Anda mungkin juga menyukai

- Investment Perspectives: What Are The Infl Ation Beating Asset Classes?Dokumen32 halamanInvestment Perspectives: What Are The Infl Ation Beating Asset Classes?Len RittbergBelum ada peringkat

- When Stock-Bond Diversification FailsDokumen17 halamanWhen Stock-Bond Diversification FailsRickardBelum ada peringkat

- A Technical Paper On "Inflation Indexed Bonds (Iibs) " : I. RationaleDokumen11 halamanA Technical Paper On "Inflation Indexed Bonds (Iibs) " : I. Rationaletarunmehta24Belum ada peringkat

- Inflation and Real Estate InvestmentDokumen22 halamanInflation and Real Estate InvestmentShamsheer Ali TurkBelum ada peringkat

- Blackrock Special Report - Inflation-Linked Bonds PrimerDokumen8 halamanBlackrock Special Report - Inflation-Linked Bonds PrimerGreg JachnoBelum ada peringkat

- How Important Is The Stock Market Effect On Consumption?: Sydney Ludvigson and Charles SteindelDokumen23 halamanHow Important Is The Stock Market Effect On Consumption?: Sydney Ludvigson and Charles SteindelpinakindpatelBelum ada peringkat

- Part2-EquityInvestmentsAsAHedgeAgainst LazardResearchDokumen7 halamanPart2-EquityInvestmentsAsAHedgeAgainst LazardResearchLen RittbergBelum ada peringkat

- Uncertainty and Style Dynamics: Portfolios Under ConstructionDokumen27 halamanUncertainty and Style Dynamics: Portfolios Under ConstructionRaphael100% (1)

- This Content Downloaded From 152.118.24.31 On Fri, 07 May 2021 01:48:47 UTCDokumen6 halamanThis Content Downloaded From 152.118.24.31 On Fri, 07 May 2021 01:48:47 UTCclinton junkBelum ada peringkat

- S Z C I S ..................................................................................................................... 12Dokumen15 halamanS Z C I S ..................................................................................................................... 12darkheart_29Belum ada peringkat

- Benefits and Risks of Alternative Investment Strategies : October 10 2002Dokumen22 halamanBenefits and Risks of Alternative Investment Strategies : October 10 2002sherlock92Belum ada peringkat

- Hedging Inflation Risk A Practical GuideDokumen7 halamanHedging Inflation Risk A Practical GuidemainooBelum ada peringkat

- Insight Education On ILBDokumen6 halamanInsight Education On ILBSean ChuaBelum ada peringkat

- Barcap Global Inflation Linked Products 2010Dokumen312 halamanBarcap Global Inflation Linked Products 2010linxu124Belum ada peringkat

- Inflation: MacroeconomicsDokumen15 halamanInflation: MacroeconomicsNathaniel Remendado100% (1)

- Lesson 5 - Economy - Inflation Lyst8717Dokumen20 halamanLesson 5 - Economy - Inflation Lyst8717Deepak ShahBelum ada peringkat

- TEST-8: Lesson 5 InflationDokumen20 halamanTEST-8: Lesson 5 InflationDeepak ShahBelum ada peringkat

- Business Journal 200206 DDokumen15 halamanBusiness Journal 200206 DTroy SmithBelum ada peringkat

- Towers Watson Treasury Inflation Protected Securities TIPs White PaperDokumen6 halamanTowers Watson Treasury Inflation Protected Securities TIPs White Paperkamath.abhi3173Belum ada peringkat

- Investment Outlook: Great Expectations: InflationDokumen16 halamanInvestment Outlook: Great Expectations: InflationjregusBelum ada peringkat

- Inside The Vault - Spring 2011Dokumen8 halamanInside The Vault - Spring 2011Federal Reserve Bank of St. LouisBelum ada peringkat

- Yield Curve Control 1942-51 RoseDokumen16 halamanYield Curve Control 1942-51 RosesuksesBelum ada peringkat

- 2nd Exam FinmanDokumen17 halaman2nd Exam FinmanKate AngBelum ada peringkat

- En Measuring Liquidity Risk A Cross Asset Perspective July 2015Dokumen8 halamanEn Measuring Liquidity Risk A Cross Asset Perspective July 2015MinhChauTranBelum ada peringkat

- Common Stocks As A Hedge Against InflationDokumen13 halamanCommon Stocks As A Hedge Against InflationManias Panics CrashesBelum ada peringkat

- The Global Financial Environment: Major Advanced EconomiesDokumen12 halamanThe Global Financial Environment: Major Advanced EconomiesKashvi KatewaBelum ada peringkat

- S B M - A I: Tudy of Various Factors Affecting Return in OND Arket Case of NdiaDokumen13 halamanS B M - A I: Tudy of Various Factors Affecting Return in OND Arket Case of Ndialekha1997Belum ada peringkat

