Anda mungkin juga menyukai

- Lab Expansion Proposal: Kwabena Osei & Tim TolinDokumen21 halamanLab Expansion Proposal: Kwabena Osei & Tim Tolinttolin03Belum ada peringkat

- Financial evaluation of property development projects using cash flow methodDokumen10 halamanFinancial evaluation of property development projects using cash flow methodLe Thi Anh TuyetBelum ada peringkat

- MegaPower Project Memo VfinalDokumen5 halamanMegaPower Project Memo VfinalSandra Sayarath AndersonBelum ada peringkat

- Banking Sector of Bangladesh: Course Instructor: Dr. Md. Kismatul AhsanDokumen10 halamanBanking Sector of Bangladesh: Course Instructor: Dr. Md. Kismatul AhsanSave PgcbBelum ada peringkat

- Illustration On Projects AppraisalDokumen6 halamanIllustration On Projects AppraisalAsmerom MosinehBelum ada peringkat

- Risk Analysis of Rivertype Hydropower PlantDokumen7 halamanRisk Analysis of Rivertype Hydropower PlantJhoni SitompulBelum ada peringkat

- General Foods' Super Project NPV AnalysisDokumen4 halamanGeneral Foods' Super Project NPV AnalysisAmeya KhaladkarBelum ada peringkat

- Handstar Case AnalysisDokumen4 halamanHandstar Case AnalysisarchaonscribdBelum ada peringkat

- The Investment Detective Answer Q1Dokumen4 halamanThe Investment Detective Answer Q1marco jeffBelum ada peringkat

- Case Assignment 8 - Diamond Energy Resources PDFDokumen3 halamanCase Assignment 8 - Diamond Energy Resources PDFAudrey Ang100% (1)

- Valuation of Himadri Specialty Chemical LTD.: Presented byDokumen11 halamanValuation of Himadri Specialty Chemical LTD.: Presented byArnab ChakrabortyBelum ada peringkat

- Aqua Bounty Harvard Business School Case N9-213-047 Courseware 9-213-701Dokumen3 halamanAqua Bounty Harvard Business School Case N9-213-047 Courseware 9-213-701Rishi RajBelum ada peringkat

- Investment Analysis (Part I) : Project Ranking Based On Simple Inspection of Cash FlowsDokumen5 halamanInvestment Analysis (Part I) : Project Ranking Based On Simple Inspection of Cash FlowsDivesha RaviBelum ada peringkat

- Project appraisal techniques analysisDokumen44 halamanProject appraisal techniques analysisRaghupathi Venkata SujathaBelum ada peringkat

- Powergrid Corporation of India history and financialsDokumen9 halamanPowergrid Corporation of India history and financialsShringar ThakkarBelum ada peringkat

- Mini Case Capital Budgeting ProcessDokumen6 halamanMini Case Capital Budgeting Process032179253460% (1)

- UtkarshVikramSinghChauhan TATASTEELDokumen12 halamanUtkarshVikramSinghChauhan TATASTEELUtkarsh VikramBelum ada peringkat

- Cost Planning and Cost Estimating: By: Engr. Nelson S. Tapsirul Bsce, Mba, MSCMDokumen22 halamanCost Planning and Cost Estimating: By: Engr. Nelson S. Tapsirul Bsce, Mba, MSCMNelson TapsirulBelum ada peringkat

- Evaluating Transport ProjectsDokumen28 halamanEvaluating Transport ProjectsGirmaye Kebede100% (1)

- Anand Kumar GourDokumen8 halamanAnand Kumar GourMayank ChoukseyBelum ada peringkat

- City of Fort St. John - 2023-2027 Operating BudgetDokumen30 halamanCity of Fort St. John - 2023-2027 Operating BudgetAlaskaHighwayNewsBelum ada peringkat

- ASS1Dokumen15 halamanASS1moezBelum ada peringkat

- Financial+Statements+ +indigo+Dokumen45 halamanFinancial+Statements+ +indigo+monami.sankarsanBelum ada peringkat

