Anda mungkin juga menyukai

- The Toilet Paper Entrepreneur PDFDokumen198 halamanThe Toilet Paper Entrepreneur PDFMarco Gómez Caballero83% (6)

- Partnership Formation and OperationDokumen43 halamanPartnership Formation and OperationRay DonovanBelum ada peringkat

- Management Controll System BookDokumen192 halamanManagement Controll System Bookmathrix01Belum ada peringkat

- Presentation On Industrial Training ProjectDokumen38 halamanPresentation On Industrial Training ProjectBHAWANACHAWLA100% (1)

- Price Adjustment in Construction ContractDokumen7 halamanPrice Adjustment in Construction ContractRam Prasad Awasthi100% (1)

- A R RoqueDokumen73 halamanA R RoqueTwish BarriosBelum ada peringkat

- Project Timeline de Pus Planned Jos: Q1 January FebruaryDokumen20 halamanProject Timeline de Pus Planned Jos: Q1 January FebruaryAlexandruDanielBelum ada peringkat

- Aris A. Syntetos, Service Parts Management - Demand Forecasting and Inventory Control-Springer-Verlag London (2011)Dokumen327 halamanAris A. Syntetos, Service Parts Management - Demand Forecasting and Inventory Control-Springer-Verlag London (2011)Agung SudrajatBelum ada peringkat

- Management Control Systems and Strategy A Critical ReviewDokumen26 halamanManagement Control Systems and Strategy A Critical ReviewDimas Jatu WidiatmajaBelum ada peringkat

- A Review On The Growing Importance of Location IntelligenceDokumen2 halamanA Review On The Growing Importance of Location IntelligenceAirSage Inc.Belum ada peringkat

- Management - ControlDokumen20 halamanManagement - Controlrsikira7905Belum ada peringkat

- R3 SimonsDokumen17 halamanR3 SimonsFathur RojiBelum ada peringkat

- Mastering Opportunities and Risks in IT Projects: Identifying, anticipating and controlling opportunities and risks: A model for effective management in IT development and operationDari EverandMastering Opportunities and Risks in IT Projects: Identifying, anticipating and controlling opportunities and risks: A model for effective management in IT development and operationBelum ada peringkat

- BSBMKG 501 Identify and Evaluate Marketing OpportunitiesDokumen17 halamanBSBMKG 501 Identify and Evaluate Marketing Opportunitiesbabluanand100% (1)

- CHPTR 1Dokumen3 halamanCHPTR 1tghongeBelum ada peringkat

- Management Control SystemDokumen2 halamanManagement Control SystemManisha GuptaBelum ada peringkat

- Robert NDokumen2 halamanRobert NentelkiBelum ada peringkat

- Marketing 08.completed - WordDokumen21 halamanMarketing 08.completed - WordboutelaylaaBelum ada peringkat

- Management Control SystemsDokumen9 halamanManagement Control SystemsKetan BhandariBelum ada peringkat

- Chhillar - Management Control Systems and Corporate Governance A Theoretical Review PDFDokumen26 halamanChhillar - Management Control Systems and Corporate Governance A Theoretical Review PDFOsfred Umbu Djadji100% (1)

- Summary of Journal Management Control SystemDokumen3 halamanSummary of Journal Management Control SystemYara Abu JaberBelum ada peringkat

- Article1379425775 NamaziDokumen10 halamanArticle1379425775 NamazivisdaishamnatserBelum ada peringkat

- Management ControlDokumen16 halamanManagement ControlsrikantBelum ada peringkat

- 3 Management Control System Changes, Influencing Internal Factors, Firm Performance, and The Conceptual Framework of The StudyDokumen28 halaman3 Management Control System Changes, Influencing Internal Factors, Firm Performance, and The Conceptual Framework of The StudyAmar MaharanaBelum ada peringkat

- Chhillar - Management Control Systems and Corporate Governance A Theoretical ReviewDokumen26 halamanChhillar - Management Control Systems and Corporate Governance A Theoretical Reviewdinda adventiawatiBelum ada peringkat

- Management Control SystemDokumen18 halamanManagement Control SystemCamilaBelum ada peringkat

- Mid Exam Management Control SystemDokumen6 halamanMid Exam Management Control SystemKristina KittyBelum ada peringkat

- MCS - Unit IDokumen145 halamanMCS - Unit ISubin RajBelum ada peringkat

- Effectiveness of Management Control Systems As Levers of Strategic Renewal: An Exploratory StudyDokumen16 halamanEffectiveness of Management Control Systems As Levers of Strategic Renewal: An Exploratory Studydr_tripathineeraj100% (1)

