Anda mungkin juga menyukai

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (74)

- Evestment Investment Statistics A Reference Guide September 2012 PDFDokumen72 halamanEvestment Investment Statistics A Reference Guide September 2012 PDFDeepak KukretyBelum ada peringkat

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- Singular Spectrum Analysis Demo With VBADokumen12 halamanSingular Spectrum Analysis Demo With VBAPeter UrbaniBelum ada peringkat

- Ishares Portfolio Analytics Coskew and CoKurt VBA3Dokumen178 halamanIshares Portfolio Analytics Coskew and CoKurt VBA3Peter Urbani100% (1)

- Opalesque New Managers May 2012Dokumen51 halamanOpalesque New Managers May 2012Peter Urbani0% (1)

- Opalesque New Managers May 2012Dokumen51 halamanOpalesque New Managers May 2012Peter Urbani0% (1)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- EVestment Reference GuideDokumen83 halamanEVestment Reference GuideEthanBelum ada peringkat

- IMNU HimasnhuPatel Anand Rathi Internship ReportDokumen57 halamanIMNU HimasnhuPatel Anand Rathi Internship ReportHimanshu Patel33% (3)

- September 2008 Caia Level I Sample Questions: Chartered Alternative Investment AnalystDokumen27 halamanSeptember 2008 Caia Level I Sample Questions: Chartered Alternative Investment AnalystRavi Gupta100% (1)

- Do You Have To Be Abnormal To Beat The MarketDokumen3 halamanDo You Have To Be Abnormal To Beat The MarketPeter UrbaniBelum ada peringkat

- Cholesky Versus SVDDokumen4 halamanCholesky Versus SVDPeter UrbaniBelum ada peringkat

- Random Forest in Excel and VBADokumen24 halamanRandom Forest in Excel and VBAPeter UrbaniBelum ada peringkat

- Partial Correlation Network Graph VBA (DJINDI)Dokumen463 halamanPartial Correlation Network Graph VBA (DJINDI)Peter UrbaniBelum ada peringkat

- Intra-Horizon VaR and Expected Shortfall Spreadsheet With VBADokumen7 halamanIntra-Horizon VaR and Expected Shortfall Spreadsheet With VBAPeter Urbani0% (1)

- How Well Does Your Hedge Fund HedgeDokumen2 halamanHow Well Does Your Hedge Fund HedgePeter UrbaniBelum ada peringkat

- Opalesque NewManagers July 2012Dokumen45 halamanOpalesque NewManagers July 2012Peter UrbaniBelum ada peringkat

- Risk Perspectives: What Is Risk? Its Measurement, Dimensions, Modeling (Asset Classes, Risk Factors and Regimes)Dokumen11 halamanRisk Perspectives: What Is Risk? Its Measurement, Dimensions, Modeling (Asset Classes, Risk Factors and Regimes)Peter UrbaniBelum ada peringkat

- Opalesque New Managers March 2012Dokumen37 halamanOpalesque New Managers March 2012Peter UrbaniBelum ada peringkat

- Why Distributions Matter (16 Jan 2012)Dokumen43 halamanWhy Distributions Matter (16 Jan 2012)Peter UrbaniBelum ada peringkat

- TLS Orthogonal Regression VBADokumen16 halamanTLS Orthogonal Regression VBAPeter Urbani0% (1)

- Liqudity VaR With Correct Time Scaling of Higher MomentsDokumen113 halamanLiqudity VaR With Correct Time Scaling of Higher MomentsPeter UrbaniBelum ada peringkat

- Four Moment Risk Decomposition No VBADokumen13 halamanFour Moment Risk Decomposition No VBAPeter UrbaniBelum ada peringkat

- Incremental and Marginal VaR Plus Infiniti 4 Moment Version No VBADokumen14 halamanIncremental and Marginal VaR Plus Infiniti 4 Moment Version No VBAPeter UrbaniBelum ada peringkat

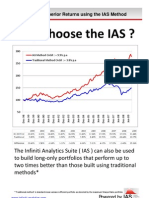

- Why Choose The IASDokumen6 halamanWhy Choose The IASPeter UrbaniBelum ada peringkat