- CH 4Dokumen28 halamanCH 4Girmaye KebedeBelum ada peringkat

- Ch.1 - Introduction To Cost-Benefit Analysis - Class 2Dokumen20 halamanCh.1 - Introduction To Cost-Benefit Analysis - Class 2buthaina abdullahBelum ada peringkat

- and Shortage Administration Cost Per Unit CDokumen9 halamanand Shortage Administration Cost Per Unit CSơn Trần BảoBelum ada peringkat

- 2 Plenary - Introducing ADB by RSubramaniam Rev 22mar2017Dokumen22 halaman2 Plenary - Introducing ADB by RSubramaniam Rev 22mar2017Butch D. de la Cruz100% (2)

- MBA student report analyses investment projectsDokumen17 halamanMBA student report analyses investment projectsRegina AtkinsBelum ada peringkat

- Melrose Fiscal Year BudgetDokumen67 halamanMelrose Fiscal Year BudgetMike CarraggiBelum ada peringkat

- Financial Analysis of WSPsDokumen3 halamanFinancial Analysis of WSPsAnju KarkiBelum ada peringkat

- SRN: PES1PG20MB214 Name: Pooja V: Indian Mumbai Conglomerate Aditya Birla GroupDokumen4 halamanSRN: PES1PG20MB214 Name: Pooja V: Indian Mumbai Conglomerate Aditya Birla GroupPooja VBelum ada peringkat

- Globalizing the Cost of Capital and Capital Budgeting at AESDokumen13 halamanGlobalizing the Cost of Capital and Capital Budgeting at AESClaire Marie ThomasBelum ada peringkat

- Sapm AssignmentDokumen4 halamanSapm Assignment401-030 B. Harika bcom regBelum ada peringkat

- FMIBDokumen10 halamanFMIBVu Ngoc QuyBelum ada peringkat

- Prospective Analysis - ForecastingDokumen17 halamanProspective Analysis - ForecastingqueenbeeastBelum ada peringkat

- DCF Valuation of Media CompaniesDokumen35 halamanDCF Valuation of Media CompaniesArchit PateriaBelum ada peringkat

- IM - Cogent HRDokumen14 halamanIM - Cogent HRAaron WilsonBelum ada peringkat

- AES Case PresentationDokumen13 halamanAES Case PresentationClaire Marie Thomas67% (3)

- Fin 254 Part 3 2Dokumen6 halamanFin 254 Part 3 2wali6965Belum ada peringkat

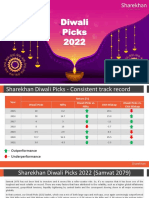

- DiwaliPicks2022 131022Dokumen22 halamanDiwaliPicks2022 131022tranganathanBelum ada peringkat

- Task 1 and Task 2Dokumen10 halamanTask 1 and Task 2Sarah BunoBelum ada peringkat

- 29116520Dokumen6 halaman29116520Rendy Setiadi MangunsongBelum ada peringkat

- Golden Tree Annual 2023 ENDokumen146 halamanGolden Tree Annual 2023 ENsteveBelum ada peringkat

- Project Report for Plastic Granules Production UnitDokumen14 halamanProject Report for Plastic Granules Production UnitMohit JainBelum ada peringkat

- NPV & IRR TemplateDokumen7 halamanNPV & IRR TemplateDimas AriotejoBelum ada peringkat

- Financial Statement Analysis of Samsung ElectronicsDokumen19 halamanFinancial Statement Analysis of Samsung ElectronicsSangita GautamBelum ada peringkat

- Analyzing Financial Statement of Vinamilk Group 2Dokumen24 halamanAnalyzing Financial Statement of Vinamilk Group 2Phan Thị Hương TrâmBelum ada peringkat

- Finance M-5Dokumen30 halamanFinance M-5Vrutika ShahBelum ada peringkat

- Project Risk Management-20188Dokumen39 halamanProject Risk Management-20188pragya budhathokiBelum ada peringkat

