Anda mungkin juga menyukai

- Admin Digest 2Dokumen10 halamanAdmin Digest 2rheyneBelum ada peringkat

- Donor's Tax-2Dokumen36 halamanDonor's Tax-2Razel Mhin MendozaBelum ada peringkat

- Chapter 1. Requisites of MarriageDokumen36 halamanChapter 1. Requisites of MarriageWagun Lobbangon BasungitBelum ada peringkat

- 24 Camp John Hay Development Corp. v. CBAA, 706 SCRA 547Dokumen2 halaman24 Camp John Hay Development Corp. v. CBAA, 706 SCRA 547Raymond MedinaBelum ada peringkat

- Mortgage On Condominium Units CasesDokumen34 halamanMortgage On Condominium Units CasesKatherine OlidanBelum ada peringkat

- Case FriaDokumen7 halamanCase FriaMichelle Marie TablizoBelum ada peringkat

- Lawyers League VsDokumen3 halamanLawyers League VsJuralexBelum ada peringkat

- Suspensive Vs ResolutoryDokumen14 halamanSuspensive Vs Resolutoryclifford tubanaBelum ada peringkat

- Transfer TaxesDokumen8 halamanTransfer TaxesMikee TanBelum ada peringkat

- Megaworld vs Tanseco Contract DisputeDokumen21 halamanMegaworld vs Tanseco Contract DisputeCattleyaBelum ada peringkat

- Larra Certificate of Decrease of Authorized Capital StockDokumen4 halamanLarra Certificate of Decrease of Authorized Capital StockKimberly PsychBelum ada peringkat

- 6.3 Villegas v. Hiu Chiong Tsai Hao PoDokumen7 halaman6.3 Villegas v. Hiu Chiong Tsai Hao PoGlenn Robin FedillagaBelum ada peringkat

- Person - Orporation: Income TaxDokumen138 halamanPerson - Orporation: Income TaxMich FelloneBelum ada peringkat

- Menzi and Co. v. BastidaDokumen1 halamanMenzi and Co. v. BastidaBless CarpenaBelum ada peringkat

- Benefits-Protection Theory Lorenzo V Posadas (Tax) : Double TaxationDokumen9 halamanBenefits-Protection Theory Lorenzo V Posadas (Tax) : Double Taxationkristel jane caldozaBelum ada peringkat

- Income Tax On Resident Foreign CorporationDokumen6 halamanIncome Tax On Resident Foreign CorporationElaiBelum ada peringkat

- Neeco I VS ErcDokumen2 halamanNeeco I VS Ercangelsu04Belum ada peringkat

- Rodriguez Vs PeopleDokumen2 halamanRodriguez Vs PeopleT Cel MrmgBelum ada peringkat

- The Warehouse Receipts LawDokumen62 halamanThe Warehouse Receipts LawPingotMagangaBelum ada peringkat

- Rodriguez Vs RodriguezDokumen2 halamanRodriguez Vs Rodriguezral cbBelum ada peringkat

- Sony Philippines tax disputeDokumen12 halamanSony Philippines tax disputeAnisah AquilaBelum ada peringkat

- Demurrer To Evidence: Rule 33Dokumen53 halamanDemurrer To Evidence: Rule 33MacBelum ada peringkat

- Request For SEBADokumen2 halamanRequest For SEBAEduard Loberez ReyesBelum ada peringkat

- Commercial Law Final Exam 2022 2023Dokumen2 halamanCommercial Law Final Exam 2022 2023Mary Nove PatanganBelum ada peringkat

- 13) DEUTCHE KNOWLEDGE Vs CIR - J Perlas - BernabeDokumen3 halaman13) DEUTCHE KNOWLEDGE Vs CIR - J Perlas - BernabejdonBelum ada peringkat

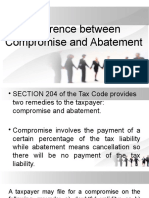

- Difference between Tax Compromise and AbatementDokumen3 halamanDifference between Tax Compromise and AbatementToni Ying100% (1)

- Rule 108 Petition for Cancellation or Correction of Civil Registry EntriesDokumen14 halamanRule 108 Petition for Cancellation or Correction of Civil Registry EntriesRPCO 4B PRDP IREAPBelum ada peringkat

- Admin Law Assignment #1 (Complete)Dokumen314 halamanAdmin Law Assignment #1 (Complete)Ýel ÄcedilloBelum ada peringkat

- Case Digest - Rabuco v. Villegas, G.R. Nos. L-24661, LDokumen3 halamanCase Digest - Rabuco v. Villegas, G.R. Nos. L-24661, LRichelle FabellonBelum ada peringkat

