Anda mungkin juga menyukai

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5795)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (74)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1091)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- The Accounting Cycle - Part1Dokumen12 halamanThe Accounting Cycle - Part1RaaiinaBelum ada peringkat

- Job Order Costing Practice Problem 1 Davis Manufacturing, Inc. 1994 Manufacturing Overhead BudgetDokumen8 halamanJob Order Costing Practice Problem 1 Davis Manufacturing, Inc. 1994 Manufacturing Overhead BudgetNessa MarasiganBelum ada peringkat

- Chapter 19Dokumen17 halamanChapter 19Rachel EnokouBelum ada peringkat

- Bab 2 MateriDokumen4 halamanBab 2 MateriAndikaBelum ada peringkat

- Test Bank For Management 3 e 3rd Edition Michael A Hitt Stewart Black Lyman W PorterDokumen24 halamanTest Bank For Management 3 e 3rd Edition Michael A Hitt Stewart Black Lyman W PorterStephanieRosemzdke100% (45)

- Part 2 - AccDokumen9 halamanPart 2 - AccSheikh Mass JahBelum ada peringkat

- Accounting For SalamDokumen19 halamanAccounting For SalamVani IndrawatiBelum ada peringkat

- User's Manual Adarian Money 5Dokumen62 halamanUser's Manual Adarian Money 5rdxqscBelum ada peringkat

- Corporate Tax PlanningDokumen85 halamanCorporate Tax PlanningLavi KambojBelum ada peringkat

- Advacc Quiz On PartnershipDokumen10 halamanAdvacc Quiz On PartnershipCzaeshel Edades0% (2)

- P43ADokumen5 halamanP43AAquanetta OrtonBelum ada peringkat

- Q 1 3Dokumen9 halamanQ 1 3Ahasanul AlamBelum ada peringkat

- ALABANG PLUMBING IntroDokumen1 halamanALABANG PLUMBING IntroIsa NgBelum ada peringkat

- Cogs FaqDokumen21 halamanCogs Faqthulasee77Belum ada peringkat

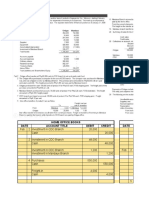

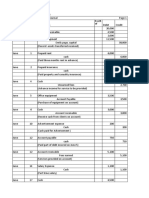

- Home Office Books Mandaue Books Date Account Title Debit Credit DateDokumen27 halamanHome Office Books Mandaue Books Date Account Title Debit Credit DateVon Andrei MedinaBelum ada peringkat

- ICAI - ICMAI - ICSI - Branch Accounting PDFDokumen5 halamanICAI - ICMAI - ICSI - Branch Accounting PDFRowdy RahulBelum ada peringkat

- Accounting Cycle Exercises IV PDFDokumen47 halamanAccounting Cycle Exercises IV PDFhansrajhans tBelum ada peringkat

- Non-Trading ConcernDokumen5 halamanNon-Trading ConcernveenaBelum ada peringkat

- DMGT104 Financial Accounting PDFDokumen317 halamanDMGT104 Financial Accounting PDFNani100% (1)

- D) Click Next at Account List Window E) Enter The Amount NextDokumen3 halamanD) Click Next at Account List Window E) Enter The Amount NextNoor Salehah100% (6)

- Using Sage 50 Accounting 2017 Canadian 1st Edition Purbhoo Test BankDokumen13 halamanUsing Sage 50 Accounting 2017 Canadian 1st Edition Purbhoo Test Bankmungoosemodus1qrzsk100% (25)

- Manage General Ledger BlueprintDokumen40 halamanManage General Ledger BlueprintOshinfowokan Ololade0% (1)

- CH 031Dokumen54 halamanCH 031ambermuBelum ada peringkat

- Supplier Business Plan 1Dokumen10 halamanSupplier Business Plan 1Bipana SapkotaBelum ada peringkat

- Shanti Gyan Niketan Sr. Sec. Public School Mid-Term Examination-2021-22 Accountancy (055) Class - XiDokumen9 halamanShanti Gyan Niketan Sr. Sec. Public School Mid-Term Examination-2021-22 Accountancy (055) Class - XiAnoop SinghBelum ada peringkat

- FM HLDokumen16 halamanFM HLhuleBelum ada peringkat

- ACC117-CON09 Module 3 ExamDokumen16 halamanACC117-CON09 Module 3 ExamMarlon LadesmaBelum ada peringkat

- Full Download Financial Accounting 10th Edition Weygandt Test BankDokumen24 halamanFull Download Financial Accounting 10th Edition Weygandt Test Bankjacobgrahamlet100% (32)

- Tutorial Test 2: Nicole ConsultingDokumen2 halamanTutorial Test 2: Nicole ConsultingTrinh Nguyen Linh ChiBelum ada peringkat

- Accounting For Government and Non-Profit Organization 3Dokumen11 halamanAccounting For Government and Non-Profit Organization 3accounting SolutionBelum ada peringkat