- Infiniti Capital Four Moment Risk DecompositionDokumen19 halamanInfiniti Capital Four Moment Risk DecompositionPeter UrbaniBelum ada peringkat

- Calculate Portfolio Sharpe RatioDokumen7 halamanCalculate Portfolio Sharpe RatioazamopulentBelum ada peringkat

- ETF Portfolio Details - Saxo Bank - Balanced Portfolio Description 2013Dokumen8 halamanETF Portfolio Details - Saxo Bank - Balanced Portfolio Description 2013Bruno Dias da CostaBelum ada peringkat

- Financial Ratios CFP On ExcelDokumen20 halamanFinancial Ratios CFP On ExcelAkash JadhavBelum ada peringkat

- Risks: Mean-Variance Optimization Is A Good Choice, But For Other Reasons Than You Might ThinkDokumen16 halamanRisks: Mean-Variance Optimization Is A Good Choice, But For Other Reasons Than You Might ThinkThảo Như Trần NgọcBelum ada peringkat

- Data AnanysisDokumen14 halamanData AnanysisDrishty BishtBelum ada peringkat

- Task 20 - HedgeDokumen4 halamanTask 20 - HedgeZea ZakeBelum ada peringkat

- Introduction To Alternative Investments: Weekly Test - AIDokumen96 halamanIntroduction To Alternative Investments: Weekly Test - AIRuchira GoleBelum ada peringkat

- Sortino - A Better Measure of Risk? ROLLINGER Feb 2013Dokumen3 halamanSortino - A Better Measure of Risk? ROLLINGER Feb 2013Interconti Ltd.Belum ada peringkat

- Mock Exam A - AMDokumen6 halamanMock Exam A - AMGlenn NgBelum ada peringkat

- Investor Letter: The Seventh Month in A RowDokumen5 halamanInvestor Letter: The Seventh Month in A RowAgustin VeraBelum ada peringkat

- 35 Quantitative Value FinalDokumen11 halaman35 Quantitative Value FinalMiha4Belum ada peringkat

- Bostwick Capital LLC Bostwick Compound LPDokumen1 halamanBostwick Capital LLC Bostwick Compound LPbessiebuBelum ada peringkat

- Mutual Fund AnalysisDokumen6 halamanMutual Fund AnalysisAnooja SajeevBelum ada peringkat

- Sharma2015 PDFDokumen20 halamanSharma2015 PDFCitra MurtiBelum ada peringkat

- Nqir To Jun 2018Dokumen11 halamanNqir To Jun 2018pBelum ada peringkat

- An Introduction To Alternative InvestmentsDokumen20 halamanAn Introduction To Alternative InvestmentshbobadillapBelum ada peringkat

- RR Sortino A Sharper RatioDokumen6 halamanRR Sortino A Sharper Ratiokostistriant30Belum ada peringkat

- 2010 - On The Consistency of Performance Measures For Hedge FundsDokumen16 halaman2010 - On The Consistency of Performance Measures For Hedge FundsCarlosBelum ada peringkat

- An Analysis of Index Option Writing For Liquid Enhanced Risk-Adjusted ReturnsDokumen6 halamanAn Analysis of Index Option Writing For Liquid Enhanced Risk-Adjusted ReturnsJoe DBelum ada peringkat

- Portfolio Analysis ToolsDokumen6 halamanPortfolio Analysis Toolsrupesh_kanabar1604100% (5)

- Option SupertraderDokumen10 halamanOption SupertraderJunedi dBelum ada peringkat

- Sortino A Sharper Ratio PDFDokumen6 halamanSortino A Sharper Ratio PDFJonathan RengifoBelum ada peringkat

- Mutual Funds ShivnadarDokumen126 halamanMutual Funds ShivnadarKritika KoulBelum ada peringkat

- Wiesinger 2010 BA Risk Adjusted Performance Measurement State of The ArtDokumen56 halamanWiesinger 2010 BA Risk Adjusted Performance Measurement State of The Artabhishek210585Belum ada peringkat

- R26 CFA Level 3Dokumen12 halamanR26 CFA Level 3Ashna0188Belum ada peringkat