- Group 17 Magna International - FinalDokumen41 halamanGroup 17 Magna International - FinalLauren HoBelum ada peringkat

- Individual Report. MD - Najmul Islam, 201901019.Dokumen12 halamanIndividual Report. MD - Najmul Islam, 201901019.Najmul IslamBelum ada peringkat

- Lecture 1 Manufacturing Project Appraisal, Selection & FeasibilityDokumen41 halamanLecture 1 Manufacturing Project Appraisal, Selection & FeasibilityMuhammadBelum ada peringkat

- Presentation - New Earth Mining IncDokumen12 halamanPresentation - New Earth Mining IncShamsuzzaman SunBelum ada peringkat

- Study On PV System Development at UP Brantas For HDokumen5 halamanStudy On PV System Development at UP Brantas For HAdam SHBelum ada peringkat

- 01 Levelized Cost EnergyDokumen6 halaman01 Levelized Cost EnergySopanghadgeBelum ada peringkat

- Performance Analysis of Vishal Mega MartDokumen17 halamanPerformance Analysis of Vishal Mega Martsunnysonal_123Belum ada peringkat

- Group 1 Written Assignment V FIN C FIN304Dokumen15 halamanGroup 1 Written Assignment V FIN C FIN304Rajesh MongerBelum ada peringkat

- R Aditya Rayhan Zanesty - 29223341 - Entrepreneurship 26Dokumen41 halamanR Aditya Rayhan Zanesty - 29223341 - Entrepreneurship 26R. Aditya Rayhan ZanestyBelum ada peringkat

- Southeast Asia and the Economics of Global Climate StabilizationDari EverandSoutheast Asia and the Economics of Global Climate StabilizationBelum ada peringkat

- Handbook for Developing Joint Crediting Mechanism ProjectsDari EverandHandbook for Developing Joint Crediting Mechanism ProjectsBelum ada peringkat

- Distribution Earthing Systems in LVMV Networks (Design Instructions and Precautions)Dokumen10 halamanDistribution Earthing Systems in LVMV Networks (Design Instructions and Precautions)M iqbalBelum ada peringkat

- How To Find The Suitable Size of Cable & WireDokumen10 halamanHow To Find The Suitable Size of Cable & WireM iqbalBelum ada peringkat

- Concrete Mixer What Do These Machines Do, Their Types and Applications in ConstructionDokumen3 halamanConcrete Mixer What Do These Machines Do, Their Types and Applications in ConstructionM iqbalBelum ada peringkat

- 9 Crucial PM Do's for SuccessDokumen2 halaman9 Crucial PM Do's for SuccessM iqbalBelum ada peringkat

- 05 - External Wall InsulationDokumen5 halaman05 - External Wall InsulationM iqbalBelum ada peringkat

- 7 Project Management Skills That Have Been OverlookedDokumen3 halaman7 Project Management Skills That Have Been OverlookedM iqbalBelum ada peringkat

- 06 - Snagging A Self Builder's GuideDokumen2 halaman06 - Snagging A Self Builder's GuideM iqbalBelum ada peringkat

- Renovating a House Guide: Essentials for Your ProjectDokumen15 halamanRenovating a House Guide: Essentials for Your ProjectM iqbalBelum ada peringkat

- 02 - How To Find A Good Renovation Project (How To Assess A House For Renovation Potential)Dokumen9 halaman02 - How To Find A Good Renovation Project (How To Assess A House For Renovation Potential)M iqbalBelum ada peringkat

- Building Repair Techniques That Can Be Used To Repair Buildings and Restore Their Strength EffectivelyDokumen3 halamanBuilding Repair Techniques That Can Be Used To Repair Buildings and Restore Their Strength EffectivelyM iqbalBelum ada peringkat