- Analyze The Factors That Have An Influence On The Management Control SystemDokumen8 halamanAnalyze The Factors That Have An Influence On The Management Control SystemiisteBelum ada peringkat

- Management and Public Administration - EditedDokumen2 halamanManagement and Public Administration - EditedIwuagwu JosephBelum ada peringkat

- Langfield 1997Dokumen26 halamanLangfield 1997Yan SugondoBelum ada peringkat

- Management Control SystemsDokumen14 halamanManagement Control SystemsTejashree SavantBelum ada peringkat

- Behavioral FactorsDokumen10 halamanBehavioral FactorsDennis ChenBelum ada peringkat

- 2 - British Journal of Management - Management Control - An Overview of Its DevelopmentDokumen14 halaman2 - British Journal of Management - Management Control - An Overview of Its DevelopmentTAMBA CEDRICBelum ada peringkat

- SM5b-The Evolution of The Concept of Management Control Towards A Definition of Performance Management SystemDokumen47 halamanSM5b-The Evolution of The Concept of Management Control Towards A Definition of Performance Management SystemArief MunandarBelum ada peringkat

- Mcs 1Dokumen7 halamanMcs 1shru14Belum ada peringkat

- 452 MCSDokumen208 halaman452 MCSDigvijay DiggiBelum ada peringkat

- Managerial Style ArticleDokumen7 halamanManagerial Style ArticleAna-MariaBelum ada peringkat

- Management Control System, A Historical PerspectiveDokumen19 halamanManagement Control System, A Historical PerspectiveAlessandro LangellaBelum ada peringkat

- Managment Practices Chapter TwoDokumen16 halamanManagment Practices Chapter TwoTolu OlusakinBelum ada peringkat

- Management Is The Process of Reaching Organizational Goals by Working With and Through People and Other Organizational ResourcesDokumen6 halamanManagement Is The Process of Reaching Organizational Goals by Working With and Through People and Other Organizational ResourcesMicah Acudo Tampos100% (1)

- INTRODUCTION To Management AccountingDokumen4 halamanINTRODUCTION To Management AccountingOkechukwu LovedayBelum ada peringkat

- Management Theory and Practice Paper PresentationDokumen8 halamanManagement Theory and Practice Paper PresentationsavedroseBelum ada peringkat

- MCS1st SessionDokumen29 halamanMCS1st SessionLea WigiartiBelum ada peringkat

- Otley1999 PDFDokumen20 halamanOtley1999 PDFrezasattariBelum ada peringkat

- Accounting, Budgeting, and Control Systems in Their Organizational Context: Theoretical and Empirical Prespectives By: Eric G. FlamholtzDokumen1 halamanAccounting, Budgeting, and Control Systems in Their Organizational Context: Theoretical and Empirical Prespectives By: Eric G. FlamholtzKadekBelum ada peringkat

- Meta Analysis of Management Control System StrategDokumen9 halamanMeta Analysis of Management Control System Strategandini243Belum ada peringkat

- Introduction: Meaning Nature and Basic Concepts: ObjectivesDokumen16 halamanIntroduction: Meaning Nature and Basic Concepts: ObjectivesKetema AsfawBelum ada peringkat

- 1992 AmjDokumen37 halaman1992 AmjMiguel Sánchez RivasBelum ada peringkat

- Control, Organisation and AccountingDokumen14 halamanControl, Organisation and AccountingDaegal LeungBelum ada peringkat

- Management Control Systems 3Dokumen6 halamanManagement Control Systems 3Manjunath HSBelum ada peringkat

- Abstract:: How Can Management Control System Fairness Reduce Managers' Unethical Behaviours?Dokumen37 halamanAbstract:: How Can Management Control System Fairness Reduce Managers' Unethical Behaviours?Oom DzakyBelum ada peringkat

- 5.0 Business EnvironmentDokumen78 halaman5.0 Business EnvironmentReizel Jane PascuaBelum ada peringkat

- Management Accounting EssayDokumen5 halamanManagement Accounting EssayvardaBelum ada peringkat

- Presented by Pramod Tiwari Roll No - 40Dokumen16 halamanPresented by Pramod Tiwari Roll No - 40Govind VijayvargiyaBelum ada peringkat

- Running Head: CONTROL 1Dokumen8 halamanRunning Head: CONTROL 1Audrey Martin DodsonBelum ada peringkat

- Managementcontrol 150506055614 Conversion Gate02Dokumen14 halamanManagementcontrol 150506055614 Conversion Gate02Waqas IqbalBelum ada peringkat

- Behavior in The Context of Management AccountingDokumen14 halamanBehavior in The Context of Management AccountingAzlan PspBelum ada peringkat

