Anda mungkin juga menyukai

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5795)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (74)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- Nifty 50 Companies Logo'sDokumen6 halamanNifty 50 Companies Logo'sbhas6302Belum ada peringkat

- The Ultimate Options Trading ST - Roji AbrahamDokumen170 halamanThe Ultimate Options Trading ST - Roji Abrahamcodingfreek007Belum ada peringkat

- Pre-Market PulseDokumen8 halamanPre-Market Pulseayush7376307320Belum ada peringkat

- NSDL HoldingDokumen5 halamanNSDL HoldingJaydeep DoshiBelum ada peringkat

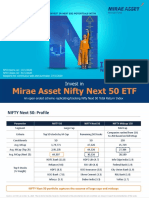

- Mirae Asset Nifty Next 50 Etf - Final PresentationDokumen27 halamanMirae Asset Nifty Next 50 Etf - Final PresentationHetanshBelum ada peringkat

- Speciality Chemicals - Nirmal Bang - Rally JustifiedDokumen21 halamanSpeciality Chemicals - Nirmal Bang - Rally Justifiedvipul sharmaBelum ada peringkat

- Study of Stock Market Working FrameworkDokumen13 halamanStudy of Stock Market Working Frameworkbenjoel1209Belum ada peringkat

- Futures & Options SegmentDokumen36 halamanFutures & Options SegmentVijay MadhvanBelum ada peringkat

- Options Scalping Refresher DocumentDokumen25 halamanOptions Scalping Refresher DocumentChandrasekar Chandramohan95% (21)

- Statement of Axis Account No:914010029142900 For The Period (From: 01-04-2020 To: 31-03-2021)Dokumen14 halamanStatement of Axis Account No:914010029142900 For The Period (From: 01-04-2020 To: 31-03-2021)CA Nikhil MunjalBelum ada peringkat

- All Products Payout Structure Dec'23 13Dokumen8 halamanAll Products Payout Structure Dec'23 13Albert PeterBelum ada peringkat

- The Ine That We NeedDokumen8 halamanThe Ine That We NeedTyrion LannisterBelum ada peringkat

- CNX Nifty - Wikipedia, The Free EncyclopediaDokumen5 halamanCNX Nifty - Wikipedia, The Free Encyclopediapriyansh priyadarshiBelum ada peringkat

- Nifty DDKDK LFKDSFSDKFDK KF Sdkfdlsfkldskfds LLFKSLDLFKSLD KF DSKL FKLDSK Fks DKFKDKFKKF DSKFL DSFK LDSFK LKF LDK Lks LK K LK DK LL K LK KDokumen42 halamanNifty DDKDK LFKDSFSDKFDK KF Sdkfdlsfkldskfds LLFKSLDLFKSLD KF DSKL FKLDSK Fks DKFKDKFKKF DSKFL DSFK LDSFK LKF LDK Lks LK K LK DK LL K LK KVikas RockBelum ada peringkat

- SEBI Bulletin September 2019 Issue Word - PDokumen66 halamanSEBI Bulletin September 2019 Issue Word - Parti guptaBelum ada peringkat

- State Wise Banker DetailsDokumen6.584 halamanState Wise Banker DetailsAshwani KumarBelum ada peringkat

- National Stock Exchange of IndiaDokumen22 halamanNational Stock Exchange of IndiaParesh Narayan BagweBelum ada peringkat

- 1 Hour Bullish Divergence ChartinkDokumen35 halaman1 Hour Bullish Divergence ChartinksaiBelum ada peringkat

- IIM Sambalpur PI KIT 2021Dokumen110 halamanIIM Sambalpur PI KIT 2021Kaushal P.Belum ada peringkat

- Mini Project On NseDokumen19 halamanMini Project On Nsecharan tejaBelum ada peringkat

- Data For DeepakDokumen130 halamanData For DeepakAnshu GuptaBelum ada peringkat

- Method Nifty Shariah IndicesDokumen15 halamanMethod Nifty Shariah IndicesT BwrsxBelum ada peringkat

- NinftyDokumen16 halamanNinftysonalliBelum ada peringkat

- Aslam PDFDokumen75 halamanAslam PDFSangeethaBelum ada peringkat

- Shri - Vinod.C.H Shri - Sanjeev Kumar Shri - Rajagopalan SivasankaranDokumen6 halamanShri - Vinod.C.H Shri - Sanjeev Kumar Shri - Rajagopalan SivasankaranAmit KrBelum ada peringkat

- A Study On Investors Perception Towards Sharemarket in Sharekhan LTDDokumen10 halamanA Study On Investors Perception Towards Sharemarket in Sharekhan LTDSANAULLAH SULTANPURBelum ada peringkat

- Ak Non Tech BookDokumen195 halamanAk Non Tech BookDeore DnyaneshwarBelum ada peringkat

- Nifty and BankNifty Constituents and WeightageDokumen5 halamanNifty and BankNifty Constituents and WeightageDavid JosephBelum ada peringkat

- 15 Min Bullish Divergence ChartinkDokumen40 halaman15 Min Bullish Divergence Chartinkshivaji patilBelum ada peringkat

- Ind Nifty50Dokumen2 halamanInd Nifty50Venu MadhavBelum ada peringkat