Anda mungkin juga menyukai

- ACHC"social Responsibility" Report Upstream Ayeyawady Confluence Basin Hydropower Co., LTD.Dokumen60 halamanACHC"social Responsibility" Report Upstream Ayeyawady Confluence Basin Hydropower Co., LTD.Pugh JuttaBelum ada peringkat

- Asia Foundation "National Public Perception Surveys of The Thai Electorate,"Dokumen181 halamanAsia Foundation "National Public Perception Surveys of The Thai Electorate,"Pugh JuttaBelum ada peringkat

- Davenport McKesson Corporation Agreed To Provide Lobbying Services For The The Kingdom of Thailand Inside The United States CongressDokumen4 halamanDavenport McKesson Corporation Agreed To Provide Lobbying Services For The The Kingdom of Thailand Inside The United States CongressPugh JuttaBelum ada peringkat

- Poverty, Displacement and Local Governance in South East Burma/Myanmar-ENGLISHDokumen44 halamanPoverty, Displacement and Local Governance in South East Burma/Myanmar-ENGLISHPugh JuttaBelum ada peringkat

- UNODC Record High Methamphetamine Seizures in Southeast Asia 2013Dokumen162 halamanUNODC Record High Methamphetamine Seizures in Southeast Asia 2013Anonymous S7Cq7ZDgPBelum ada peringkat

- Brief in BumeseDokumen6 halamanBrief in BumeseKo WinBelum ada peringkat

- KNU and RCSS Joint Statement-October 26-English.Dokumen2 halamanKNU and RCSS Joint Statement-October 26-English.Pugh JuttaBelum ada peringkat

- SHWE GAS REPORT :DrawingTheLine ENGLISHDokumen48 halamanSHWE GAS REPORT :DrawingTheLine ENGLISHPugh JuttaBelum ada peringkat

- The Dark Side of Transition Violence Against Muslims in MyanmarDokumen36 halamanThe Dark Side of Transition Violence Against Muslims in MyanmarPugh JuttaBelum ada peringkat

- Karen Refugee Committee Newsletter & Monthly Report, August 2013 (English, Karen, Burmese, Thai)Dokumen21 halamanKaren Refugee Committee Newsletter & Monthly Report, August 2013 (English, Karen, Burmese, Thai)Pugh JuttaBelum ada peringkat

- TBBC 2013-6-Mth-Rpt-Jan-JunDokumen130 halamanTBBC 2013-6-Mth-Rpt-Jan-JuntaisamyoneBelum ada peringkat

- State and Region Governments in Myanmar CESD TAFDokumen113 halamanState and Region Governments in Myanmar CESD TAFThet Aung LynnBelum ada peringkat

- AHRDO - Arakan Violence Report - ENGLISHDokumen178 halamanAHRDO - Arakan Violence Report - ENGLISHPugh JuttaBelum ada peringkat

- Open Letter To KNU by Daughter of SAW BA U GYI-Thelma Gyi - August 2013-ENGLISHDokumen1 halamanOpen Letter To KNU by Daughter of SAW BA U GYI-Thelma Gyi - August 2013-ENGLISHPugh JuttaBelum ada peringkat

- UNFC Info Release - EnG (7-2013)Dokumen1 halamanUNFC Info Release - EnG (7-2013)Mu Eh HserBelum ada peringkat

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (74)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- Maceda Vs ERBDokumen13 halamanMaceda Vs ERBMargrein M. GreganaBelum ada peringkat

- Income Statement - Kieso 4Dokumen34 halamanIncome Statement - Kieso 4Muhammad RezaBelum ada peringkat

- Alert Circular - DGGI GZU 324 GST 2023-24Dokumen12 halamanAlert Circular - DGGI GZU 324 GST 2023-24IAS MeenaBelum ada peringkat

- Impact of New Housing Units On Existing Rents 090120Dokumen57 halamanImpact of New Housing Units On Existing Rents 090120pkrysl2384Belum ada peringkat

- Social Issues of Pakistan and Solutions To ThemDokumen13 halamanSocial Issues of Pakistan and Solutions To Themmuhammad shoaib100% (7)

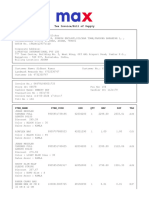

- Boat InvoiceDokumen1 halamanBoat Invoiceshiv kumarBelum ada peringkat

- Example Withholding TaxDokumen2 halamanExample Withholding TaxRaudhatun Nisa'Belum ada peringkat

- Question: How Can A Person Recover The Bank Deposits Left by The Deceased?Dokumen2 halamanQuestion: How Can A Person Recover The Bank Deposits Left by The Deceased?Cirila TatlongarawBelum ada peringkat

- 01 Interview Questions For Tax AuditorsDokumen2 halaman01 Interview Questions For Tax AuditorsTijana DoberšekBelum ada peringkat

- HWK - 6Dokumen3 halamanHWK - 6Karen Nicole Lopez0% (1)

- Labor Code Book IVDokumen17 halamanLabor Code Book IVJestoni PabiaBelum ada peringkat

- Senior Accountant Job Description and ProfileDokumen2 halamanSenior Accountant Job Description and ProfileHarendra PasiBelum ada peringkat

- Basco Vs PAGCOR DigestDokumen2 halamanBasco Vs PAGCOR DigestJoseph Dimalanta DajayBelum ada peringkat

- Ajio FN0334206010 1655992237774Dokumen1 halamanAjio FN0334206010 1655992237774Deepak RaguBelum ada peringkat

- HR Law Cases Compilation 2Dokumen86 halamanHR Law Cases Compilation 2Hilary MostajoBelum ada peringkat

- MODULE 2 Business FinanceDokumen16 halamanMODULE 2 Business FinanceWinshei CaguladaBelum ada peringkat

- Business Permits RequirementsDokumen2 halamanBusiness Permits RequirementsJurilBrokaPatiño100% (1)

- Taxation of Entertainers and Sportspersons Performing AbroadDokumen16 halamanTaxation of Entertainers and Sportspersons Performing AbroadSport Business ManagementBelum ada peringkat

- Chapter 6 - Section 2 The Baldwin Company: An Example: Year 1 Year 2 Year 3Dokumen11 halamanChapter 6 - Section 2 The Baldwin Company: An Example: Year 1 Year 2 Year 3Meghana ErapagaBelum ada peringkat

- Deductions From Gross Income Part 2 Illustrative ProblemsDokumen2 halamanDeductions From Gross Income Part 2 Illustrative ProblemsJohn Rich GamasBelum ada peringkat

- Laws Pertaining To SPEDDokumen20 halamanLaws Pertaining To SPEDginasalyv73% (22)

- SyllabusDokumen76 halamanSyllabusamattirkeyBelum ada peringkat

- WineDokumen30 halamanWinefaust642Belum ada peringkat

- Up Land LawsDokumen22 halamanUp Land LawsLakshit100% (1)

- In Voice 1788723483826306452Dokumen3 halamanIn Voice 1788723483826306452Sid KBelum ada peringkat

- 2021 HSC EconomicsDokumen24 halaman2021 HSC EconomicspotpalBelum ada peringkat

- ACA Simplified - CatalogueDokumen10 halamanACA Simplified - CatalogueZsoltNagyBelum ada peringkat

- Cambridge IGCSE: Economics 0455/12Dokumen12 halamanCambridge IGCSE: Economics 0455/12ShadyBelum ada peringkat

- Week 10B Corporate Tax RatesDokumen4 halamanWeek 10B Corporate Tax RatesCrizzalyn CruzBelum ada peringkat