Anda mungkin juga menyukai

- ACC 203 Ch04 SolutionDokumen10 halamanACC 203 Ch04 Solutionomaritani2005Belum ada peringkat

- 4 1aDokumen1 halaman4 1aWaritsa KupraditBelum ada peringkat

- ACTG115 - Ch04 SolutionsDokumen14 halamanACTG115 - Ch04 SolutionsxxmbetaBelum ada peringkat

- Examples Ch3 SolutionDokumen7 halamanExamples Ch3 SolutionNajwa Al-khateebBelum ada peringkat

- Reporting Financial Results: Practice Session and Revision LectureDokumen53 halamanReporting Financial Results: Practice Session and Revision LectureNurt TurdBelum ada peringkat

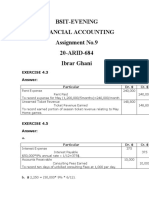

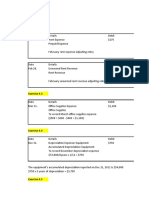

- Bsit-Evening Financial Accounting Assignment No.9 20-ARID-684 Ibrar GhaniDokumen3 halamanBsit-Evening Financial Accounting Assignment No.9 20-ARID-684 Ibrar Ghaniibrar ghani100% (1)

- Group Assignment - Questions - RevisedDokumen6 halamanGroup Assignment - Questions - Revised31231023949Belum ada peringkat

- Accounting Assignment Sample SolutionsDokumen20 halamanAccounting Assignment Sample SolutionsHebrew JohnsonBelum ada peringkat

- Here and On Page 88 Are Financial Statements of EdmistonDokumen1 halamanHere and On Page 88 Are Financial Statements of EdmistonM Bilal SaleemBelum ada peringkat

- CH 4 SolutionDokumen14 halamanCH 4 SolutionRody El KhalilBelum ada peringkat

- Solutions To Exercises - CHAP4Dokumen16 halamanSolutions To Exercises - CHAP4InciaBelum ada peringkat

- Solution Aassignments CH 12Dokumen7 halamanSolution Aassignments CH 12RuturajPatilBelum ada peringkat

- Summer ExamDokumen17 halamanSummer Examoliverchukwudi97Belum ada peringkat

- ACC 101 - CHP 3 Solutions To QS 3-1, QS 3-2, QS 3-3 & Ex 3-2Dokumen5 halamanACC 101 - CHP 3 Solutions To QS 3-1, QS 3-2, QS 3-3 & Ex 3-2KEVIN GORDONBelum ada peringkat

- Case Study 2Dokumen4 halamanCase Study 28142301001Belum ada peringkat

- Practice Homework Chapter 4 (25 Ed)Dokumen4 halamanPractice Homework Chapter 4 (25 Ed)Thomas TermoteBelum ada peringkat

- Exercises Chapter 04Dokumen23 halamanExercises Chapter 04vintcs181892Belum ada peringkat

- Unit 5: Worksheets: Worksheet 1 The Contents of Financial StatementsDokumen12 halamanUnit 5: Worksheets: Worksheet 1 The Contents of Financial StatementsSommerledBelum ada peringkat

- Mock 1 Mid-Term Exam (Answers and Explanations)Dokumen8 halamanMock 1 Mid-Term Exam (Answers and Explanations)100519554Belum ada peringkat

- Financial Accounting CH 4Dokumen21 halamanFinancial Accounting CH 4Israel MoraBelum ada peringkat

- Accounting CH1Dokumen5 halamanAccounting CH1shamseldeinhBelum ada peringkat

- Module 5 Activity SolutionsDokumen19 halamanModule 5 Activity SolutionsSushan Maharjan100% (3)

- Principles of Accounts IDokumen7 halamanPrinciples of Accounts IMohamed MubarakBelum ada peringkat

- C) D e P R e C I A T I o N o F F I X e D A S S e T SDokumen17 halamanC) D e P R e C I A T I o N o F F I X e D A S S e T SMohamed ZizoBelum ada peringkat

- Practice Questions Code 313, With AnswersDokumen19 halamanPractice Questions Code 313, With AnswersChang QiBelum ada peringkat

- First Exam (ch.1-5) PDFDokumen43 halamanFirst Exam (ch.1-5) PDFOmar HosnyBelum ada peringkat

- Hampton Suggested AnswersDokumen5 halamanHampton Suggested Answersenkay12100% (3)

- Adjustments Short CasesDokumen1 halamanAdjustments Short CasesMahmoud OkashaBelum ada peringkat

- Chapter 1 - Activity WorksheetDokumen3 halamanChapter 1 - Activity WorksheetHillary MoreyBelum ada peringkat

- Accounting IAS Model Answers Series 2 2010Dokumen17 halamanAccounting IAS Model Answers Series 2 2010Aung Zaw HtweBelum ada peringkat

