Anda mungkin juga menyukai

- Acc 501 Midterm Solved MCQ SDokumen697 halamanAcc 501 Midterm Solved MCQ Sbani100% (3)

- 2011-06-07 Natixis The Eurozone-France Inflation Differential at Its Highest Level in Ten Years - Causes and OutlookDokumen3 halaman2011-06-07 Natixis The Eurozone-France Inflation Differential at Its Highest Level in Ten Years - Causes and OutlookkjlaqiBelum ada peringkat

- Hull OFOD10e MultipleChoice Questions Only Ch08Dokumen4 halamanHull OFOD10e MultipleChoice Questions Only Ch08Kevin Molly KamrathBelum ada peringkat

- Double in A Day Forex TechniqueDokumen11 halamanDouble in A Day Forex Techniqueabdulrazakyunus75% (4)

- Global - Macro - Weekly - 8 March 2019 PDFDokumen60 halamanGlobal - Macro - Weekly - 8 March 2019 PDFchaotic_pandemoniumBelum ada peringkat

- Advanced Financial Accounting 11th Edition Christensen Test BankDokumen51 halamanAdvanced Financial Accounting 11th Edition Christensen Test BankHeatherRobertstwopa100% (29)

- Import Dropped Due To Covid-19 Disruption 16 Mar 2020Dokumen3 halamanImport Dropped Due To Covid-19 Disruption 16 Mar 2020botoy26Belum ada peringkat

- Global Markets Minesweeper: F e B R U A R y 6, 2 0 1 5Dokumen4 halamanGlobal Markets Minesweeper: F e B R U A R y 6, 2 0 1 5anisdangasBelum ada peringkat

- JUL 22 DanskeDailyDokumen3 halamanJUL 22 DanskeDailyMiir ViirBelum ada peringkat

- JUL 15 DanskeDailyDokumen3 halamanJUL 15 DanskeDailyMiir ViirBelum ada peringkat

- UniCredit - Friday Notes 29.9.10Dokumen31 halamanUniCredit - Friday Notes 29.9.10jockxyzBelum ada peringkat

- Capital Daily (13th Nov 08)Dokumen3 halamanCapital Daily (13th Nov 08)babytooth2100% (1)

- Woori Daily 221110Dokumen2 halamanWoori Daily 221110Teuku Hendry AndreanBelum ada peringkat

- Economic Calendar Us LAST WEEKDokumen6 halamanEconomic Calendar Us LAST WEEKMo AlamBelum ada peringkat

- JUL 19 DanskeDailyDokumen3 halamanJUL 19 DanskeDailyMiir ViirBelum ada peringkat

- JUL 13 Danske Research DanskeDailyDokumen3 halamanJUL 13 Danske Research DanskeDailyMiir ViirBelum ada peringkat

- Morning Call - June 3 2010Dokumen7 halamanMorning Call - June 3 2010chibondkingBelum ada peringkat

- Korean Financial Markets During January 2010Dokumen8 halamanKorean Financial Markets During January 2010Republic of Korea (Korea.net)Belum ada peringkat

- PHPDPF FJGDokumen9 halamanPHPDPF FJGfred607Belum ada peringkat

- RBCCapitalMarkets RBAminutesleavespacefortaperingU-turn Aug 17 2021Dokumen11 halamanRBCCapitalMarkets RBAminutesleavespacefortaperingU-turn Aug 17 2021Dylan AdrianBelum ada peringkat

- Morning Call June 21 2010Dokumen5 halamanMorning Call June 21 2010chibondkingBelum ada peringkat

- PHP 43 L TMIDokumen5 halamanPHP 43 L TMIfred607Belum ada peringkat

- Weekly Observatory Weekly Observatory: Latin LatinDokumen7 halamanWeekly Observatory Weekly Observatory: Latin Latinogutierrez3Belum ada peringkat

- AUG 04 UOB Global MarketsDokumen3 halamanAUG 04 UOB Global MarketsMiir ViirBelum ada peringkat

- Phpurt QKNDokumen7 halamanPhpurt QKNfred607Belum ada peringkat

- AUG 10 UOB Global MarketsDokumen3 halamanAUG 10 UOB Global MarketsMiir ViirBelum ada peringkat

