Anda mungkin juga menyukai

- Monetary Policy in IndiaDokumen8 halamanMonetary Policy in Indiaamitwaghela50Belum ada peringkat

- Monetary Policy Chapter 1Dokumen16 halamanMonetary Policy Chapter 1faliyarahulBelum ada peringkat

- Monetary Policy RBI.Dokumen28 halamanMonetary Policy RBI.santoshys50% (2)

- Eco 326 Assignment 1 Group 11Dokumen6 halamanEco 326 Assignment 1 Group 11stanely ndlovuBelum ada peringkat

- Finance Basics - Monetary Policy and Inflation ExplainedDokumen3 halamanFinance Basics - Monetary Policy and Inflation ExplainedAkash MahalikBelum ada peringkat

- The Impact of Money Supply On Economic Growth in India: Student's Name: Student's ID: DateDokumen17 halamanThe Impact of Money Supply On Economic Growth in India: Student's Name: Student's ID: DateReeya ElixirBelum ada peringkat

- Monetary PolicyDokumen10 halamanMonetary PolicyAshish MisraBelum ada peringkat

- Introduction To Economics and FinanceDokumen10 halamanIntroduction To Economics and FinanceShanti Prakhar AwasthiBelum ada peringkat

- Prince Monetary PolicyDokumen12 halamanPrince Monetary Policyrohit707Belum ada peringkat

- Significant Bad Debts On Loans?Dokumen5 halamanSignificant Bad Debts On Loans?imehmood88Belum ada peringkat

- Unit 16 Equilibrium in Money Market: 16.0 ObjectivesDokumen14 halamanUnit 16 Equilibrium in Money Market: 16.0 ObjectivesAjeet KumarBelum ada peringkat

- Monetary Policy Is The Process by Which TheDokumen4 halamanMonetary Policy Is The Process by Which TheS_JITHBelum ada peringkat

- Macroeconomics AssignmentDokumen12 halamanMacroeconomics AssignmentAkhil NarangBelum ada peringkat

- Monetary Policy Operations: Demand-Supply CurveDokumen2 halamanMonetary Policy Operations: Demand-Supply CurveNeha MahmoodBelum ada peringkat

- Unit II The Concept of Money SupplyDokumen24 halamanUnit II The Concept of Money SupplyLoungo GopaneBelum ada peringkat

- Evidence of Interest Rate Channel of Monetary Policy Transmission in IndiaDokumen53 halamanEvidence of Interest Rate Channel of Monetary Policy Transmission in IndiaNitish SikandBelum ada peringkat

- Money SupplyDokumen31 halamanMoney SupplyDivya JainBelum ada peringkat

- F 309 Group 6 FinalDokumen18 halamanF 309 Group 6 FinalMD Alamin 25-125Belum ada peringkat

- Paper For ISAC Journal For Udaipur Conference 2015Dokumen15 halamanPaper For ISAC Journal For Udaipur Conference 2015jainish_bhagatBelum ada peringkat

- Government Influence On Exchange Rate in BangladeshDokumen22 halamanGovernment Influence On Exchange Rate in BangladeshOmar50% (2)

- Theories of Money SupplyDokumen15 halamanTheories of Money SupplyAppan Kandala Vasudevachary100% (1)

- Interest Rates and ImpactsDokumen6 halamanInterest Rates and ImpactsSunny KalraBelum ada peringkat

- Economic TermsDokumen7 halamanEconomic TermsHimani MehtaBelum ada peringkat

- Monetary Policy ToolsDokumen7 halamanMonetary Policy ToolsDeepak PathakBelum ada peringkat

- Mohd. Moktasid Hossain Bhuiyan ID: 19304024Dokumen2 halamanMohd. Moktasid Hossain Bhuiyan ID: 19304024Moktasid HossainBelum ada peringkat

- What is monetary and fiscal policyDokumen27 halamanWhat is monetary and fiscal policynohel01100% (1)

- Money Supply and Banking System ProjectDokumen15 halamanMoney Supply and Banking System ProjectFaraz AhmadBelum ada peringkat

- Relationship Between Macroeconomic Variables and Monetary Policy in KenyaDokumen29 halamanRelationship Between Macroeconomic Variables and Monetary Policy in KenyaSimon MutekeBelum ada peringkat

- Economic S2 Reduction.Dokumen13 halamanEconomic S2 Reduction.062 Prajwal.R. SataoBelum ada peringkat

- Analisis Permintaan Dan Penawaran Uang Di Indonesia: Muhammad Andi PrayogiDokumen10 halamanAnalisis Permintaan Dan Penawaran Uang Di Indonesia: Muhammad Andi Prayogidwi fuji cahyantiBelum ada peringkat

- Money and Inflation: Chapter FourDokumen56 halamanMoney and Inflation: Chapter FourahmeddanafBelum ada peringkat