- Tutorial On AdjustmentsDokumen8 halamanTutorial On AdjustmentsPushpa ValliBelum ada peringkat

- Debt Investments TutorialDokumen4 halamanDebt Investments TutorialRawan YasserBelum ada peringkat

- CH 4: Apply Your Knowledge Decision Case 4-1: Accounting 9/e Solutions Manual 392Dokumen15 halamanCH 4: Apply Your Knowledge Decision Case 4-1: Accounting 9/e Solutions Manual 392Loany Martinez100% (1)

- Class Exercise CH 4Dokumen9 halamanClass Exercise CH 4Iftekhar AhmedBelum ada peringkat

- ACC102 Final Examination ProblemDokumen8 halamanACC102 Final Examination ProblemtygurBelum ada peringkat

- Chapter Fifteen SolutionsDokumen21 halamanChapter Fifteen Solutionsapi-3705855Belum ada peringkat

- Practice Test Chap 34Dokumen7 halamanPractice Test Chap 34Mefa MefaiBelum ada peringkat

- Preparing Financial Statements: Key Terms and Concepts To KnowDokumen27 halamanPreparing Financial Statements: Key Terms and Concepts To KnowMohammed AkramBelum ada peringkat

- Preparing Financial Statements: Key Terms and Concepts To KnowDokumen27 halamanPreparing Financial Statements: Key Terms and Concepts To KnowTrisha Monique VillaBelum ada peringkat

- ACTG115 - Ch02 SolutionsDokumen16 halamanACTG115 - Ch02 SolutionsxxmbetaBelum ada peringkat

- Solutions To Brief Exercises - Chapter 12Dokumen12 halamanSolutions To Brief Exercises - Chapter 12Anh KietBelum ada peringkat

- Assignment No 2 FinalDokumen14 halamanAssignment No 2 FinalMuhammad AwaisBelum ada peringkat

- Mock 1 Mid-Term Exam AcountabilityDokumen6 halamanMock 1 Mid-Term Exam AcountabilityJhon WickBelum ada peringkat

- Solution Manual For Accounting 9th Edition by Charles T Horngren Walter T Harrison JR M Suzanne OliverDokumen39 halamanSolution Manual For Accounting 9th Edition by Charles T Horngren Walter T Harrison JR M Suzanne OliverPatriciaCooleyMDkrws100% (34)

- Financial Statements and Accounting Concepts/Principles: Category Financial Statement(s)Dokumen7 halamanFinancial Statements and Accounting Concepts/Principles: Category Financial Statement(s)cialeeBelum ada peringkat

- Student NameDokumen16 halamanStudent NameishwarsumeetBelum ada peringkat

- Acc 201 CH3Dokumen7 halamanAcc 201 CH3Trickster TwelveBelum ada peringkat

- Financial Analysis 4Dokumen10 halamanFinancial Analysis 4Alaitz GBelum ada peringkat

- EMBA Financial Accounting Re-Take Spring 2021 - PSR (6-4-2021)Dokumen4 halamanEMBA Financial Accounting Re-Take Spring 2021 - PSR (6-4-2021)Sheraz KhalilBelum ada peringkat

- Income Statement, Balance Sheet and Adjustments (2) - 1Dokumen11 halamanIncome Statement, Balance Sheet and Adjustments (2) - 1David-Lee Skinner-BallantyneBelum ada peringkat

- DUAZO - 6th EXAM SIM ANSWERSDokumen7 halamanDUAZO - 6th EXAM SIM ANSWERSJeric TorionBelum ada peringkat

- Yashpreet Kaur 7834156Dokumen8 halamanYashpreet Kaur 7834156Hardeep KaurBelum ada peringkat

- Acc3100 - Group 9Dokumen11 halamanAcc3100 - Group 9upunktschulzBelum ada peringkat

- Chapter 16 Sol 2020 WKDokumen53 halamanChapter 16 Sol 2020 WKVu Khanh LeBelum ada peringkat

- ACCT 3110 CH 7 Homework E 4 8 13 19 20 27Dokumen7 halamanACCT 3110 CH 7 Homework E 4 8 13 19 20 27John Job100% (1)

- Chapter 7 - Notes - Part 1Dokumen10 halamanChapter 7 - Notes - Part 1XienaBelum ada peringkat

- 77 FDokumen3 halaman77 FJohn CalvinBelum ada peringkat

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsDari EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsBelum ada peringkat

- Using Economic Indicators to Improve Investment AnalysisDari EverandUsing Economic Indicators to Improve Investment AnalysisPenilaian: 3.5 dari 5 bintang3.5/5 (1)

- Economic Incentive SystemsDokumen23 halamanEconomic Incentive SystemsMark Arboleda GumamelaBelum ada peringkat

