Anda mungkin juga menyukai

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5795)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (589)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (74)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1091)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- Quiz 1 - Semana 1 - PDFDokumen6 halamanQuiz 1 - Semana 1 - PDFLeonardo AlzateBelum ada peringkat

- Sample: Business Plan Business NameDokumen10 halamanSample: Business Plan Business NameDan688Belum ada peringkat

- Statement: Comprehensive IncomeDokumen11 halamanStatement: Comprehensive IncomeAngela Cuevas DimaanoBelum ada peringkat

- Chapter 4Dokumen50 halamanChapter 4andrea de capellaBelum ada peringkat

- Chapter 1 - Principles of FinanceDokumen12 halamanChapter 1 - Principles of FinancehtrucphuongBelum ada peringkat

- Intermediate Macroeconomics Sec 222Dokumen163 halamanIntermediate Macroeconomics Sec 222Katunga MwiyaBelum ada peringkat

- The Effect of Working Capital Management On ProfitDokumen12 halamanThe Effect of Working Capital Management On ProfitMirza Zain Ul AbideenBelum ada peringkat

- A Standard Unqualified Audit Report Indicates That The Opinion Expressed IsDokumen7 halamanA Standard Unqualified Audit Report Indicates That The Opinion Expressed IsAnkit KapoorBelum ada peringkat

- BitcoinDokumen20 halamanBitcoinSaloni Jain 1820343Belum ada peringkat

- Ekurhuleni North District Grade 7: Economic and Management SciencesDokumen9 halamanEkurhuleni North District Grade 7: Economic and Management SciencesMolemo S Masemula100% (6)

- Chapter 1 Partnerships Part 1Dokumen12 halamanChapter 1 Partnerships Part 1kevin royBelum ada peringkat

- R To JatDokumen2 halamanR To Jatbagdogra bagdograBelum ada peringkat

- Project Report On Personal Loan CompressDokumen62 halamanProject Report On Personal Loan CompressSudhakar GuntukaBelum ada peringkat

- Overview of Marine Insurance Law Prof. Dr. Marko PavlihaDokumen51 halamanOverview of Marine Insurance Law Prof. Dr. Marko PavlihasimranBelum ada peringkat

- Institute Progressive Tax Reform and More Effective Tax Collection, Indexing Taxes To Inflation. A Tax Reform Package Will Be Submitted To Congress by September 2016Dokumen28 halamanInstitute Progressive Tax Reform and More Effective Tax Collection, Indexing Taxes To Inflation. A Tax Reform Package Will Be Submitted To Congress by September 2016RAIZA GRACE OAMILBelum ada peringkat

- An Orientation of Gsis Membership, Benefits, Programs and LoansDokumen31 halamanAn Orientation of Gsis Membership, Benefits, Programs and LoansFrancis Ysabella BalagtasBelum ada peringkat

- Accounting For Merchandising Operations: Assignment Classification TableDokumen70 halamanAccounting For Merchandising Operations: Assignment Classification Table김재민Belum ada peringkat

- Bcom 314 Goldman Sachs Presentation 2Dokumen17 halamanBcom 314 Goldman Sachs Presentation 2api-486170232Belum ada peringkat

- Accounting ReviewerDokumen2 halamanAccounting ReviewerFranco Luis C. Mapua100% (4)

- Afisco Insurance CorpDokumen1 halamanAfisco Insurance CorpMarife MinorBelum ada peringkat

- Bank Ownership Reform and Bank Performance in China: Xiaochi Lin, Yi ZhangDokumen10 halamanBank Ownership Reform and Bank Performance in China: Xiaochi Lin, Yi ZhangdeaBelum ada peringkat

- ICMA ProfileDokumen41 halamanICMA Profilesarfraz ahmedBelum ada peringkat

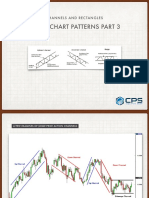

- Forex Chart Patterns Part 3: Channels and RectanglesDokumen10 halamanForex Chart Patterns Part 3: Channels and RectanglesJeremy NealBelum ada peringkat

- Analysis Investment Decision - IndiabullsDokumen72 halamanAnalysis Investment Decision - Indiabullssaiyuvatech100% (1)

- Housing Rent US CensusDokumen402 halamanHousing Rent US CensusMcKenzie StaufferBelum ada peringkat

- Department of Accountancy: Cash and Cash EquivalentsDokumen3 halamanDepartment of Accountancy: Cash and Cash EquivalentsAsterism LoneBelum ada peringkat

- Abc Analysis of Ca Final FR For May 2022 ExamsDokumen4 halamanAbc Analysis of Ca Final FR For May 2022 ExamsYuva LakshmiBelum ada peringkat

- Chapter 24 CVP - Break Even AnalysisDokumen58 halamanChapter 24 CVP - Break Even AnalysisShehryar Abdul SattarBelum ada peringkat

- Hindustan Colas (Hincol) : Bituminous Emulsion Price List Wef 01.12.21 Till Further Revision Ex - CHENNAIDokumen1 halamanHindustan Colas (Hincol) : Bituminous Emulsion Price List Wef 01.12.21 Till Further Revision Ex - CHENNAIveevimalBelum ada peringkat

- Advocates For Truth in Lending, Inc. vs. BSP, Et. Al. DigestDokumen2 halamanAdvocates For Truth in Lending, Inc. vs. BSP, Et. Al. Digestroquesa buray100% (1)