- (Insert Project Name) (Insert Project Number)Dokumen21 halaman(Insert Project Name) (Insert Project Number)OPAZOSCBelum ada peringkat

- 15 Project Management Principles You Should KnowDokumen8 halaman15 Project Management Principles You Should KnowM iqbalBelum ada peringkat

- 7 Important Skills For Project ManagersDokumen5 halaman7 Important Skills For Project ManagersM iqbalBelum ada peringkat

- 7 Powerful Phrases Project Managers Use at WorkplaceDokumen3 halaman7 Powerful Phrases Project Managers Use at WorkplaceM iqbalBelum ada peringkat

- 6 Unexpected Project Manager Skills That Recruiters Look ForDokumen4 halaman6 Unexpected Project Manager Skills That Recruiters Look ForM iqbalBelum ada peringkat

- 7 Best Ways To Prepare Your Team For A ProjectDokumen3 halaman7 Best Ways To Prepare Your Team For A ProjectM iqbalBelum ada peringkat

- 6 Challenges Faced by Project ManagersDokumen4 halaman6 Challenges Faced by Project ManagersM iqbal100% (1)

- 7 Tips Effective Project Team CommunicationDokumen4 halaman7 Tips Effective Project Team CommunicationM iqbalBelum ada peringkat

- 5 Ways To Elevate Project Management Status in Your EnterpriseDokumen3 halaman5 Ways To Elevate Project Management Status in Your EnterpriseM iqbalBelum ada peringkat

- How To Use Rate Analysis of Brick Work Calculator Rate Analysis of Brick WorkDokumen7 halamanHow To Use Rate Analysis of Brick Work Calculator Rate Analysis of Brick WorkM iqbalBelum ada peringkat

- WBS - Market Research ProjectDokumen3 halamanWBS - Market Research ProjectM iqbalBelum ada peringkat

- Construction WBSDokumen1 halamanConstruction WBSM iqbalBelum ada peringkat

- WBS-Planning For A Trade ShowDokumen2 halamanWBS-Planning For A Trade ShowM iqbalBelum ada peringkat

- WBS The Solar Cell Work BreakdownDokumen2 halamanWBS The Solar Cell Work BreakdownM iqbalBelum ada peringkat

- Microsoft Project Training CourseDokumen8 halamanMicrosoft Project Training CourseM iqbalBelum ada peringkat

- Commercial Construction WBS BreakdownDokumen2 halamanCommercial Construction WBS BreakdownM iqbalBelum ada peringkat

- WBS Const SiteDokumen1 halamanWBS Const SiteM iqbalBelum ada peringkat

- Waste Water Treatment Plan Construction WBSDokumen1 halamanWaste Water Treatment Plan Construction WBSM iqbal100% (1)

- Infrastructure Deployment WBS Project PlanningDokumen2 halamanInfrastructure Deployment WBS Project PlanningM iqbalBelum ada peringkat

- WBS-Construction of A HouseDokumen1 halamanWBS-Construction of A HouseM iqbalBelum ada peringkat

- Chapter 10 FIXED INCOME SECURITIES PDFDokumen21 halamanChapter 10 FIXED INCOME SECURITIES PDFJinal SanghviBelum ada peringkat

- ES 5 - Template 1 and 2Dokumen4 halamanES 5 - Template 1 and 2ERIC DEL ROSARIOBelum ada peringkat

- Appraising A Project by Discounting and Non-Discounting CriteriaDokumen55 halamanAppraising A Project by Discounting and Non-Discounting CriteriaVaidyanathan Ravichandran100% (5)

- 6184-7 SupbDokumen17 halaman6184-7 SupbLibyaFlowerBelum ada peringkat

- Total (CF) 17,500,000.0 550,000 5,000,000 550,000 5,000,000 600,000 5,000,000 650,000 5,000,000 700,000 5,000,000 IRR Jumlah 4,450,000Dokumen5 halamanTotal (CF) 17,500,000.0 550,000 5,000,000 550,000 5,000,000 600,000 5,000,000 650,000 5,000,000 700,000 5,000,000 IRR Jumlah 4,450,000Devania PratiwiBelum ada peringkat