- Assessment of Income From House PropertyDokumen15 halamanAssessment of Income From House PropertyManish SinghBelum ada peringkat

- Microeconomics Practice TestDokumen9 halamanMicroeconomics Practice TestSonataBelum ada peringkat

- Construction Crane Busines - Plan 2019Dokumen25 halamanConstruction Crane Busines - Plan 2019Sohibul AminBelum ada peringkat

- 3M Innovation AnalysisDokumen3 halaman3M Innovation AnalysisBarunava Pal100% (1)

- Human Resource Management: Shrichand BhambhaniDokumen64 halamanHuman Resource Management: Shrichand BhambhaniNikita GuptaBelum ada peringkat

- Effect of Liquidity and Bank Size On The Profitability of Commercial Banks in BangladeshDokumen4 halamanEffect of Liquidity and Bank Size On The Profitability of Commercial Banks in BangladeshdelowerBelum ada peringkat

- S12 Retail PricingDokumen66 halamanS12 Retail PricingVishnuvardhan Ravichandran0% (1)

- Homework Week 10Dokumen13 halamanHomework Week 10LBelum ada peringkat

- PIANOKAFECOM ноты Elton John - This train dont stop there anymore PDFDokumen2 halamanPIANOKAFECOM ноты Elton John - This train dont stop there anymore PDFРавиль МаксимовBelum ada peringkat

- 23-24. Mrunal Economy Lecture 23-24 PDFDokumen29 halaman23-24. Mrunal Economy Lecture 23-24 PDFHemachandar RaviBelum ada peringkat

- 34 48 48 39 66 64 46 24 53 64 54 56 83 31 Total Result 442 268 710 38%Dokumen89 halaman34 48 48 39 66 64 46 24 53 64 54 56 83 31 Total Result 442 268 710 38%Agus MaulanaBelum ada peringkat

- Quiz 12Dokumen3 halamanQuiz 12mwende faiyuuBelum ada peringkat

- Shandong Longheng International Trade Co.,Ltd: Commercial InvoiceDokumen2 halamanShandong Longheng International Trade Co.,Ltd: Commercial InvoiceJose LahozBelum ada peringkat

- Writing Covered Calls: The Ultimate Guide ToDokumen36 halamanWriting Covered Calls: The Ultimate Guide ToRamus PerssonBelum ada peringkat

- Salvador, Gem D. Prelim Exam FM 7Dokumen3 halamanSalvador, Gem D. Prelim Exam FM 7Gem. SalvadorBelum ada peringkat

- "The New Science of Salesforce Productivity": Reading SummaryDokumen2 halaman"The New Science of Salesforce Productivity": Reading SummarypratyakshmalviBelum ada peringkat

- Monthly Digest Dec 2013Dokumen134 halamanMonthly Digest Dec 2013innvolBelum ada peringkat

- CFA Investment Foundations - Module 1 (CFA Institute) (Z-Library)Dokumen39 halamanCFA Investment Foundations - Module 1 (CFA Institute) (Z-Library)gmofneweraBelum ada peringkat

- Instrument Loan Agreement FormDokumen2 halamanInstrument Loan Agreement FormBrianBelum ada peringkat

- Identifying Causes of Construction Waste - Case of Central Region of Peninsula MalaysiaDokumen7 halamanIdentifying Causes of Construction Waste - Case of Central Region of Peninsula MalaysiaTewodros TadesseBelum ada peringkat

- KFC in Japan Case ReportDokumen11 halamanKFC in Japan Case ReportLittleDuckBaby100% (5)

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDokumen5 halamanStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceSandesh Pujari100% (1)

- Managing Small Projects PDFDokumen4 halamanManaging Small Projects PDFJ. ZhouBelum ada peringkat

- WJEC Economics AS Unit 2 QP S19Dokumen7 halamanWJEC Economics AS Unit 2 QP S19angeleschang99Belum ada peringkat

- Bài Báo Thu MuaDokumen10 halamanBài Báo Thu MuaMinh TânBelum ada peringkat

- Enterpreneurial Finance Class of MBADokumen3 halamanEnterpreneurial Finance Class of MBAFahad RabbaniBelum ada peringkat

- The Dissadvantages and Challenges of Federalizing Philippine StateDokumen3 halamanThe Dissadvantages and Challenges of Federalizing Philippine StateBenjamin III D. MirandaBelum ada peringkat

- LebronDokumen5 halamanLebronRobert oumaBelum ada peringkat

- Bidder 1 Bidder 2 Bidder 3 Technical Score Commercial Score: Bid EvaluationDokumen11 halamanBidder 1 Bidder 2 Bidder 3 Technical Score Commercial Score: Bid EvaluationAncaBelum ada peringkat