Anda mungkin juga menyukai

- Energy Prices: Ameron HanoveDokumen3 halamanEnergy Prices: Ameron HanoveDvNetBelum ada peringkat

- Energy Prices: Ameron HanoveDokumen3 halamanEnergy Prices: Ameron HanoveDvNetBelum ada peringkat

- Energy Prices: Ameron HanoveDokumen3 halamanEnergy Prices: Ameron HanoveDvNetBelum ada peringkat

- 0119PMDokumen3 halaman0119PMadmin3341Belum ada peringkat

- Energy Prices: Ameron HanoveDokumen3 halamanEnergy Prices: Ameron HanoveDvNetBelum ada peringkat

- Energy Prices: Ameron HanoveDokumen3 halamanEnergy Prices: Ameron HanoveDvNetBelum ada peringkat

- 0809PMDokumen2 halaman0809PMZerohedgeBelum ada peringkat

- 0802PMDokumen2 halaman0802PMZerohedgeBelum ada peringkat

- 0812PMDokumen2 halaman0812PMZerohedgeBelum ada peringkat

- 0816PMDokumen2 halaman0816PMZerohedgeBelum ada peringkat

- Economic Survey of India 2022 - 2023 - TableDokumen145 halamanEconomic Survey of India 2022 - 2023 - Tablemerawi6699Belum ada peringkat

- Ameron Hanove: Aily Nergy EdgerDokumen12 halamanAmeron Hanove: Aily Nergy Edgeradmin3341Belum ada peringkat

- Summary of Daily Minimum Wage Rates Per Wage Order, by Region Non-Agriculture (1989 - 2014)Dokumen11 halamanSummary of Daily Minimum Wage Rates Per Wage Order, by Region Non-Agriculture (1989 - 2014)Arnold ApduaBelum ada peringkat

- Quiz 1 - 20220916 - Crude Oil Vs Natural Gas - SLNDokumen13 halamanQuiz 1 - 20220916 - Crude Oil Vs Natural Gas - SLNĐỗ Huy HoàngBelum ada peringkat

- Workbook Contents: Henry Hub Natural Gas Spot Price (Dollars Per Million Btu)Dokumen8 halamanWorkbook Contents: Henry Hub Natural Gas Spot Price (Dollars Per Million Btu)Alexander SeminarioBelum ada peringkat

- Premi Driver & Operator April 2022-AeroDokumen41 halamanPremi Driver & Operator April 2022-AeroMey Frenty TariganBelum ada peringkat

- Tipo de Cambio: Fuente: Banco Central de ChileDokumen22 halamanTipo de Cambio: Fuente: Banco Central de ChileBenjamin EspañaBelum ada peringkat

- Black 7e Excel DatabaseDokumen45 halamanBlack 7e Excel DatabaseSaumil PatelBelum ada peringkat

- Igp-Di: Mês Índice Variação (%) No Mês No Ano 12 MesesDokumen7 halamanIgp-Di: Mês Índice Variação (%) No Mês No Ano 12 MesesRenato VasconcellosBelum ada peringkat

- Summary of Nca MinistriesDokumen205 halamanSummary of Nca MinistriesHazel Ommayah Tomawis-MangansakanBelum ada peringkat

- Data Set 6 - ProcessedDokumen34 halamanData Set 6 - ProcessedNguyễn Thị Ánh NgọcBelum ada peringkat

- PswrgvwallDokumen2.058 halamanPswrgvwallShrekBelum ada peringkat

- Tabel 1.1 Data Curah Hujan Harian MaksimumDokumen10 halamanTabel 1.1 Data Curah Hujan Harian MaksimumIrfan LuckerBelum ada peringkat

- Vengkar AssignmentDokumen10 halamanVengkar AssignmentVengkar SoibamBelum ada peringkat

- Monthly Averages of Air Temperatures (In Celsius) and Amount of Rainfall in Lake Taal From 2000 - 2011Dokumen33 halamanMonthly Averages of Air Temperatures (In Celsius) and Amount of Rainfall in Lake Taal From 2000 - 2011Brian PaguiaBelum ada peringkat