- Evidence 3dDokumen52 halamanEvidence 3dEmilio PahinaBelum ada peringkat

- Legal Counseling First Exam Reviewer PDFDokumen20 halamanLegal Counseling First Exam Reviewer PDFMadeleine DinoBelum ada peringkat

- Bank Secrecy Law ExplainedDokumen35 halamanBank Secrecy Law ExplainedGee GuevarraBelum ada peringkat

- General Bonded Warehouse ActDokumen3 halamanGeneral Bonded Warehouse ActFides DamascoBelum ada peringkat

- CIR Vs FBDCDokumen2 halamanCIR Vs FBDCCarmz SumileBelum ada peringkat

- CredTrans - Southern Motors V Barbosa - VilloncoDokumen2 halamanCredTrans - Southern Motors V Barbosa - VilloncoCHEENSBelum ada peringkat

- Local TaxationDokumen240 halamanLocal TaxationJulia Inez BlandoBelum ada peringkat

- RMC No. 32-2022Dokumen5 halamanRMC No. 32-2022Shiela Marie MaraonBelum ada peringkat

- Topic 12 Delgado and Lim PALE Report!Dokumen15 halamanTopic 12 Delgado and Lim PALE Report!Kwesi DelgadoBelum ada peringkat

- Land Titles 2nd Year End Lectures: Subsequent Registration and Voluntary/Involuntary DealingsDokumen72 halamanLand Titles 2nd Year End Lectures: Subsequent Registration and Voluntary/Involuntary DealingsLiz Zie100% (1)

- Real EstateDokumen8 halamanReal Estateeugzs109161Belum ada peringkat

- Affidavit - No Payment of Percentage TaxDokumen1 halamanAffidavit - No Payment of Percentage TaxRothea SimonBelum ada peringkat

- Alano v. Babasa - CaseDokumen4 halamanAlano v. Babasa - CaseRobehgene Atud-JavinarBelum ada peringkat

- Consumido V RosDokumen1 halamanConsumido V RosElaizza Concepcion0% (1)

- Gokongwei vs. SECDokumen45 halamanGokongwei vs. SECJimi SolomonBelum ada peringkat

- Bonifacio Cruz MemoDokumen7 halamanBonifacio Cruz MemoErgel Mae Encarnacion RosalBelum ada peringkat

- Lintag v. NPCDokumen1 halamanLintag v. NPCPrincess AyomaBelum ada peringkat

- Election Law CasesDokumen34 halamanElection Law CasesLizanne GauranaBelum ada peringkat

- MercmercDokumen3 halamanMercmercFely DesembranaBelum ada peringkat

- ADMIN 3.30.21 HighlitedDokumen64 halamanADMIN 3.30.21 HighlitedMarian's PreloveBelum ada peringkat

- Consent DecreeDokumen29 halamanConsent DecreeJermain GibsonBelum ada peringkat

- CIR v. Next Mobile IncDokumen11 halamanCIR v. Next Mobile IncPaulineBelum ada peringkat

- Capital Gains TaxDokumen3 halamanCapital Gains TaxAJ Santos100% (2)

- Aid Ofadmin Law Cases Other Powers Secretary of Justice Vs Judge Lantion-1Dokumen2 halamanAid Ofadmin Law Cases Other Powers Secretary of Justice Vs Judge Lantion-1Reb CustodioBelum ada peringkat

- TAXATION 1 - Hopewell Power V CommissionerDokumen3 halamanTAXATION 1 - Hopewell Power V CommissionerSuiBelum ada peringkat

- Sale of Delinquent Stock and Quorum RequirementsDokumen25 halamanSale of Delinquent Stock and Quorum RequirementsArrianne ObiasBelum ada peringkat

- People Vs TulaganDokumen50 halamanPeople Vs Tulaganbai malyanah a salmanBelum ada peringkat

- Bir Ruling 197-93 (May 7, 1993)Dokumen5 halamanBir Ruling 197-93 (May 7, 1993)matinikkiBelum ada peringkat

- Articles of Partnership Limited June2015Dokumen4 halamanArticles of Partnership Limited June2015Regina MuellerBelum ada peringkat

- CIR vs. Bank of Commerce (2005)Dokumen16 halamanCIR vs. Bank of Commerce (2005)BenBelum ada peringkat

- CIR v. Bank of Commerce (2005) Case DigestDokumen2 halamanCIR v. Bank of Commerce (2005) Case DigestShandrei GuevarraBelum ada peringkat

- AsfdafDokumen38 halamanAsfdafMikee RazonBelum ada peringkat

- Tax Bulletin Highlights June 2018Dokumen24 halamanTax Bulletin Highlights June 2018RhenfacelManlegroBelum ada peringkat

- 1 BIR List of Top Withholding Agents - ExistingDokumen31 halaman1 BIR List of Top Withholding Agents - ExistingMonica Soriano67% (3)