- Performance Management A Framework For MDokumen20 halamanPerformance Management A Framework For MNurussyifa SafiraBelum ada peringkat

- Effectiveness of Management Control System in Organisation..Dokumen4 halamanEffectiveness of Management Control System in Organisation..Arjun SukumaranBelum ada peringkat

- Jessica MbuliDokumen11 halamanJessica MbuliHilda MbuliBelum ada peringkat

- 1 5150099021255147675Dokumen5 halaman1 5150099021255147675Ketema AsfawBelum ada peringkat

- Give An Overview On Management Control System and Its Importance in Different Organizations With Examples?Dokumen4 halamanGive An Overview On Management Control System and Its Importance in Different Organizations With Examples?Hanisha RaviBelum ada peringkat

- MGT Control 3Dokumen18 halamanMGT Control 3Lawal Idris AdesholaBelum ada peringkat

- Henri, Jean-Francois (2006) Organizational Culture and Performance Management SystemDokumen3 halamanHenri, Jean-Francois (2006) Organizational Culture and Performance Management SystemFiqih Daffa100% (1)

- Parte 1 Andy en-GBDokumen19 halamanParte 1 Andy en-GBAlicia CavadaBelum ada peringkat

- 08 - The - Presentation Layer - ENGLISH (2nd Edt V0.2)Dokumen52 halaman08 - The - Presentation Layer - ENGLISH (2nd Edt V0.2)Ankur GuptaBelum ada peringkat

- ACCT 423 Cheat Sheet 1.0Dokumen2 halamanACCT 423 Cheat Sheet 1.0HelloWorldNowBelum ada peringkat

- Disruptive TechnologyDokumen3 halamanDisruptive TechnologyNeetu GoyalBelum ada peringkat

- Intan Larasati 2A English For Syariah Banking Islamic Banking and Finance ContextDokumen7 halamanIntan Larasati 2A English For Syariah Banking Islamic Banking and Finance ContextMauLana IqbalBelum ada peringkat

- Chapter SummaryDokumen11 halamanChapter SummaryJenjen AnieteBelum ada peringkat

- Service Plan For 2GO TravelDokumen33 halamanService Plan For 2GO TravelPaulino OccupadoBelum ada peringkat

- Marketing MixDokumen14 halamanMarketing MixNhư QuỳnhBelum ada peringkat

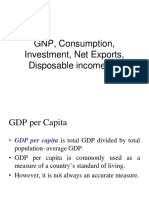

- GNP, Consumption, Investment, Net Exports, Disposable Income EtcDokumen18 halamanGNP, Consumption, Investment, Net Exports, Disposable Income EtcAurongo NasirBelum ada peringkat

- Case Questions Excel SheetDokumen8 halamanCase Questions Excel SheetMustafa MahmoodBelum ada peringkat

- Bed2110 2124 Mathematics For Economist I Reg SuppDokumen4 halamanBed2110 2124 Mathematics For Economist I Reg SuppQelvoh JoxBelum ada peringkat

- Notice Inviting Tender (NIT) For Empanelment of Survey Agencies For Conducting Surveys On Households and EnterprisesDokumen56 halamanNotice Inviting Tender (NIT) For Empanelment of Survey Agencies For Conducting Surveys On Households and Enterprisesssat111Belum ada peringkat

- Finance Lecturers by Course and Size UNSWDokumen2 halamanFinance Lecturers by Course and Size UNSWhello248Belum ada peringkat

- Starbucks Confirms Rapid Growth StrategyDokumen2 halamanStarbucks Confirms Rapid Growth StrategyAlexandros PetronikolosBelum ada peringkat

- 01JUNIDokumen1 halaman01JUNISteven Kuang01Belum ada peringkat

- Annual Report 2020 Full Version PDF 1Dokumen161 halamanAnnual Report 2020 Full Version PDF 1pukis pukisBelum ada peringkat

- Annual Report 2011Dokumen41 halamanAnnual Report 2011Moinul HasanBelum ada peringkat

- SAP-APO - Create Field Material ViewDokumen8 halamanSAP-APO - Create Field Material ViewPArk100Belum ada peringkat

- Sale 238 26-06-2023Dokumen2 halamanSale 238 26-06-2023Creeper TechnologiesBelum ada peringkat

- Lesson 2.2 Compound InterestDokumen30 halamanLesson 2.2 Compound InterestShyla Patrice DantesBelum ada peringkat

- 1 - Finance Short NotesDokumen12 halaman1 - Finance Short NotesSudhanshu PatelBelum ada peringkat

- DSD Fee Study 12.04.202Dokumen27 halamanDSD Fee Study 12.04.202April ToweryBelum ada peringkat