- Danske Daily: Key NewsDokumen4 halamanDanske Daily: Key NewsMiir ViirBelum ada peringkat

- Economic CalendarDokumen12 halamanEconomic CalendarMaria januario TembeBelum ada peringkat

- 29 Juni 2023Dokumen4 halaman29 Juni 2023cahyono79Belum ada peringkat

- Phpiei KS0Dokumen5 halamanPhpiei KS0fred607Belum ada peringkat

- PHP GF QM2 KDokumen9 halamanPHP GF QM2 Kfred607Belum ada peringkat

- 2023 03 24 Weekly Economic ReleaseDokumen13 halaman2023 03 24 Weekly Economic ReleaseStephen EddlestonBelum ada peringkat

- PHP 3 LR M5 KDokumen7 halamanPHP 3 LR M5 Kfred607Belum ada peringkat

- Westpack JUN 16 Mornng ReportDokumen1 halamanWestpack JUN 16 Mornng ReportMiir ViirBelum ada peringkat

- ING FX TalkingDokumen20 halamanING FX TalkingCiocoiu Vlad AndreiBelum ada peringkat

- AUG 08 DanskeDailyDokumen4 halamanAUG 08 DanskeDailyMiir ViirBelum ada peringkat

- Economic CalendarDokumen6 halamanEconomic CalendarAtulBelum ada peringkat

- ABL Funds Manager Report - Conventional - August 2022Dokumen14 halamanABL Funds Manager Report - Conventional - August 2022Aniqa AsgharBelum ada peringkat

- Calendar of Releases: FinancialdataDokumen24 halamanCalendar of Releases: Financialdatarryan123123Belum ada peringkat

- ABL - FMR - JULY'23 ConventionalDokumen14 halamanABL - FMR - JULY'23 ConventionalAniqa AsgharBelum ada peringkat

- Monitor Markets 20230908Dokumen2 halamanMonitor Markets 20230908Kicki AnderssonBelum ada peringkat

- Commodity Eye Catchers of The Week: Buy MCX Copper (Feb) Around 443 SL 438 TGT 453Dokumen4 halamanCommodity Eye Catchers of The Week: Buy MCX Copper (Feb) Around 443 SL 438 TGT 453Padma SriBelum ada peringkat

- PHPV ZAQKbDokumen9 halamanPHPV ZAQKbfred607Belum ada peringkat

- Ashika Morning Report - 6.06.11Dokumen7 halamanAshika Morning Report - 6.06.11ratishblue7650Belum ada peringkat

- Stevo's Market Update 7-30-2010Dokumen10 halamanStevo's Market Update 7-30-2010HedgedInBelum ada peringkat

- US Fed Between A Stock and A Bond Place 100810Dokumen4 halamanUS Fed Between A Stock and A Bond Place 100810tuyetnt20016337Belum ada peringkat

- PHPW J2 FKQDokumen5 halamanPHPW J2 FKQfred607Belum ada peringkat

- Dow 12,288.17 +61.53 +0.50% S&P 500 1,336.32 +8.31 +0.63% Nasdaq 2,825.56 +21.21 +0.76%Dokumen6 halamanDow 12,288.17 +61.53 +0.50% S&P 500 1,336.32 +8.31 +0.63% Nasdaq 2,825.56 +21.21 +0.76%Andre_Setiawan_1986Belum ada peringkat

- Second Quarterly ReportDokumen67 halamanSecond Quarterly ReportsultanabidBelum ada peringkat

- JUL 23 DanskeDailyDokumen3 halamanJUL 23 DanskeDailyMiir ViirBelum ada peringkat

- ICICI PrudentialDokumen6 halamanICICI PrudentialMoumita DasBelum ada peringkat

- Market Commentary 3/6Dokumen10 halamanMarket Commentary 3/6pdoorBelum ada peringkat

- Daily Treasury Report0405-EnGDokumen3 halamanDaily Treasury Report0405-EnGBiliguudei AmarsaikhanBelum ada peringkat