- Hidro Rian (1) - 101748Dokumen31 halamanHidro Rian (1) - 101748Muhammad Farid RaisBelum ada peringkat

- 02ab Serie Historica Inpc IbgeDokumen7 halaman02ab Serie Historica Inpc IbgeAlberto AndradeBelum ada peringkat

- 591b Serie Historica Incc Di FGVDokumen12 halaman591b Serie Historica Incc Di FGVGuilherme GomezBelum ada peringkat

- Incc-Di: Mês Índice Variação (%) No Mês No Ano 12 MesesDokumen10 halamanIncc-Di: Mês Índice Variação (%) No Mês No Ano 12 MesesRenato VasconcellosBelum ada peringkat

- Incc-Di: Mês Índice Variação (%) No Mês No Ano 12 MesesDokumen7 halamanIncc-Di: Mês Índice Variação (%) No Mês No Ano 12 MesesEdson PontesBelum ada peringkat

- Blackrock Global Funds - Global Opportunities Fund - $A2 (Mi9X) Mi9X:Gr Germany Open-End FundDokumen12 halamanBlackrock Global Funds - Global Opportunities Fund - $A2 (Mi9X) Mi9X:Gr Germany Open-End FundAndreea GorunBelum ada peringkat

- Global Opportunities Fund Price HistoryDokumen12 halamanGlobal Opportunities Fund Price HistoryAndreea GorunBelum ada peringkat

- G13 - MGM GrandDokumen4.953 halamanG13 - MGM GrandShaina DewanBelum ada peringkat

- Table of monetary update factors for contribution salariesDokumen4 halamanTable of monetary update factors for contribution salariesMárcia MendesBelum ada peringkat

- Nikkei 225 stock chart from 1984 to 2002Dokumen72 halamanNikkei 225 stock chart from 1984 to 2002Gallo SolarisBelum ada peringkat

- Tabela de Atualização Monetária Dos Salários-De - Contribuição para Apuração Do Salário-De-Benefício (Art.33, Decreto N 3.048/99)Dokumen4 halamanTabela de Atualização Monetária Dos Salários-De - Contribuição para Apuração Do Salário-De-Benefício (Art.33, Decreto N 3.048/99)Márcia MendesBelum ada peringkat

- Industry Type Food & AlliedDokumen140 halamanIndustry Type Food & AlliedShaikh Saifullah KhalidBelum ada peringkat

- ChocolateDokumen3 halamanChocolateCristinaBelum ada peringkat

- Cat Turnover 050224Dokumen4 halamanCat Turnover 050224anilkhubchandani9744Belum ada peringkat

- Feb 2020Dokumen4 halamanFeb 2020Sardar Aqeel BashirBelum ada peringkat

- Incc-M: Mês Índice Variação (%) No Mês No Ano 12 MesesDokumen8 halamanIncc-M: Mês Índice Variação (%) No Mês No Ano 12 MesesRenato VasconcellosBelum ada peringkat

- Incc-M: Mês Índice Variação (%) No Mês No Ano 12 MesesDokumen9 halamanIncc-M: Mês Índice Variação (%) No Mês No Ano 12 MesesRenato VasconcellosBelum ada peringkat

- Case: 3-5-1 Case: 3-5-2Dokumen48 halamanCase: 3-5-1 Case: 3-5-2Firas BarrajBelum ada peringkat

- Around 3% LOSSES Removal From Monthly UnitsDokumen6 halamanAround 3% LOSSES Removal From Monthly UnitsBhargav KumarBelum ada peringkat

- 4008-Serie-Historica-Igp-M-Fgv - JANEIRO-2021Dokumen8 halaman4008-Serie-Historica-Igp-M-Fgv - JANEIRO-2021Renato VasconcellosBelum ada peringkat

- Blotong 2023Dokumen5 halamanBlotong 2023Helmi KurniaBelum ada peringkat

- 7a6d Syrie Histyrica Incc Di FGVDokumen10 halaman7a6d Syrie Histyrica Incc Di FGVcaionvrroBelum ada peringkat