- How Do Regular Treasury Bonds WorkDokumen3 halamanHow Do Regular Treasury Bonds WorkiluvparixitBelum ada peringkat

- Sy CH - 5Dokumen8 halamanSy CH - 5Rafayeat Hasan MehediBelum ada peringkat

- An Investor's Guide To Inflation-Linked BondsDokumen16 halamanAn Investor's Guide To Inflation-Linked BondscoolaclBelum ada peringkat

- Portfolio Rotation StrategyDokumen8 halamanPortfolio Rotation StrategyONKAR BHAGATBelum ada peringkat

- Fiscal Deficits Interest Rates and InflationDokumen9 halamanFiscal Deficits Interest Rates and InflationSatish BindumadhavanBelum ada peringkat

- The Relationship Between Economic Growth and Inflation in New ZealandDokumen18 halamanThe Relationship Between Economic Growth and Inflation in New ZealandRohol Amin RajuBelum ada peringkat

- Chapter Two Risk and Return 2.1. RiskDokumen10 halamanChapter Two Risk and Return 2.1. RiskSeid KassawBelum ada peringkat

- Unit 3Dokumen16 halamanUnit 3smit9993Belum ada peringkat

- Strategies LOW VOLATILITYDokumen8 halamanStrategies LOW VOLATILITYbla blaBelum ada peringkat

- Chap 030Dokumen18 halamanChap 030George WagihBelum ada peringkat

- Navigating by R : Safe or Hazardous?Dokumen19 halamanNavigating by R : Safe or Hazardous?DavidBelum ada peringkat

- Risk Parity - The Truly Balanced Portfolio - Magazine - IPE - Ray DalioDokumen4 halamanRisk Parity - The Truly Balanced Portfolio - Magazine - IPE - Ray Daliokuky6549369Belum ada peringkat

- Effects of Inflation AlchianDokumen18 halamanEffects of Inflation AlchianCoco 12Belum ada peringkat

- A Guide To Portfolio HedgingDokumen18 halamanA Guide To Portfolio Hedgingdmytro.khullaBelum ada peringkat

- Is A Less Pro-Cyclical Financial System An Achievable Goal?Dokumen27 halamanIs A Less Pro-Cyclical Financial System An Achievable Goal?api-26091012Belum ada peringkat

- 18 Portfolio Management Capital Market Theory Basic ConceptsDokumen17 halaman18 Portfolio Management Capital Market Theory Basic ConceptsSin MelmondBelum ada peringkat

- Dynamic Correlations: The Implications For Portfolio ConstructionDokumen14 halamanDynamic Correlations: The Implications For Portfolio ConstructionNIKITA GUPTABelum ada peringkat

- An Introduction To Inflation-Linked Bonds: Investment ResearchDokumen12 halamanAn Introduction To Inflation-Linked Bonds: Investment ResearchMatt EbrahimiBelum ada peringkat

- Topic2 Risk and ReturnDokumen21 halamanTopic2 Risk and ReturnMirza VejzagicBelum ada peringkat

- INFLATIONDokumen20 halamanINFLATIONsamuel karateBelum ada peringkat

- Ilmanen Kizer 2012 Death of Diversification ExaggeratedDokumen14 halamanIlmanen Kizer 2012 Death of Diversification Exaggeratedroblee1Belum ada peringkat

- Unlisted Infrastructure - Proven PerformerDokumen4 halamanUnlisted Infrastructure - Proven PerformerjleungcmBelum ada peringkat

- Agriculture and Fishery Arts Handout 3Dokumen9 halamanAgriculture and Fishery Arts Handout 3Jonas CabacunganBelum ada peringkat

- Assets AllocationDokumen16 halamanAssets AllocationkavyaBelum ada peringkat

- Economia - Articulo - Es.enDokumen37 halamanEconomia - Articulo - Es.enSebastian Jaramillo GilBelum ada peringkat

- Deflation - Making Sure It Doesn't Happen Here (Ben S. Bernanke)Dokumen8 halamanDeflation - Making Sure It Doesn't Happen Here (Ben S. Bernanke)João Henrique F. VieiraBelum ada peringkat

- PortfolioDokumen18 halamanPortfolioheyBelum ada peringkat

- GS Guide To Inflation-Linked BondsDokumen8 halamanGS Guide To Inflation-Linked BondsOmer H.Belum ada peringkat

- WhereDokumen3 halamanWhereRexi Chynna Maning - AlcalaBelum ada peringkat

- Smu Asignment 303Dokumen8 halamanSmu Asignment 303Mukesh AgarwalBelum ada peringkat