- DailyNewsLetter - 20 Oct 10Dokumen3 halamanDailyNewsLetter - 20 Oct 10checrucifixBelum ada peringkat

- EGB Bond Analysis 20032023Dokumen7 halamanEGB Bond Analysis 20032023asdf23Belum ada peringkat

- AUG 11 UOB Global MarketsDokumen3 halamanAUG 11 UOB Global MarketsMiir ViirBelum ada peringkat

- Phpi 2 KB 84Dokumen5 halamanPhpi 2 KB 84fred607Belum ada peringkat

- 2011-05-04 Unicredit Euro Compass - How Long Before The Next Cyclical DownturnDokumen40 halaman2011-05-04 Unicredit Euro Compass - How Long Before The Next Cyclical DownturnkjlaqiBelum ada peringkat

- Daily Treasury Report0320 ENGDokumen3 halamanDaily Treasury Report0320 ENGBiliguudei AmarsaikhanBelum ada peringkat

- PHP Ilt KW KDokumen5 halamanPHP Ilt KW Kfred607Belum ada peringkat

- Surge in Chinese Imports: Morning ReportDokumen3 halamanSurge in Chinese Imports: Morning Reportnaudaslietas_lvBelum ada peringkat

- PHPG KWZAYDokumen5 halamanPHPG KWZAYfred607Belum ada peringkat

- Market Overview Weekly Analysis With Fundamental and Technical Outlook Important Events of The WeekDokumen6 halamanMarket Overview Weekly Analysis With Fundamental and Technical Outlook Important Events of The WeekshivaBelum ada peringkat

- Useianalysis 20101211114753Dokumen5 halamanUseianalysis 20101211114753Gautham KoderiBelum ada peringkat

- Japan's Financial Crisis: Institutional Rigidity and Reluctant ChangeDari EverandJapan's Financial Crisis: Institutional Rigidity and Reluctant ChangeBelum ada peringkat

- 2011-06-17 LLOY Data Analysis - Greek TragedyDokumen4 halaman2011-06-17 LLOY Data Analysis - Greek TragedykjlaqiBelum ada peringkat

- 2011-07-12 LLOY European Risk - Oversold and Ready To Recover For Medium-TermDokumen9 halaman2011-07-12 LLOY European Risk - Oversold and Ready To Recover For Medium-TermkjlaqiBelum ada peringkat

- 2011-06-15 AXA IM Weekly Comment Japan - V-Shaped Rebound ConfirmedDokumen3 halaman2011-06-15 AXA IM Weekly Comment Japan - V-Shaped Rebound ConfirmedkjlaqiBelum ada peringkat

- 2011-06-28 Natixis Do Germans Work More Than Southern Europeans - No, They Work Much Less, and Not More IntenselyDokumen10 halaman2011-06-28 Natixis Do Germans Work More Than Southern Europeans - No, They Work Much Less, and Not More IntenselykjlaqiBelum ada peringkat

- 2011-06-17 Erste Financial Focus WeeklyDokumen14 halaman2011-06-17 Erste Financial Focus WeeklykjlaqiBelum ada peringkat

- 2011-06-27 HSBC FX Edge - EURUSD in The Bigger PictureDokumen4 halaman2011-06-27 HSBC FX Edge - EURUSD in The Bigger PicturekjlaqiBelum ada peringkat

- 2011-06-09 Scotia FX DailyDokumen3 halaman2011-06-09 Scotia FX DailykjlaqiBelum ada peringkat

- 2011-06-10 LLOY UK Consumer Discretionary Sector AnalysisDokumen3 halaman2011-06-10 LLOY UK Consumer Discretionary Sector AnalysiskjlaqiBelum ada peringkat

- 2011-06-16 Natixis Tunisia - What's Next After The Jasmine RevolutionDokumen11 halaman2011-06-16 Natixis Tunisia - What's Next After The Jasmine RevolutionkjlaqiBelum ada peringkat

- 2011-06-10 DBS Daily Breakfast SpreadDokumen8 halaman2011-06-10 DBS Daily Breakfast SpreadkjlaqiBelum ada peringkat

- 2011-06-10 UOB Asian MarketsDokumen2 halaman2011-06-10 UOB Asian MarketskjlaqiBelum ada peringkat