- Incc-Di: Mês Índice Variação (%) No Mês No Ano 12 MesesDokumen10 halamanIncc-Di: Mês Índice Variação (%) No Mês No Ano 12 MesescaionvrroBelum ada peringkat

- STT STT Bid BVH CTD CTG DPM Eib FPT Gas GMD HDB HPG MBB MSNMWGNVL PNJ ReeDokumen23 halamanSTT STT Bid BVH CTD CTG DPM Eib FPT Gas GMD HDB HPG MBB MSNMWGNVL PNJ ReeTuan NguyenBelum ada peringkat

- Gold plows to record high after Powell's remarks, (AKD Commodities vantage, Apr 04 2024)Dokumen5 halamanGold plows to record high after Powell's remarks, (AKD Commodities vantage, Apr 04 2024)Awais KhalidBelum ada peringkat

- Cost of Caital - Gabriel IndiaDokumen26 halamanCost of Caital - Gabriel IndiasarangdharBelum ada peringkat

- Managerial Economics Midterm Exam AnalysisDokumen8 halamanManagerial Economics Midterm Exam AnalysisAilene QuintoBelum ada peringkat

- T Year Month Demand MA (4) CMA (4) S, I S: Regression StatisticsDokumen8 halamanT Year Month Demand MA (4) CMA (4) S, I S: Regression StatisticsAilene QuintoBelum ada peringkat

- Student Datafile (Lab1)Dokumen61 halamanStudent Datafile (Lab1)bishoy sefinBelum ada peringkat

- Student Datafile EnviroDokumen61 halamanStudent Datafile Envirobishoy sefinBelum ada peringkat

- Student Datafile (Lab1)Dokumen61 halamanStudent Datafile (Lab1)bishoy sefinBelum ada peringkat

- Managerial Economics Midterm Exam AnalysisDokumen8 halamanManagerial Economics Midterm Exam AnalysisAilene QuintoBelum ada peringkat

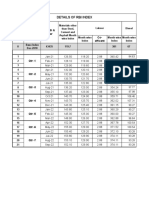

- Details of Rbi IndexDokumen1 halamanDetails of Rbi IndexBhadresh KumbhaniBelum ada peringkat

- Salary contribution monetary update factors 1994-2007Dokumen3 halamanSalary contribution monetary update factors 1994-2007Márcia MendesBelum ada peringkat

- Donald Trump National Security LetterDokumen8 halamanDonald Trump National Security LetterGerman Lopez33% (3)

- ECB Financial Stability Review - May 2015Dokumen12 halamanECB Financial Stability Review - May 2015DvNetBelum ada peringkat

- ANTIBIOTIC RESISTANCE THREATS in The United States, 2013Dokumen114 halamanANTIBIOTIC RESISTANCE THREATS in The United States, 2013Virabase100% (2)

- Government Development Bank For Puerto Rico Provides Update On Fiscal and Economic Development ProgressDokumen2 halamanGovernment Development Bank For Puerto Rico Provides Update On Fiscal and Economic Development ProgressDvNetBelum ada peringkat

- Central Bank Incentive Program Questions & Answers January 2014Dokumen4 halamanCentral Bank Incentive Program Questions & Answers January 2014DvNetBelum ada peringkat

- The Commonwealth of Puerto Rico Update On Fiscal and Economic Progress FY 2014 Q1 Investor Webcast - October 15, 2013Dokumen73 halamanThe Commonwealth of Puerto Rico Update On Fiscal and Economic Progress FY 2014 Q1 Investor Webcast - October 15, 2013DvNetBelum ada peringkat

- Central Bank Incentive Program - CME GroupDokumen3 halamanCentral Bank Incentive Program - CME GroupIBIS_NewsBelum ada peringkat

- Valuations Suggest Extremely Overvalued MarketDokumen9 halamanValuations Suggest Extremely Overvalued Marketstreettalk700Belum ada peringkat

- Russian Sanctions 9/12/2014Dokumen13 halamanRussian Sanctions 9/12/2014DvNetBelum ada peringkat

- Reserve Bank of Indias January 28, 2014 Policy StatementDokumen2 halamanReserve Bank of Indias January 28, 2014 Policy StatementDvNetBelum ada peringkat