- THE SOCIAL SCIENCE OF ECONOMICS COMMON TERMS AND DEFINITIONSDari EverandTHE SOCIAL SCIENCE OF ECONOMICS COMMON TERMS AND DEFINITIONSBelum ada peringkat

- Target Date Funds Still Under AttackDokumen6 halamanTarget Date Funds Still Under AttackRoman PolnarBelum ada peringkat

- BRS Market Report: Week II: 5Dokumen7 halamanBRS Market Report: Week II: 5Sudheera IndrajithBelum ada peringkat

- FIMA 30013 FS Analysis Premium FSDokumen4 halamanFIMA 30013 FS Analysis Premium FSdcdeguzman.pup.pulilanBelum ada peringkat

- Advanced Option Strategies NotebookDokumen78 halamanAdvanced Option Strategies NotebookCapavara Lin100% (4)

- Bloomberg Excel Add-In Tutorial: October 3, 2013Dokumen7 halamanBloomberg Excel Add-In Tutorial: October 3, 2013Apurva Soumya100% (1)

- Iecmd - Jan 2020Dokumen79 halamanIecmd - Jan 2020Steven Wang100% (1)

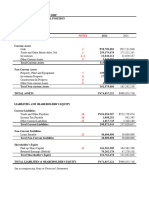

- Laporan Keuangan ASSIDokumen3 halamanLaporan Keuangan ASSITiti MuntiartiBelum ada peringkat

- SCHW 2022 Winter Business Update 012822Dokumen134 halamanSCHW 2022 Winter Business Update 012822Jamie EdwardsBelum ada peringkat

- Intermediate Accounting IFRS 3rd EditionDokumen20 halamanIntermediate Accounting IFRS 3rd EditionMalik MaulanaBelum ada peringkat

- Finance 1 Modules 3-6Dokumen58 halamanFinance 1 Modules 3-6MTECH ASIABelum ada peringkat

- Module 2 Math of InvestmentDokumen17 halamanModule 2 Math of InvestmentvlythevergreenBelum ada peringkat

- Case 8Dokumen3 halamanCase 8Neil GumbanBelum ada peringkat

- BIM Experiences and Expectations: The Constructors' PerspectiveDokumen24 halamanBIM Experiences and Expectations: The Constructors' PerspectiveArifBelum ada peringkat

- SMCH 05Dokumen73 halamanSMCH 05FratFool100% (1)

- Basel ReportDokumen8 halamanBasel ReportskenkanBelum ada peringkat

- MCQDokumen6 halamanMCQTariq Hussain Khan100% (1)

- IFIC Bank Internship ReportDokumen136 halamanIFIC Bank Internship ReportAppleBelum ada peringkat

- Derivatives (Fin402) : Assignment: EssayDokumen5 halamanDerivatives (Fin402) : Assignment: EssayNga Thị NguyễnBelum ada peringkat

- MBA 502 Financial Accounting AssignmentDokumen4 halamanMBA 502 Financial Accounting AssignmentNil AkashBelum ada peringkat

- Effect of Glob On WomenDokumen36 halamanEffect of Glob On WomenRahul JeshnaniBelum ada peringkat

- Accenture Strategy ZBX Zero Based Transformation POV July2019Dokumen9 halamanAccenture Strategy ZBX Zero Based Transformation POV July2019Deepak SharmaBelum ada peringkat

- Analisis Finansial Penggemukan Kambing Peranakan Boer F1 Di Perusahaan Peternakan CV. Agriranch Karangploso MalangDokumen6 halamanAnalisis Finansial Penggemukan Kambing Peranakan Boer F1 Di Perusahaan Peternakan CV. Agriranch Karangploso MalangIlhammBelum ada peringkat

- Notes - Chapter 4Dokumen6 halamanNotes - Chapter 4OneishaL.HughesBelum ada peringkat

- Solution Manual For Corporate Finance 4th Edition by BerkDokumen3 halamanSolution Manual For Corporate Finance 4th Edition by Berka38476880414% (7)

- Pre-Test 4Dokumen3 halamanPre-Test 4BLACKPINKLisaRoseJisooJennieBelum ada peringkat

- Sales AgreementDokumen1 halamanSales AgreementPhillip KingBelum ada peringkat

- ING Group 2Dokumen4 halamanING Group 2Puneet JainBelum ada peringkat

- Brand ArchitectureDokumen8 halamanBrand ArchitectureNabeelah Moses100% (1)

- Investment IDokumen30 halamanInvestment IbarchajacBelum ada peringkat

- Prop-Tech Latam 2022 Latitud ReportDokumen46 halamanProp-Tech Latam 2022 Latitud ReportCristobal FlorenzanoBelum ada peringkat

- Cee Guide To LNGDokumen2 halamanCee Guide To LNGNatalia Magaia CambaBelum ada peringkat