- Bir Registration RequirementsDokumen47 halamanBir Registration RequirementsYus CeballosBelum ada peringkat

- Tax BulletinDokumen16 halamanTax BulletinJohnny EspinosaBelum ada peringkat

- IAS 16 Property Plant and EquipmentDokumen13 halamanIAS 16 Property Plant and EquipmentLaura BalcanBelum ada peringkat

- 3 BIR List of Delisted Top Withholding AgentsDokumen9 halaman3 BIR List of Delisted Top Withholding AgentsMonica Soriano100% (1)

- TB July2018 ElecDokumen20 halamanTB July2018 ElecMonica SorianoBelum ada peringkat

- TB Aug2018 ElecDokumen22 halamanTB Aug2018 ElecMonica SorianoBelum ada peringkat

- Advisory-TWAs Final - OCt 1 2018 PDFDokumen1 halamanAdvisory-TWAs Final - OCt 1 2018 PDFNormi ZarateBelum ada peringkat

- Deductible Expense For Passive Income (CTA Case)Dokumen12 halamanDeductible Expense For Passive Income (CTA Case)Monica SorianoBelum ada peringkat

- Sec 127 (A) PDFDokumen1 halamanSec 127 (A) PDFMonica SorianoBelum ada peringkat

- SEC Opinion Rules-Governing-Redeemable-and-Treasury-Shares PDFDokumen2 halamanSEC Opinion Rules-Governing-Redeemable-and-Treasury-Shares PDFLarisa SerzoBelum ada peringkat

- Taxpayer Bill of Rights 2018Dokumen14 halamanTaxpayer Bill of Rights 2018Llerry Darlene Abaco RacuyaBelum ada peringkat

- BIR Ruling (DA-670-07) Lotto OutletDokumen3 halamanBIR Ruling (DA-670-07) Lotto OutletMonica Soriano100% (2)

- DOF Package 2 Top 10 Rationales As of Feb 28 2020Dokumen52 halamanDOF Package 2 Top 10 Rationales As of Feb 28 2020Monica SorianoBelum ada peringkat

- BIR Ruling (DA-357-03) Excess of SSS ReimbursementDokumen2 halamanBIR Ruling (DA-357-03) Excess of SSS ReimbursementMonica SorianoBelum ada peringkat

- Ethics Quamto PDFDokumen33 halamanEthics Quamto PDFGogo SorianoBelum ada peringkat

- Revenue Regulation....Dokumen28 halamanRevenue Regulation....Monica SorianoBelum ada peringkat

- Psic 1994Dokumen186 halamanPsic 1994jomardansBelum ada peringkat

- ATC HandbookDokumen15 halamanATC HandbookPrintet08Belum ada peringkat

- BIR Ruling No. 061-79 (EWT)Dokumen1 halamanBIR Ruling No. 061-79 (EWT)Monica SorianoBelum ada peringkat

- GMCAC - Follow-Up Clarification On Taxability of Purchase of GCs - 11.19.15Dokumen4 halamanGMCAC - Follow-Up Clarification On Taxability of Purchase of GCs - 11.19.15Monica SorianoBelum ada peringkat

- BIR Form 1921 - ATP - RMO 28 2002 PDFDokumen1 halamanBIR Form 1921 - ATP - RMO 28 2002 PDFMonica SorianoBelum ada peringkat

- Taxpayer Bill of Rights 2018Dokumen14 halamanTaxpayer Bill of Rights 2018Llerry Darlene Abaco RacuyaBelum ada peringkat

- Statutory Basis For The Imposition of FBT (RR 3-98)Dokumen5 halamanStatutory Basis For The Imposition of FBT (RR 3-98)Monica SorianoBelum ada peringkat

- CTA Case No. 8509Dokumen16 halamanCTA Case No. 8509Monica SorianoBelum ada peringkat

- Single Window - Annex - A1a3Dokumen4 halamanSingle Window - Annex - A1a3Monica SorianoBelum ada peringkat

- Philippine Health Insurance Corporation Re-imposes Interest on Late Premium PaymentsDokumen3 halamanPhilippine Health Insurance Corporation Re-imposes Interest on Late Premium PaymentsHomer Lopez PabloBelum ada peringkat

- Vendor Reporting Schedule for December 2018Dokumen26 halamanVendor Reporting Schedule for December 2018Monica SorianoBelum ada peringkat

- The Misunderstood Patriot: Pio ValenzuelaDokumen4 halamanThe Misunderstood Patriot: Pio ValenzuelamjBelum ada peringkat

- SSG Election Narrative ReportDokumen2 halamanSSG Election Narrative ReportTitzer Rey88% (84)

