDokumen93 halamanWeek 2 LectureДмитрий КолесниковBelum ada peringkat

- Handbook of Capital Recovery (CR) Factors: European EditionDari EverandHandbook of Capital Recovery (CR) Factors: European EditionBelum ada peringkat

- Introduction To Finance: Blair RobertsonDokumen32 halamanIntroduction To Finance: Blair Robertsonharshit guptaBelum ada peringkat

- Unit III-B PMDokumen45 halamanUnit III-B PMAbdul AleemBelum ada peringkat

- Capital BudgetingDokumen28 halamanCapital Budgetingpgdm23samamalBelum ada peringkat

- Deterministic Cash-Flows: 1 Basic Theory of InterestDokumen16 halamanDeterministic Cash-Flows: 1 Basic Theory of InterestNaveen ReddyBelum ada peringkat

- Discounted Cash Flow ValuationDokumen33 halamanDiscounted Cash Flow ValuationShadow IpBelum ada peringkat

- Test 1Dokumen28 halamanTest 1Joseph J. AssafBelum ada peringkat

- How To Calculate Present Values?: Abhinav Anand (IIM Bangalore)Dokumen50 halamanHow To Calculate Present Values?: Abhinav Anand (IIM Bangalore)Gaurav SainiBelum ada peringkat

- Session 2-The Time Value of Money-Reminder SM 2022-23Dokumen42 halamanSession 2-The Time Value of Money-Reminder SM 2022-23Deborah KpeyeBelum ada peringkat

- Busn 233 CH 08Dokumen101 halamanBusn 233 CH 08Pramod VasudevBelum ada peringkat

- CH 04Dokumen12 halamanCH 04Jazzy PascualBelum ada peringkat

- What Is Capital Budgeting?Dokumen43 halamanWhat Is Capital Budgeting?anjanellaBelum ada peringkat

- Finanical Management Ch4Dokumen60 halamanFinanical Management Ch4Chucky ChungBelum ada peringkat

- 395 Midterm 1 Cheat SheetDokumen2 halaman395 Midterm 1 Cheat Sheetchrisjames20036Belum ada peringkat

- The Basics of Capital BudgetingDokumen39 halamanThe Basics of Capital BudgetingSeethalakshmy NagarajanBelum ada peringkat

- Slide 2Dokumen25 halamanSlide 2Akash SinghBelum ada peringkat

- Investment Appraisal: Methods of Capital Budgeting: Presented By: Shyam Kumar Mishra Sonia Gupta PGDM (Ib) 2008-2010Dokumen32 halamanInvestment Appraisal: Methods of Capital Budgeting: Presented By: Shyam Kumar Mishra Sonia Gupta PGDM (Ib) 2008-2010shyammishra2355Belum ada peringkat

- FinanceDokumen246 halamanFinanceLuis Munguía LandinBelum ada peringkat

- 01 V1 - 2016CFA一级强化班 - 数量组合经济学固收3Dokumen105 halaman01 V1 - 2016CFA一级强化班 - 数量组合经济学固收3Mario XieBelum ada peringkat

- Chapter 5Dokumen15 halamanChapter 5eclecticpandaBelum ada peringkat

- CH 04Dokumen12 halamanCH 04Mai NguyễnBelum ada peringkat

- Tvom PDFDokumen16 halamanTvom PDFgoyal_khushbu88Belum ada peringkat

- Ema Ge Berk CF 2GE SG 04Dokumen13 halamanEma Ge Berk CF 2GE SG 04Duygu ÇınarBelum ada peringkat

- Chapter 3 and 4Dokumen22 halamanChapter 3 and 4Eldar AlizadeBelum ada peringkat

- CHPT 05Dokumen40 halamanCHPT 05Anirban RoyBelum ada peringkat

- Chapter 2 - Time Value of Money and Its ApplicationDokumen69 halamanChapter 2 - Time Value of Money and Its ApplicationQUYÊN VŨ THỊ THUBelum ada peringkat

- IRR and NPV Conflict - IllustartionDokumen27 halamanIRR and NPV Conflict - IllustartionVaidyanathan RavichandranBelum ada peringkat

- RWJ Chapter 5 NPV and Other Investment RulesDokumen55 halamanRWJ Chapter 5 NPV and Other Investment RulesMinh Châu Tạ ThịBelum ada peringkat

- Profitability AnalysisDokumen24 halamanProfitability AnalysisAnonymous 1P14SXhUBelum ada peringkat

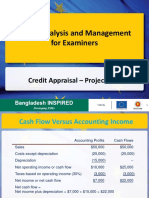

- Credit Analysis and Management For Examiners: Credit Appraisal - Project RiskDokumen17 halamanCredit Analysis and Management For Examiners: Credit Appraisal - Project RisksabetaliBelum ada peringkat