- Research Title:: "The Role of Monetary Policy On Inflation in Developing Country"Dokumen14 halamanResearch Title:: "The Role of Monetary Policy On Inflation in Developing Country"Zaina RathoreBelum ada peringkat

- Measuring price stability and monetary policy options in BangladeshDokumen15 halamanMeasuring price stability and monetary policy options in BangladeshDipayan_luBelum ada peringkat

- The Money Supply Process and Implications of Bad DebtsDokumen4 halamanThe Money Supply Process and Implications of Bad Debtsimehmood88Belum ada peringkat

- A Study On The Impact of RBI Monetary Policies On Indian Stock MarketDokumen63 halamanA Study On The Impact of RBI Monetary Policies On Indian Stock MarketNavaneeth GsBelum ada peringkat

- 3 Macroeconomic Policies ExplainedDokumen8 halaman3 Macroeconomic Policies ExplainedRaul JainBelum ada peringkat

- Interest Rates and Inflation: Federal Reserve Bank of Minneapolis Research DepartmentDokumen19 halamanInterest Rates and Inflation: Federal Reserve Bank of Minneapolis Research DepartmentHarshit JainBelum ada peringkat

- Provide A Definition ofDokumen6 halamanProvide A Definition ofGiovanniDelGrecoBelum ada peringkat

- Impact of Macroeconomic Factors On Money SupplyDokumen30 halamanImpact of Macroeconomic Factors On Money Supplyshrekdj88% (8)

- Section B - Group 3Dokumen1 halamanSection B - Group 3swapnil tyagiBelum ada peringkat

- Reserve Bank of India:-: On What Bases RBI Print CurrencyDokumen5 halamanReserve Bank of India:-: On What Bases RBI Print CurrencyNavjot MannBelum ada peringkat

- FINAL Paper - Inflation Targeting Framework of The BSPDokumen17 halamanFINAL Paper - Inflation Targeting Framework of The BSPLeyCodes LeyCodes100% (1)

- Inflation Targeting Framework: Indonesia in ComparisonDokumen25 halamanInflation Targeting Framework: Indonesia in ComparisonPrasya AnindityaBelum ada peringkat

- Principles of MacroeconomicsDokumen52 halamanPrinciples of Macroeconomicsmoaz21100% (1)

- How To Analyze The Stock MarketDokumen9 halamanHow To Analyze The Stock MarketantumanipadamBelum ada peringkat

- What Is It?: Importance of Inflation and GDP.)Dokumen3 halamanWhat Is It?: Importance of Inflation and GDP.)Arun_Prasath_1679Belum ada peringkat

- Economy Gross Domestic Product Inflation: What Does Macroeconomics Mean?Dokumen8 halamanEconomy Gross Domestic Product Inflation: What Does Macroeconomics Mean?Parth GargBelum ada peringkat

- Topic-Impact of Demonetization On The Economy of India Submitted By, Tanay Bothra Bba LLB Semester Ii Economics Ii Division-F Roll No - F008Dokumen20 halamanTopic-Impact of Demonetization On The Economy of India Submitted By, Tanay Bothra Bba LLB Semester Ii Economics Ii Division-F Roll No - F008Tanay BothraBelum ada peringkat

- Mba ProjectDokumen8 halamanMba Projectakmundada123Belum ada peringkat

- Macro-Economics of Financial Markets BFM Black BookDokumen74 halamanMacro-Economics of Financial Markets BFM Black BookJameson KurianBelum ada peringkat

- Monetary Policy and Money SupplyDokumen68 halamanMonetary Policy and Money SupplypearlksrBelum ada peringkat

- Literature Review On Money Supply and InflationDokumen5 halamanLiterature Review On Money Supply and Inflationea8dpyt0100% (1)

- The Financial Sector of The Economy: Money and BankingDokumen12 halamanThe Financial Sector of The Economy: Money and BankingNefta BaptisteBelum ada peringkat

- CB GOALS AND TOOLS FOR MONETARY POLICYDokumen26 halamanCB GOALS AND TOOLS FOR MONETARY POLICYZayed Mohammad JohnyBelum ada peringkat

- Demonetization Through Segmented MarketsDokumen9 halamanDemonetization Through Segmented MarketsParag WaknisBelum ada peringkat

- RupeeDokumen5 halamanRupeeGarveet ModiBelum ada peringkat

- Stock Market and Foreign Exchange Market: An Empirical GuidanceDari EverandStock Market and Foreign Exchange Market: An Empirical GuidanceBelum ada peringkat

- Inflation Hacking: Inflation Investing Techniques to Benefit from High InflationDari EverandInflation Hacking: Inflation Investing Techniques to Benefit from High InflationBelum ada peringkat

- Exchange Rate Determination Puzzle: Long Run Behavior and Short Run DynamicsDari EverandExchange Rate Determination Puzzle: Long Run Behavior and Short Run DynamicsBelum ada peringkat