- USA vs. RANDALL KEITH BEANE, HEATHER ANN TUCCI-JARRAFDokumen92 halamanUSA vs. RANDALL KEITH BEANE, HEATHER ANN TUCCI-JARRAFArameus79Belum ada peringkat

- Oppose Donna Lee Elm Reappointment Federal DefenderDokumen196 halamanOppose Donna Lee Elm Reappointment Federal DefenderNeil GillespieBelum ada peringkat

- CTA erred in dismissing tax case due to non-payment of docket feesDokumen3 halamanCTA erred in dismissing tax case due to non-payment of docket feesJeffrey MagadaBelum ada peringkat

- Yeo v. Town of Lexington, 1st Cir. (1997)Dokumen134 halamanYeo v. Town of Lexington, 1st Cir. (1997)Scribd Government DocsBelum ada peringkat

- Khilafat Movement SlidesDokumen14 halamanKhilafat Movement SlidesSamantha JonesBelum ada peringkat

- CourtRuleFile - 3987DD3D CRPC Sec 125Dokumen9 halamanCourtRuleFile - 3987DD3D CRPC Sec 125surendra kumarBelum ada peringkat

- Arrest Jorge Mario Bergoglio PDFDokumen1 halamanArrest Jorge Mario Bergoglio PDFLucy Maysonet100% (2)

- Gec 1112 Prelim Exam Rizal and Contemporary 1Dokumen5 halamanGec 1112 Prelim Exam Rizal and Contemporary 1sarah miinggBelum ada peringkat

- Architectures of Globalization and Colonialism in ShanghaiDokumen38 halamanArchitectures of Globalization and Colonialism in ShanghaiUjjwal BhattacharyaBelum ada peringkat

- COA upholds disallowance of food basket allowance for BFAR employeesDokumen5 halamanCOA upholds disallowance of food basket allowance for BFAR employeesDaryl CruzBelum ada peringkat

- International Political Economy Exam PaperDokumen13 halamanInternational Political Economy Exam PaperNenad KrstevskiBelum ada peringkat

- National Intelligence Law of The People's Republic: Current Page Learn More - Text Only Version View SourceDokumen6 halamanNational Intelligence Law of The People's Republic: Current Page Learn More - Text Only Version View SourcenebaBelum ada peringkat

- Affidavit of Loss - GalangDokumen1 halamanAffidavit of Loss - GalangOrion RuayaBelum ada peringkat

- Civil Court and Code of Civil ProcedureDokumen17 halamanCivil Court and Code of Civil ProcedureShubhankar ThakurBelum ada peringkat

- RCC 1-40Dokumen2.572 halamanRCC 1-40neo paulBelum ada peringkat

- Arroyo vs. De Venecia Ruling on House Rules ViolationDokumen3 halamanArroyo vs. De Venecia Ruling on House Rules ViolationanalynBelum ada peringkat

- ICE UFT Election FlyerDokumen1 halamanICE UFT Election FlyerICEUFTBelum ada peringkat

- G.R. No. 169517 March 14, 2006 Tan and Pagayokan vs. BalajadiaDokumen7 halamanG.R. No. 169517 March 14, 2006 Tan and Pagayokan vs. BalajadiaShenilyn MendozaBelum ada peringkat

- Lukes 1977 Socialism and EqualityDokumen7 halamanLukes 1977 Socialism and EqualityDebora Tolentino GrossiBelum ada peringkat

- Whistle Blower PolicyDokumen5 halamanWhistle Blower PolicySumit TyagiBelum ada peringkat

- The Ec-Thailand Country Strategy PaperDokumen65 halamanThe Ec-Thailand Country Strategy PaperOon KooBelum ada peringkat

- Unions Make The MiddleclassDokumen44 halamanUnions Make The Middleclassscribd445566778899Belum ada peringkat

- Contract EssentialsDokumen3 halamanContract EssentialsNoemiAlodiaMoralesBelum ada peringkat

- Radhika Seth Election Notes Limitation Act SummaryDokumen117 halamanRadhika Seth Election Notes Limitation Act SummaryAvaniJainBelum ada peringkat

- Excellent Quality Apparel Vs Win Multiple Rich BuildersDokumen2 halamanExcellent Quality Apparel Vs Win Multiple Rich BuildersDarla GreyBelum ada peringkat

- Child Labour & TraffickingDokumen5 halamanChild Labour & TraffickingBaste BaluyotBelum ada peringkat

- DRL FY2020 The Global Equality Fund NOFODokumen23 halamanDRL FY2020 The Global Equality Fund NOFORuslan BrvBelum ada peringkat

- SC Judgement On Section 498A IPC Highlighting Misuse of Law Against Husbands 2018Dokumen35 halamanSC Judgement On Section 498A IPC Highlighting Misuse of Law Against Husbands 2018Latest Laws Team100% (1)