Anda mungkin juga menyukai

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (399)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (73)

- Bil U MobileDokumen6 halamanBil U MobileTeruna ImpianBelum ada peringkat

- Commercial Law ReviewDokumen27 halamanCommercial Law ReviewimianmoralesBelum ada peringkat

- Flexcube QuestionsDokumen4 halamanFlexcube QuestionsSreepad Rao KanugoviBelum ada peringkat

- Bank AsiaDokumen26 halamanBank AsiaAsad Nabil100% (2)

- CASE DIGEST Lopez Vs OrosaDokumen1 halamanCASE DIGEST Lopez Vs OrosaErica Dela Cruz100% (1)

- Role of Self Help Groups in Financial InclusionDokumen6 halamanRole of Self Help Groups in Financial InclusionSona Kool100% (1)

- PROPERTYDokumen2 halamanPROPERTYChaMcband100% (1)

- Module Inc TaxDokumen7 halamanModule Inc TaxSree DasBelum ada peringkat

- Tax PlanningDokumen1 halamanTax PlanningSree DasBelum ada peringkat

- PPM (S) EmbacDokumen2 halamanPPM (S) EmbacSree DasBelum ada peringkat

- Shipping Management EMBADokumen4 halamanShipping Management EMBASree DasBelum ada peringkat

- 123 Operations MGT EMBADokumen1 halaman123 Operations MGT EMBASree DasBelum ada peringkat

- HRM (S)Dokumen1 halamanHRM (S)Sree DasBelum ada peringkat

- IntERNATIONAL BUZ EMBADokumen1 halamanIntERNATIONAL BUZ EMBASree DasBelum ada peringkat

- EMBA Marketing MGTDokumen1 halamanEMBA Marketing MGTSree DasBelum ada peringkat

- Consumer BehaviorDokumen1 halamanConsumer BehaviorSree DasBelum ada peringkat

- Consumer BehaviorDokumen1 halamanConsumer BehaviorSree DasBelum ada peringkat

- Case Study ApprochDokumen4 halamanCase Study Approchkeyanmaker0% (1)

- Subject: Business Ethics: An Iso 9001: 2008 Certified International B-SchoolDokumen2 halamanSubject: Business Ethics: An Iso 9001: 2008 Certified International B-SchoolSree DasBelum ada peringkat

- Subject: Advertising Management: An Iso 9001: 2008 Certified International B-SchoolDokumen1 halamanSubject: Advertising Management: An Iso 9001: 2008 Certified International B-SchoolSree DasBelum ada peringkat

- Chp8 3edition PDFDokumen21 halamanChp8 3edition PDFAbarajithan RajendranBelum ada peringkat

- Reliance Money Project ReportDokumen12 halamanReliance Money Project Reportmysterio666Belum ada peringkat

- Explanation of deductions for certain payments under Section 37Dokumen2 halamanExplanation of deductions for certain payments under Section 37NISHANTH JOSEBelum ada peringkat

- Eobi Loan RegDokumen6 halamanEobi Loan RegEOBI FEDERATION100% (1)

- Purchase order email for wooden souvenirsDokumen5 halamanPurchase order email for wooden souvenirsArif Reza MaharamaBelum ada peringkat

- Conceptual Errors in GSTDokumen5 halamanConceptual Errors in GSTKalyani BorkarBelum ada peringkat

- Investment Holding Company (IHC): Key AspectsDokumen52 halamanInvestment Holding Company (IHC): Key AspectsMin Li67% (3)

- Amanah BankDokumen3 halamanAmanah BankMaannavie MarcosBelum ada peringkat

- Raghuram G. RajanDokumen10 halamanRaghuram G. RajanyogeshBelum ada peringkat

- Determinants Of Household Access To Formal Credit In Rural VietnamDokumen33 halamanDeterminants Of Household Access To Formal Credit In Rural VietnamGunk Alit Part IIBelum ada peringkat

- Book Report Bank of BarodaDokumen13 halamanBook Report Bank of BarodaYash HemnaniBelum ada peringkat

- Sbiepay Sbiepay: Sbi Branch Payment Challan Sbi Branch Payment ChallanDokumen1 halamanSbiepay Sbiepay: Sbi Branch Payment Challan Sbi Branch Payment ChallanKishore TadinadaBelum ada peringkat

- Products & Services and Marketing Startegies of Kotak Mahindra BankDokumen64 halamanProducts & Services and Marketing Startegies of Kotak Mahindra Bankmandiratta100% (1)

- China Nigeria Bilateral Currency Swap Agreement A Cost Benefit Analysis of The PolicyDokumen8 halamanChina Nigeria Bilateral Currency Swap Agreement A Cost Benefit Analysis of The PolicyMoussaLoloBelum ada peringkat

- Microfinance Provision in Ethiopia: September 2020Dokumen11 halamanMicrofinance Provision in Ethiopia: September 2020yeshitilaBelum ada peringkat

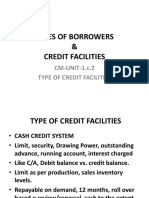

- CM Unit 1.c.2 TYPES of Credit FacilitiesDokumen8 halamanCM Unit 1.c.2 TYPES of Credit Facilitiesabdullahi shafiuBelum ada peringkat

- Operational Risk: An Overview: Dr. Richa Verma BajajDokumen37 halamanOperational Risk: An Overview: Dr. Richa Verma BajajJoydeep DuttaBelum ada peringkat

- Chevron HeadquartersDokumen2 halamanChevron HeadquartersGunjan DoshiBelum ada peringkat

- Central Bank Regulation of Kenyan Commercial BanksDokumen3 halamanCentral Bank Regulation of Kenyan Commercial BanksWesleyBelum ada peringkat

- Macroeconomics: Case Fair OsterDokumen33 halamanMacroeconomics: Case Fair OsterThalia SandersBelum ada peringkat

- Advantages of Auditing Accounts for BusinessesDokumen3 halamanAdvantages of Auditing Accounts for BusinessesNikita ChavanBelum ada peringkat

- Electrotherm India LTD PDFDokumen11 halamanElectrotherm India LTD PDFTarun ChakrabortyBelum ada peringkat

- AAA Fraud Shailesh J. Mehta PH.DDokumen3 halamanAAA Fraud Shailesh J. Mehta PH.DThomas ScharrerBelum ada peringkat