- Jack Lew Debt Ceiling Letter To CongressDokumen2 halamanJack Lew Debt Ceiling Letter To CongressBrett LoGiuratoBelum ada peringkat

- Notorious Summer of 2008 by St. Louis Fed President James Bullard NWArkansas - 11/21/2013Dokumen36 halamanNotorious Summer of 2008 by St. Louis Fed President James Bullard NWArkansas - 11/21/2013DvNetBelum ada peringkat

- Commonwealth ReportDokumen151 halamanCommonwealth ReportDvNetBelum ada peringkat

- Office of The SecretaryDokumen2 halamanOffice of The SecretaryDvNetBelum ada peringkat

- 2013 08 07 Snap June2013Dokumen4 halaman2013 08 07 Snap June2013DvNetBelum ada peringkat

- 2013 08 07 Snap June2013Dokumen4 halaman2013 08 07 Snap June2013DvNetBelum ada peringkat

- Debt Limit Letter To CongressDokumen2 halamanDebt Limit Letter To CongressBrett LoGiuratoBelum ada peringkat

- Commonwealth ReportDokumen151 halamanCommonwealth ReportDvNetBelum ada peringkat

- Koo PaperDokumen32 halamanKoo PaperDvNetBelum ada peringkat

- Overview of New York City's Fiscal Crisis (1995)Dokumen10 halamanOverview of New York City's Fiscal Crisis (1995)DvNetBelum ada peringkat

- 2-Year FY 2010 Student Default Rates by StateDokumen2 halaman2-Year FY 2010 Student Default Rates by StateDvNetBelum ada peringkat

- Richard Koo - The Future of Central Banking and Closing Remarks - INET Hong KongDokumen6 halamanRichard Koo - The Future of Central Banking and Closing Remarks - INET Hong KongDvNetBelum ada peringkat

- Barclays LIBOR/Interest Rate Derivatives Trading FraudDokumen45 halamanBarclays LIBOR/Interest Rate Derivatives Trading FraudDvNet100% (1)

- 2012 Global Box Office ResultsDokumen1 halaman2012 Global Box Office ResultsDvNetBelum ada peringkat

- 2-Year FY 2010 Student Default Rates by StateDokumen2 halaman2-Year FY 2010 Student Default Rates by StateDvNetBelum ada peringkat

- Jon Corzine MemoDokumen5 halamanJon Corzine MemoDvNetBelum ada peringkat

- Perspectives On The Current Stance of Monetary Policy - James BullardDokumen41 halamanPerspectives On The Current Stance of Monetary Policy - James BullardDvNetBelum ada peringkat

- Financial Services Authority: Final NoticeDokumen44 halamanFinancial Services Authority: Final Noticeannawitkowski88Belum ada peringkat

- News 2012-6-26 PendencyPlanApprovedDokumen3 halamanNews 2012-6-26 PendencyPlanApprovedDvNetBelum ada peringkat

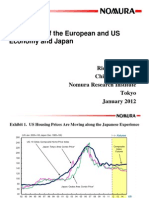

- Richard Koo Foreign Press Slides (January 2012)Dokumen35 halamanRichard Koo Foreign Press Slides (January 2012)DvNetBelum ada peringkat

- What Is The Breakeven Point (BEP) ?Dokumen3 halamanWhat Is The Breakeven Point (BEP) ?Niño Rey LopezBelum ada peringkat

- Chapter 5 Chapter 5: Risk and ReturnDokumen20 halamanChapter 5 Chapter 5: Risk and ReturnAhmad Ridhuwan AbdullahBelum ada peringkat

- Supply and Demand PDF FreeDokumen206 halamanSupply and Demand PDF Freejeerus Intis100% (1)

- Framework Agreements PDFDokumen11 halamanFramework Agreements PDFSaji VarkeyBelum ada peringkat

- Monmouth CaseDokumen6 halamanMonmouth CaseMohammed Akhtab Ul HudaBelum ada peringkat

- Mankiw SolutionDokumen259 halamanMankiw SolutionKathleen RosemalaBelum ada peringkat