- Unit 1 Mefa Material-Word DocumentDokumen33 halamanUnit 1 Mefa Material-Word DocumentrosieBelum ada peringkat

- IMT Covid19Dokumen10 halamanIMT Covid19Ganesh MisraBelum ada peringkat

- Hamed Fazlollahtabar - Supply Chain Management Models - Forward, Reverse, Uncertain, and Intelligent Foundations With Case Studies (2018, CRC Press) PDFDokumen401 halamanHamed Fazlollahtabar - Supply Chain Management Models - Forward, Reverse, Uncertain, and Intelligent Foundations With Case Studies (2018, CRC Press) PDFJohn Acid100% (2)

- Module 16 SupplyDokumen6 halamanModule 16 SupplyOlive OrpillaBelum ada peringkat

- (MARCUS WARREN) Economic Analysis For Property and PDFDokumen269 halaman(MARCUS WARREN) Economic Analysis For Property and PDFMyagmartuvshin LkhagvajavBelum ada peringkat

- Worksheet - 2 Demand & SupplyDokumen2 halamanWorksheet - 2 Demand & SupplyPrince SingalBelum ada peringkat

- Module-2: Cost and Revenue, Profit FunctionsDokumen37 halamanModule-2: Cost and Revenue, Profit FunctionsArpitha KagdasBelum ada peringkat

- Microeconomics FINAL EXAM For StudentsDokumen16 halamanMicroeconomics FINAL EXAM For Studentsakpe12340% (1)

- Microeconomics I - Chapter FiveDokumen36 halamanMicroeconomics I - Chapter FiveGena DuresaBelum ada peringkat

- Economics IGCSE Course Book AnswersDokumen37 halamanEconomics IGCSE Course Book AnswerscarltonmusenzeBelum ada peringkat

- Mcqs Demand ChapterDokumen19 halamanMcqs Demand ChapterAbdul-Ghaffar Kalhoro100% (1)

- Applied EconomicsDokumen184 halamanApplied EconomicsMichael ZinampanBelum ada peringkat

- Determine The Factors Affect InflactionDokumen10 halamanDetermine The Factors Affect InflactionClare WongBelum ada peringkat

- Presentation: Principles of EconomicsDokumen22 halamanPresentation: Principles of EconomicsDhanuhsBelum ada peringkat

- Chapter 1 6Dokumen79 halamanChapter 1 6Shundei Otawara100% (1)

- HS 252 Economics HW Analyzes Supply & DemandDokumen11 halamanHS 252 Economics HW Analyzes Supply & DemandHania AliBelum ada peringkat

- Methods of Demand ForecastingDokumen15 halamanMethods of Demand ForecastingParandhaman GRBelum ada peringkat

- BA LLB Economics Microeconomic AnalysisDokumen45 halamanBA LLB Economics Microeconomic AnalysisSimar KaurBelum ada peringkat

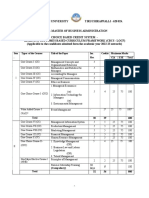

- MBA Syllabus 2022-23Dokumen162 halamanMBA Syllabus 2022-23Trichy MaheshBelum ada peringkat

- F1 TNMDokumen35 halamanF1 TNMNguyễn Lê MinhBelum ada peringkat

- Demand and supply determine priceDokumen23 halamanDemand and supply determine pricemelody b. plazaBelum ada peringkat

- International Trade Finance SlidesDokumen233 halamanInternational Trade Finance SlidesThomas ackonBelum ada peringkat

- Important Diagrams PDFDokumen43 halamanImportant Diagrams PDFapi-260512563Belum ada peringkat

- SOL BA Program 1st Year Economics Study Material and Syllabus in PDFDokumen88 halamanSOL BA Program 1st Year Economics Study Material and Syllabus in PDFShamim Akhtar83% (23)

- APPLIED ECONOMICS - PPTX NEWDokumen19 halamanAPPLIED ECONOMICS - PPTX NEWBenjie A. IbutBelum ada peringkat

- Understanding Keynesian Cross Model and Fiscal Policy MultipliersDokumen30 halamanUnderstanding Keynesian Cross Model and Fiscal Policy MultiplierswaysBelum ada peringkat

- Technical Analysis From A To ZDokumen222 halamanTechnical Analysis From A To ZPraveen R VBelum ada peringkat

- Unit Code: BM533 Unit Title: Contemporary Business EconomicsDokumen17 halamanUnit Code: BM533 Unit Title: Contemporary Business EconomicsLucifer 3013100% (1)

- FYBCOM Business Economics Sem IDokumen116 halamanFYBCOM Business Economics Sem IDarshan Tajne100% (1)

- Dms 111 Manual by Michael K. Chirchir and Githii WainainaDokumen173 halamanDms 111 Manual by Michael K. Chirchir and Githii WainainaAdventist NaturopathyBelum ada peringkat