- Kewirausahaan Konsep-Konsep Keuangan: Dteti 2021Dokumen27 halamanKewirausahaan Konsep-Konsep Keuangan: Dteti 2021PANDHU ARDI PRASETYOBelum ada peringkat

- Hedging Interest Rate RiskDokumen14 halamanHedging Interest Rate RiskVictor ManuelBelum ada peringkat

- S 4,5 - Time Value of MoneyDokumen23 halamanS 4,5 - Time Value of MoneyAninda DuttaBelum ada peringkat

- Week 10 Basics-Of-Capital-BudgetingDokumen26 halamanWeek 10 Basics-Of-Capital-BudgetingQurat SaboorBelum ada peringkat

- Chapter 2 Principles of Corporate Finance PDFDokumen4 halamanChapter 2 Principles of Corporate Finance PDFchatuuuu123Belum ada peringkat

- Discounted Cash Flow ValuationDokumen35 halamanDiscounted Cash Flow ValuationRemonBelum ada peringkat

- 15.401 Recitation 15.401 Recitation: 1: Present ValueDokumen18 halaman15.401 Recitation 15.401 Recitation: 1: Present ValueDahagam SaumithBelum ada peringkat

- (ENG) Chuong 2 - Gia Tri Thoi Gian Cua Dong Tien Va Mo Hinh DCFDokumen25 halaman(ENG) Chuong 2 - Gia Tri Thoi Gian Cua Dong Tien Va Mo Hinh DCFHoài ThuBelum ada peringkat

- Yield RatesDokumen9 halamanYield RatesDoco OkaBelum ada peringkat

- PC10 - Investment CriteriaDokumen15 halamanPC10 - Investment CriteriaSyed InshanuzzamanBelum ada peringkat

- Class 4 AnswersDokumen4 halamanClass 4 AnswersБота ОмароваBelum ada peringkat

- Chapter 3 CLC StudentDokumen38 halamanChapter 3 CLC StudentLinh HoangBelum ada peringkat

- The Basics of Capital BudgetingDokumen55 halamanThe Basics of Capital BudgetingnewaznahianBelum ada peringkat

- Financial ModelingDokumen37 halamanFinancial ModelingSofoniasBelum ada peringkat

- Lecture - 02 The Time Value of MoneyDokumen41 halamanLecture - 02 The Time Value of Moneyanujgoyal31Belum ada peringkat

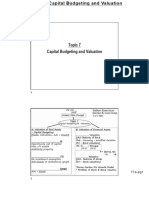

- 20220910171031HCTAN008C7a Topic7a Capital BudgetingDokumen53 halaman20220910171031HCTAN008C7a Topic7a Capital Budgetingnicholas wijayaBelum ada peringkat

- Lecture 4 INVESTMENT CRITERIA FOR PROJECT APPRAISALDokumen49 halamanLecture 4 INVESTMENT CRITERIA FOR PROJECT APPRAISALANH VÕ TỪBelum ada peringkat

- Selection of Useful FormulasDokumen3 halamanSelection of Useful FormulasМаша СкрипченкоBelum ada peringkat

- Capital BudgetingDokumen16 halamanCapital BudgetingMZK videosBelum ada peringkat

- Fina2303 Lecture - 4&5Dokumen14 halamanFina2303 Lecture - 4&5Delay NomoreBelum ada peringkat

- 05 Fin 502 Investment Decision RulesDokumen20 halaman05 Fin 502 Investment Decision RulesOSBelum ada peringkat

- Brealey - Principles of Corporate Finance - 13e - Chap05 - SMDokumen11 halamanBrealey - Principles of Corporate Finance - 13e - Chap05 - SMpt94jykqvqBelum ada peringkat

- Chapter3 EFA2 NPVDokumen29 halamanChapter3 EFA2 NPVDương DươngBelum ada peringkat

- Chapter 2Dokumen14 halamanChapter 2Kumar ShivamBelum ada peringkat

- BFLect FinMaths Answer SlidesDokumen22 halamanBFLect FinMaths Answer SlidesSheron Jude SeneviratneBelum ada peringkat

- 02 Bond FundamentalsDokumen4 halaman02 Bond Fundamentalstanya1jhaBelum ada peringkat

- Financial Management Assignment 2Dokumen6 halamanFinancial Management Assignment 2Sayaf ArbabBelum ada peringkat

- Chapter 8 - Capital Budgeting Analysis - NPV and Other MethodsDokumen71 halamanChapter 8 - Capital Budgeting Analysis - NPV and Other MethodsMadhav Chowdary TumpatiBelum ada peringkat