- Australian Exporter Currency Exchange Loss CalculationDokumen9 halamanAustralian Exporter Currency Exchange Loss CalculationleieparanoicoBelum ada peringkat

- Understanding Taxation and its ImportanceDokumen2 halamanUnderstanding Taxation and its ImportanceHannah Alvarado BandolaBelum ada peringkat

- MBA5312 Chapter 3 Quiz PDFDokumen2 halamanMBA5312 Chapter 3 Quiz PDFKunal GuptaBelum ada peringkat

- The Use of Quill Patent and Steel Pens by The Boe During The Nineteenth CenturyDokumen5 halamanThe Use of Quill Patent and Steel Pens by The Boe During The Nineteenth CenturySpencerian ScriptBelum ada peringkat

- Problems SAPMDokumen4 halamanProblems SAPMSneha Swamy100% (1)

- Speaking Question Templates for Choice, Reporter, and Teacher RolesDokumen6 halamanSpeaking Question Templates for Choice, Reporter, and Teacher Rolesseb_streitenberger100% (9)

- Government Intervention Activity AnalysisDokumen1 halamanGovernment Intervention Activity AnalysisMartha AntonBelum ada peringkat

- M&M Pizza CaseDokumen8 halamanM&M Pizza Caseaotorres99Belum ada peringkat

- List of Senior Citizen Discounts and VAT ExemptionsDokumen8 halamanList of Senior Citizen Discounts and VAT ExemptionsJoline UrbinaBelum ada peringkat

- The Market For "Lemons": Quality Uncertainty and The Market MechanismDokumen17 halamanThe Market For "Lemons": Quality Uncertainty and The Market MechanismRizki Andre PrayudaBelum ada peringkat

- 2023 Tef - Undp Rwanda Tef Business Pitch Questions DocumentDokumen2 halaman2023 Tef - Undp Rwanda Tef Business Pitch Questions DocumentVUGA UKIREBelum ada peringkat

- Index: Foreign Exchange MarketDokumen62 halamanIndex: Foreign Exchange MarketSamBelum ada peringkat

- Group 8, F-403Dokumen22 halamanGroup 8, F-403Shaikh Saifullah KhalidBelum ada peringkat

- Challenges of International BusinessDokumen4 halamanChallenges of International BusinessRikesh SapkotaBelum ada peringkat

- Competition in The Long-RunDokumen28 halamanCompetition in The Long-RunRudjun TapalBelum ada peringkat

- Chapter 2 Fair Value Measurement IFRS 13Dokumen21 halamanChapter 2 Fair Value Measurement IFRS 13johnegnBelum ada peringkat

- Bloomberg Technical Analysis HandbookDokumen35 halamanBloomberg Technical Analysis HandbookDiegoGarciaBermudezBelum ada peringkat

- 2019-06-29 IFR Asia - UnknownDokumen50 halaman2019-06-29 IFR Asia - UnknownqbichBelum ada peringkat

- Macroeconomics Measuring GDPDokumen6 halamanMacroeconomics Measuring GDPJoeBelum ada peringkat

- Chapter 2-GST Part B - Value of SupplyDokumen7 halamanChapter 2-GST Part B - Value of SupplyPooja D AcharyaBelum ada peringkat

- FMCC212 CHAPTER 23 TO CHAPTER 32 PPE-IDENTIFIABLE INTANGIBLE ASSETSDokumen18 halamanFMCC212 CHAPTER 23 TO CHAPTER 32 PPE-IDENTIFIABLE INTANGIBLE ASSETSErica Estelle May MagrareBelum ada peringkat

- CBSE Revised Syllabus & Sample Papers for Economics XII Exam 2021Dokumen50 halamanCBSE Revised Syllabus & Sample Papers for Economics XII Exam 2021The Unknown vlogger100% (1)

- Costco Marketing Strategy Term PaperDokumen7 halamanCostco Marketing Strategy Term Paperc5ha8c7g100% (1)

- Rise Food Mall Price List-1 March 2024 RetailDokumen1 halamanRise Food Mall Price List-1 March 2024 RetailNavjot Singh NarangBelum ada peringkat