- 2011-06-06 Danske Flash Comm - Greece Is Likely To Get A Second Rescue Package SoonDokumen5 halaman2011-06-06 Danske Flash Comm - Greece Is Likely To Get A Second Rescue Package SoonkjlaqiBelum ada peringkat

- 2011-06-15 UOB Asian MarketsDokumen3 halaman2011-06-15 UOB Asian MarketskjlaqiBelum ada peringkat

- 2011-06-09 UniCredit - ECB Ready To HikeDokumen4 halaman2011-06-09 UniCredit - ECB Ready To HikekjlaqiBelum ada peringkat

- 2011-06-07 DBS Daily Breakfast SpreadDokumen8 halaman2011-06-07 DBS Daily Breakfast SpreadkjlaqiBelum ada peringkat

- 2011-06-08 DBS Daily Breakfast SpreadDokumen6 halaman2011-06-08 DBS Daily Breakfast SpreadkjlaqiBelum ada peringkat

- 2011-06-07 RMB Daily FXDokumen7 halaman2011-06-07 RMB Daily FXkjlaqiBelum ada peringkat

- 2011-06-07 Scotia Asian FX UpdateDokumen3 halaman2011-06-07 Scotia Asian FX UpdatekjlaqiBelum ada peringkat

- 2011-06-07 Forsyth Barr NZ Corporate Credit WeeklyDokumen8 halaman2011-06-07 Forsyth Barr NZ Corporate Credit WeeklykjlaqiBelum ada peringkat

- 2011-06-06 DBS Daily Breakfast SpreadDokumen9 halaman2011-06-06 DBS Daily Breakfast SpreadkjlaqiBelum ada peringkat

- Euro Area Housing Markets: A Temperature GaugeDokumen8 halamanEuro Area Housing Markets: A Temperature GaugekjlaqiBelum ada peringkat

- 2011-06-07 CommBank RBA Board Meeting - Rates UnchangedDokumen4 halaman2011-06-07 CommBank RBA Board Meeting - Rates UnchangedkjlaqiBelum ada peringkat

- 2011-06-07 Mitsubishi UFJ Britains Lessons in Monetary Failure - Devaluation and QE Procude Starkly Negative ResultsDokumen3 halaman2011-06-07 Mitsubishi UFJ Britains Lessons in Monetary Failure - Devaluation and QE Procude Starkly Negative ResultskjlaqiBelum ada peringkat

- 2011-06-03 LYOD UK Industrial Production Expected To Drop SharplyDokumen4 halaman2011-06-03 LYOD UK Industrial Production Expected To Drop SharplykjlaqiBelum ada peringkat

- 2011-06-03 Erste CEE FI & FX InsightsDokumen16 halaman2011-06-03 Erste CEE FI & FX InsightskjlaqiBelum ada peringkat

- United States: Real and Nominal Consumer SpendingDokumen8 halamanUnited States: Real and Nominal Consumer SpendingkjlaqiBelum ada peringkat

- 2011 Robeco Emergence of A Global Middle Class - Impact On CommoditiesDokumen7 halaman2011 Robeco Emergence of A Global Middle Class - Impact On CommoditieskjlaqiBelum ada peringkat

- 2011-06-03 Danske Flash US - Nonfarm Payroll Weak, But Probably Too WeakDokumen5 halaman2011-06-03 Danske Flash US - Nonfarm Payroll Weak, But Probably Too WeakkjlaqiBelum ada peringkat

- SDL NSDLDokumen2 halamanSDL NSDLNeha KrishnaniBelum ada peringkat

- Chapter 9-STOCK VALUATION-FIXDokumen33 halamanChapter 9-STOCK VALUATION-FIXRacing FirmanBelum ada peringkat

- Sensex Rolling ReturnsDokumen1 halamanSensex Rolling Returnsmaheshtech76Belum ada peringkat

- Debt Structure Interest Term Corporate Paper Capital Fixed Loan Legal Bank Supply Function Nbqbs PAY Crime CurrencyDokumen20 halamanDebt Structure Interest Term Corporate Paper Capital Fixed Loan Legal Bank Supply Function Nbqbs PAY Crime CurrencyMa. Kristine Laurice AmancioBelum ada peringkat

