Anda mungkin juga menyukai

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- What Happened To The Constitution Presentation Docs LDokumen121 halamanWhat Happened To The Constitution Presentation Docs Lncwazzy100% (1)

- American Standard of Jurisdictional Hierarchy 1Dokumen6 halamanAmerican Standard of Jurisdictional Hierarchy 1LEBJBelum ada peringkat

- The Fraud of Bank LoansDokumen62 halamanThe Fraud of Bank Loansncwazzy100% (25)

- Secret Banker's ManualDokumen75 halamanSecret Banker's Manualncwazzy100% (4)

- Society of SlavesDokumen52 halamanSociety of Slavesncwazzy100% (3)

- Page 25Dokumen1 halamanPage 25ncwazzyBelum ada peringkat

- Modern Money Mechanics PDFDokumen40 halamanModern Money Mechanics PDFwestelm12Belum ada peringkat

- Bankers AcceptancesDokumen36 halamanBankers AcceptancesAlexhCreditorBelum ada peringkat

- Page 23Dokumen1 halamanPage 23ncwazzyBelum ada peringkat

- COIN's Financial School (1894)Dokumen180 halamanCOIN's Financial School (1894)Ragnar Danneskjold100% (1)

- Treatise Superior Law Higher Law My LawDokumen54 halamanTreatise Superior Law Higher Law My Law1 watchman100% (2)

- David H Friedman I Bet You ThoughtDokumen36 halamanDavid H Friedman I Bet You Thoughtncwazzy100% (3)

- Spiritual RichesDokumen93 halamanSpiritual RichesAdam Lloyd DavisBelum ada peringkat

- Treatise SovereigntyDokumen46 halamanTreatise Sovereignty1 watchman100% (1)

- Congressional Record 600-799Dokumen200 halamanCongressional Record 600-799ncwazzyBelum ada peringkat

- Principles of Banking PDFDokumen8 halamanPrinciples of Banking PDFdbush1034Belum ada peringkat

- 15646Dokumen6 halaman15646ncwazzy100% (1)

- The Law Merchant PDFDokumen57 halamanThe Law Merchant PDFwill100% (4)

- Congressional Record 200 - 399Dokumen200 halamanCongressional Record 200 - 399ncwazzyBelum ada peringkat

- Society of SlavesDokumen52 halamanSociety of Slavesncwazzy100% (3)

- Con RecDokumen2 halamanCon Recncwazzy100% (1)

- Congressional Record 400-599Dokumen200 halamanCongressional Record 400-599ncwazzyBelum ada peringkat

- McFadden On The Federal Res.Dokumen9 halamanMcFadden On The Federal Res.ncwazzyBelum ada peringkat

- Congressional Record 1 - 199Dokumen199 halamanCongressional Record 1 - 199ncwazzyBelum ada peringkat

- Congressional Record 1000-1159Dokumen159 halamanCongressional Record 1000-1159ncwazzyBelum ada peringkat

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (74)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- Hyston International Trade Co.,Limited: NO.290 Wangjiazhuang Industrial Park, Shangma Street, Chengyang Dist, Qingdao ChinaDokumen1 halamanHyston International Trade Co.,Limited: NO.290 Wangjiazhuang Industrial Park, Shangma Street, Chengyang Dist, Qingdao Chinar34syaBelum ada peringkat

- BB UD WirastriDokumen40 halamanBB UD WirastriFellisa SusantiBelum ada peringkat

- Office of The PO Cum DWO, PURULIA District: Government of West BengalDokumen3 halamanOffice of The PO Cum DWO, PURULIA District: Government of West BengalJharna RoyBelum ada peringkat

- MDP Nomination FormDokumen2 halamanMDP Nomination FormShivam ChaudharyBelum ada peringkat

- Citi Short Sale Approval Letter (Non-GSE)Dokumen2 halamanCiti Short Sale Approval Letter (Non-GSE)kwillsonBelum ada peringkat

- MGT202 Lecture 02.ppsxDokumen12 halamanMGT202 Lecture 02.ppsxBashir Ahmad100% (1)

- T03 - Working Capital FinanceDokumen40 halamanT03 - Working Capital FinanceJesha JotojotBelum ada peringkat

- Ejaz Naseer NBP Reprort 2018Dokumen58 halamanEjaz Naseer NBP Reprort 2018Tayyab ali gardaziBelum ada peringkat

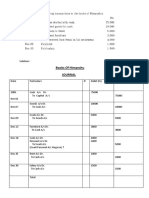

- Books of Himanshu JournalDokumen4 halamanBooks of Himanshu Journalrakesh19865Belum ada peringkat

- Bill Statement: Previous Charges Amount (RM) Current Charges Amount (RM)Dokumen7 halamanBill Statement: Previous Charges Amount (RM) Current Charges Amount (RM)WM Iskandar100% (1)

- BDO Vs RepublicDokumen2 halamanBDO Vs RepublicAngel Phyllis PriasBelum ada peringkat

- TifrDokumen3 halamanTifrgrasheedBelum ada peringkat

- Cash Book & Bank Reconciliation StatementDokumen2 halamanCash Book & Bank Reconciliation Statementst_mosviBelum ada peringkat

- ExportDokumen28 halamanExportNagarjun AithaBelum ada peringkat

- Business Studies Class11 Chapter 4Dokumen8 halamanBusiness Studies Class11 Chapter 4bhawnaBelum ada peringkat

- (2018) US-China Trade War WFR: December 2018Dokumen7 halaman(2018) US-China Trade War WFR: December 2018Mario Roger HernándezBelum ada peringkat

- Arabi Bin Hamzah No 521 Lot 6746 JLN Sultan Tengah Samariang Aman Phase 4 93050 KUCHING, SARDokumen3 halamanArabi Bin Hamzah No 521 Lot 6746 JLN Sultan Tengah Samariang Aman Phase 4 93050 KUCHING, SARcancalokBelum ada peringkat

- Environment and Land Case 941 947 of 2016 ConsolidatedDokumen10 halamanEnvironment and Land Case 941 947 of 2016 ConsolidatedSkarra Adebolaye AbayomiBelum ada peringkat

- Presentation - RbiDokumen10 halamanPresentation - Rbianandvishnubnair72% (18)

- Guthrie-Jensen - Corporate ProfileDokumen8 halamanGuthrie-Jensen - Corporate ProfileRalph GuzmanBelum ada peringkat

- 1.kobank Application Form (Pls Print in Color)Dokumen1 halaman1.kobank Application Form (Pls Print in Color)api-19759090Belum ada peringkat

- BOC Main Branch ContactDokumen3 halamanBOC Main Branch ContactshakecokeBelum ada peringkat

- Accounting Basics 3Dokumen74 halamanAccounting Basics 3Mukund kelaBelum ada peringkat

- Afm MCQDokumen10 halamanAfm MCQSarannya PillaiBelum ada peringkat

- History of BankDokumen9 halamanHistory of Bankanon_394906720Belum ada peringkat

- NIC Account BenefitsDokumen4 halamanNIC Account BenefitsAnkit UpretyBelum ada peringkat

- 0809 B&E SeptDokumen118 halaman0809 B&E Septhsrivastava703Belum ada peringkat

- Sap Liquidity PlannerDokumen48 halamanSap Liquidity Plannerabrondi100% (2)

- Commercial Law ReviewDokumen3 halamanCommercial Law ReviewElijahBactolBelum ada peringkat

- Interview-Letter Apply NowDokumen3 halamanInterview-Letter Apply NowSheikh IrfanBelum ada peringkat