- Chapter-5: Statement of Cash FlowDokumen43 halamanChapter-5: Statement of Cash FlowBAM ZAHARDBelum ada peringkat

- Option Chain LogicDokumen20 halamanOption Chain LogicNitesh Singh0% (1)

- Lucio Tan Sells PNB Insurance Arm To German AllianzDokumen4 halamanLucio Tan Sells PNB Insurance Arm To German AllianzJoannah SalamatBelum ada peringkat

- Stories of Entrepreneurship: Case StudyDokumen13 halamanStories of Entrepreneurship: Case StudyUsman KhanBelum ada peringkat

- Mercury Athletic (Student Templates) FinalDokumen6 halamanMercury Athletic (Student Templates) FinalGarland GayBelum ada peringkat

- Info 7behavioral CEO S - The Role of Managerial Overconfidence 1Dokumen30 halamanInfo 7behavioral CEO S - The Role of Managerial Overconfidence 1Baddam Goutham ReddyBelum ada peringkat

- FAQ - Valaution PDFDokumen222 halamanFAQ - Valaution PDFhindustani888Belum ada peringkat

- Discount RatesDokumen14 halamanDiscount RatesAditya Kumar SinghBelum ada peringkat

- Employee Communication EffectivenessDokumen118 halamanEmployee Communication EffectivenessRaja Reddy100% (1)

- Tutorial 10 PFPDokumen6 halamanTutorial 10 PFPWinjie PangBelum ada peringkat

- Daily Edge 01122014Dokumen41 halamanDaily Edge 01122014Mad ViruzBelum ada peringkat

- Bindura Nickel Corporation Limited PDFDokumen1 halamanBindura Nickel Corporation Limited PDFBusiness Daily ZimbabweBelum ada peringkat

- Stock Market Debacle in BangladeshDokumen33 halamanStock Market Debacle in BangladeshFalguni Chowdhury100% (1)

- 9-Introduction To Capital MarketsDokumen3 halaman9-Introduction To Capital MarketsCharlesBelum ada peringkat

- Economics Report Group 4Dokumen14 halamanEconomics Report Group 4AKSHAY SURANA100% (1)

- Nestle Pakistan Limited Balance Sheet: 2020 2019 2018 Equity and Liabilities Share Capital and ReservesDokumen39 halamanNestle Pakistan Limited Balance Sheet: 2020 2019 2018 Equity and Liabilities Share Capital and ReservesFarah NazBelum ada peringkat

- Causes and Removal of Industrial Backwardness in PakistanDokumen19 halamanCauses and Removal of Industrial Backwardness in PakistanseemaaquaBelum ada peringkat

- Tata Steel's Acquisition of CorusDokumen6 halamanTata Steel's Acquisition of CorusHarshit GuptaBelum ada peringkat

- CHASE (Citizens For A Healthy and Safe Environment) vs. Green Energy Partners Part IIDokumen24 halamanCHASE (Citizens For A Healthy and Safe Environment) vs. Green Energy Partners Part IIViola DavisBelum ada peringkat

- GE 9 Cell MatrixDokumen10 halamanGE 9 Cell MatrixMr. M. Sandeep Kumar0% (1)

- Transmission PricingDokumen57 halamanTransmission PricingMuruganBelum ada peringkat

- Vizag-Chennai Industrial Corridor - Full ReportDokumen388 halamanVizag-Chennai Industrial Corridor - Full ReportPrasad GogineniBelum ada peringkat

- Introduction To Global Investment Banking - Merrill LynchDokumen28 halamanIntroduction To Global Investment Banking - Merrill LynchAlexander Junior Huayana Espinoza100% (2)

- Gigacampus Final ReportDokumen28 halamanGigacampus Final Reportmacao100Belum ada peringkat

- GEM3 Empirical NotesDokumen60 halamanGEM3 Empirical Notesxy053333Belum ada peringkat

- Notes Unit 1 - CH 1-EnterpriseDokumen7 halamanNotes Unit 1 - CH 1-Enterprisekhalid malikBelum ada peringkat

- GEM LOPEZ TransactionsDokumen12 halamanGEM LOPEZ TransactionsRon83% (6)

- Accounting DefinationsDokumen17 halamanAccounting DefinationsPbawal50% (2)

- Investor Presentation Feb 2019Dokumen26 halamanInvestor Presentation Feb 2019ROBINSON CHIRAN ACOSTA100% (1)

- Piercing The Corporate VeilDokumen40 halamanPiercing The Corporate VeilJacky WuBelum ada peringkat