- Consolidated FDI Policy, 2017Dokumen113 halamanConsolidated FDI Policy, 2017Latest Laws TeamBelum ada peringkat

- MARS Portfolio Performance 31 MarchDokumen3 halamanMARS Portfolio Performance 31 MarchMukesh KumarBelum ada peringkat

- Fin358 Individual Assignment Nur Hazani 2020818012Dokumen12 halamanFin358 Individual Assignment Nur Hazani 2020818012nur hazaniBelum ada peringkat

- Portfolio Optimization Maximizing Returns and Reducing RiskDokumen8 halamanPortfolio Optimization Maximizing Returns and Reducing Riskpramodkumar808751528270Belum ada peringkat

- Project PPT in Mutual Fund SipDokumen13 halamanProject PPT in Mutual Fund SipNARASIMHA REDDYBelum ada peringkat

- 6 Pas 23 28 PDFDokumen1 halaman6 Pas 23 28 PDFcherry blossomBelum ada peringkat

- Morrissette ProfileAngelInvestors 2007Dokumen16 halamanMorrissette ProfileAngelInvestors 2007pattitil.ppBelum ada peringkat

- Capital Market in India ProjectDokumen26 halamanCapital Market in India ProjectNamrataShahaniBelum ada peringkat

- United States District Court Central District of California: 8:21-Cv-00403-Jvs-AdsxDokumen114 halamanUnited States District Court Central District of California: 8:21-Cv-00403-Jvs-Adsxtriguy_2010Belum ada peringkat

- Lecture Notes Topic 6 Student PDFDokumen94 halamanLecture Notes Topic 6 Student PDFAnDy YiMBelum ada peringkat

- Quiz 1 - Understanding Investments and Investment Alternatives - Attempt ReviewDokumen6 halamanQuiz 1 - Understanding Investments and Investment Alternatives - Attempt ReviewDivya chandBelum ada peringkat

- Annual Report Aces 2020Dokumen161 halamanAnnual Report Aces 2020Dua TigaBelum ada peringkat

- Statement of CashflowDokumen2 halamanStatement of CashflowAna Marie IllutBelum ada peringkat

- Cbip Q&aDokumen4 halamanCbip Q&aZerohedgeBelum ada peringkat

- Sec Form Auf-002-R: Securities and Exchange CommissionDokumen3 halamanSec Form Auf-002-R: Securities and Exchange CommissionRodolfo KhiaBelum ada peringkat

- Amanah Saham Nasional: January 2023Dokumen1 halamanAmanah Saham Nasional: January 2023Afif ApihBelum ada peringkat

- The Investing Secrets Of: ISA MillionairesDokumen6 halamanThe Investing Secrets Of: ISA MillionairesRamBelum ada peringkat

- Review Questions - CH 3Dokumen2 halamanReview Questions - CH 3bigbadbear30% (2)

- ChemaliteDokumen8 halamanChemaliteamitinfo_mishraBelum ada peringkat

- Advertising: Academic Year 2022-2023 Elective Courses (EC) Group B. Marketing ElectivesDokumen119 halamanAdvertising: Academic Year 2022-2023 Elective Courses (EC) Group B. Marketing ElectivesMilan JainBelum ada peringkat

- Chapter 7 - Portfolio Theory and The Capital Asset Model Pricing (Compatibility Mode)Dokumen21 halamanChapter 7 - Portfolio Theory and The Capital Asset Model Pricing (Compatibility Mode)Hanh TranBelum ada peringkat

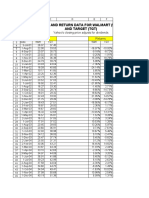

- Price and Return Data For Walmart (WMT) and Target (TGT) : Prices Returns Yahoo's Closing Price Adjusts For DividendsDokumen19 halamanPrice and Return Data For Walmart (WMT) and Target (TGT) : Prices Returns Yahoo's Closing Price Adjusts For DividendsSyed Ameer Ali ShahBelum ada peringkat