- School of Engineering & Technology: Sandip UniversityDokumen3 halamanSchool of Engineering & Technology: Sandip UniversityNavin JayswalBelum ada peringkat

- Profile V 1 0 1Dokumen5 halamanProfile V 1 0 1sarantceBelum ada peringkat

- Financial Profitability and Sensitivity Analysis oDokumen10 halamanFinancial Profitability and Sensitivity Analysis oMuhammad JunaidBelum ada peringkat

- Sneaker SolutionDokumen19 halamanSneaker SolutionSuperGuyBelum ada peringkat

- Fin Calc Guide GraphingDokumen49 halamanFin Calc Guide GraphingviktorBelum ada peringkat

- 05 Project EvaluationDokumen17 halaman05 Project EvaluationReiVan0% (1)

- Accounting and Finance MCQsDokumen50 halamanAccounting and Finance MCQsSathish Kumar MagapuBelum ada peringkat

- Topic 4 - Investment AppraisalDokumen46 halamanTopic 4 - Investment AppraisalmaureenBelum ada peringkat

- Mathematics of Finance and Investment GuideDokumen97 halamanMathematics of Finance and Investment GuideAlfred alegadoBelum ada peringkat

- Strategic Approach in Multi-Criteria Decision Making - A Practical Guide For Complex Scenarios (PDFDrive)Dokumen276 halamanStrategic Approach in Multi-Criteria Decision Making - A Practical Guide For Complex Scenarios (PDFDrive)majibBelum ada peringkat

- Department of Humanities and Social Sciences SyllabusDokumen60 halamanDepartment of Humanities and Social Sciences SyllabusRajput RishavBelum ada peringkat

- TDP-903 Life Cycle Costing For Hvac SystemsDokumen104 halamanTDP-903 Life Cycle Costing For Hvac SystemsAmr HeshamBelum ada peringkat

- F402 In-Class Exercise September 3, 2020Dokumen2 halamanF402 In-Class Exercise September 3, 2020Harrison GalavanBelum ada peringkat

- GGFPC Cassava Farming and Processing ProposalDokumen27 halamanGGFPC Cassava Farming and Processing ProposalprosperBelum ada peringkat

- Greenfield Trading LLC - Company ProfileDokumen49 halamanGreenfield Trading LLC - Company ProfileSikander Nawaz100% (2)

- Wipro's Financial Performance Comparison 2009-2010Dokumen46 halamanWipro's Financial Performance Comparison 2009-2010Abhishek KhareBelum ada peringkat

- Engineering EconomyDokumen42 halamanEngineering EconomyGodofredo Luayon Jipus Jr.Belum ada peringkat

- Venture Capital Vs Corporate VenturingDokumen2 halamanVenture Capital Vs Corporate VenturingRabia JamilBelum ada peringkat

- Capital Budgeting Sample Questions ExplainedDokumen2 halamanCapital Budgeting Sample Questions ExplainedNCTBelum ada peringkat

- Audit of Power Purchase AgreementsDokumen6 halamanAudit of Power Purchase AgreementsRochdi BahiriBelum ada peringkat

- Formula Sheet of AFBDokumen16 halamanFormula Sheet of AFBSAI TEJA NAIKBelum ada peringkat

- Business Decision MakingDokumen45 halamanBusiness Decision Makingsheran2350% (2)

- Module 2 Capital Budgeting Net Present Value and Other Investment CriteriaDokumen70 halamanModule 2 Capital Budgeting Net Present Value and Other Investment CriteriaJoyal jose100% (1)

- Cpa Review QuestionsDokumen81 halamanCpa Review QuestionsMJ YaconBelum ada peringkat

- VB6 Commands and FunctionsDokumen18 halamanVB6 Commands and FunctionsDumdum7Belum ada peringkat