Anda mungkin juga menyukai

- A Digitally Controlled Low Voltage Variable Gain Amplifier With Constant Return LossDokumen7 halamanA Digitally Controlled Low Voltage Variable Gain Amplifier With Constant Return LossCyberJournals MultidisciplinaryBelum ada peringkat

- Prototype of 5.8 GHZ Wireless Power Transmission System For Electric Vehicle SystemDokumen5 halamanPrototype of 5.8 GHZ Wireless Power Transmission System For Electric Vehicle SystemCyberJournals MultidisciplinaryBelum ada peringkat

- Nonlinear Model Identification For Inverter of AMB-Flywheel SystemDokumen6 halamanNonlinear Model Identification For Inverter of AMB-Flywheel SystemCyberJournals MultidisciplinaryBelum ada peringkat

- Computing The Configuration Space On Reconfiguration Mesh MultiprocessorsDokumen8 halamanComputing The Configuration Space On Reconfiguration Mesh MultiprocessorsCyberJournals MultidisciplinaryBelum ada peringkat

- Simulations For Time Delay Compensation in Networked Control SystemsDokumen7 halamanSimulations For Time Delay Compensation in Networked Control SystemsCyberJournals MultidisciplinaryBelum ada peringkat

- Relaying Schemes For Improving Coverage and Capacity in Cellular System With Selectable User EquipmentDokumen8 halamanRelaying Schemes For Improving Coverage and Capacity in Cellular System With Selectable User EquipmentCyberJournals MultidisciplinaryBelum ada peringkat

- Fast Block Direction Prediction For Directional TransformsDokumen8 halamanFast Block Direction Prediction For Directional TransformsCyberJournals MultidisciplinaryBelum ada peringkat

- Inspection of The Interior Surface of A Cylindrical Pipe by Omnidirectional Image Acquisition SystemDokumen6 halamanInspection of The Interior Surface of A Cylindrical Pipe by Omnidirectional Image Acquisition SystemCyberJournals MultidisciplinaryBelum ada peringkat

- Exploration of Co-Relation Between Depression and Anaemia in Pregnant Women Using Knowledge Discovery and Data Mining Algorithms and ToolsDokumen9 halamanExploration of Co-Relation Between Depression and Anaemia in Pregnant Women Using Knowledge Discovery and Data Mining Algorithms and ToolsCyberJournals MultidisciplinaryBelum ada peringkat

- A Local WBC System Operating Across A University CampusDokumen7 halamanA Local WBC System Operating Across A University CampusCyberJournals MultidisciplinaryBelum ada peringkat

- Artemisa: Using An Android Device As An Eco-Driving AssistantDokumen8 halamanArtemisa: Using An Android Device As An Eco-Driving AssistantCyberJournals MultidisciplinaryBelum ada peringkat

- Nuclear Power-An Inevitable Option For Most Vulnerable Countries From The Perspective of Environmental DegradationDokumen6 halamanNuclear Power-An Inevitable Option For Most Vulnerable Countries From The Perspective of Environmental DegradationCyberJournals MultidisciplinaryBelum ada peringkat

- An Improved Shock Graph For An Improved Object RecognitionDokumen8 halamanAn Improved Shock Graph For An Improved Object RecognitionCyberJournals MultidisciplinaryBelum ada peringkat

- A Scheme To Monitor Maximum Link Load With Load RankingDokumen7 halamanA Scheme To Monitor Maximum Link Load With Load RankingCyberJournals MultidisciplinaryBelum ada peringkat

- Performance of Hybrid Pump-Wavelength Configurations For Optical Packet Switch With Parametric Wavelength ConvertersDokumen8 halamanPerformance of Hybrid Pump-Wavelength Configurations For Optical Packet Switch With Parametric Wavelength ConvertersCyberJournals MultidisciplinaryBelum ada peringkat

- Performance Estimation of Novel 32-Bit and 64-Bit RISC Based Network Processor CoresDokumen13 halamanPerformance Estimation of Novel 32-Bit and 64-Bit RISC Based Network Processor CoresCyberJournals MultidisciplinaryBelum ada peringkat

- Modified Log Domain Decoding Algorithm For LDPC Codes Over GF (Q)Dokumen7 halamanModified Log Domain Decoding Algorithm For LDPC Codes Over GF (Q)CyberJournals MultidisciplinaryBelum ada peringkat

- A Novel Adaptive Resource Allocation Scheme With QoS Support in Mobile WiMAX Release 2 Wireless NetworksDokumen8 halamanA Novel Adaptive Resource Allocation Scheme With QoS Support in Mobile WiMAX Release 2 Wireless NetworksCyberJournals MultidisciplinaryBelum ada peringkat

- Relay Network Extension On Wireless Access Links (ReNEWAL) of High Rate Packet Data (HRPD)Dokumen11 halamanRelay Network Extension On Wireless Access Links (ReNEWAL) of High Rate Packet Data (HRPD)CyberJournals MultidisciplinaryBelum ada peringkat

- An Overview of Technical and Economical Feasibility of Retrofitted MHD Power Plants From The Perspective of BangladeshDokumen5 halamanAn Overview of Technical and Economical Feasibility of Retrofitted MHD Power Plants From The Perspective of BangladeshCyberJournals MultidisciplinaryBelum ada peringkat

- An Efficient MODEL For Detecting LEARNING STYLE Preferences in A Personalized E-Learning Management SystemDokumen8 halamanAn Efficient MODEL For Detecting LEARNING STYLE Preferences in A Personalized E-Learning Management SystemCyberJournals MultidisciplinaryBelum ada peringkat

- A Hybrid Scheme With Impressive QoS Over Telecommunication NetworksDokumen7 halamanA Hybrid Scheme With Impressive QoS Over Telecommunication NetworksCyberJournals MultidisciplinaryBelum ada peringkat

- Throughput Performance Enhancement For MUDiv/OFDMA Using MMSE Equalization Without Guard IntervalDokumen7 halamanThroughput Performance Enhancement For MUDiv/OFDMA Using MMSE Equalization Without Guard IntervalCyberJournals MultidisciplinaryBelum ada peringkat

- Performance Evaluation of Stochastic Algorithms For Linear Antenna Arrays Synthesis Under Constrained ConditionsDokumen7 halamanPerformance Evaluation of Stochastic Algorithms For Linear Antenna Arrays Synthesis Under Constrained ConditionsCyberJournals MultidisciplinaryBelum ada peringkat

- Simulations For WDM Mesh Networks With Visual BasicDokumen7 halamanSimulations For WDM Mesh Networks With Visual BasicCyberJournals MultidisciplinaryBelum ada peringkat

- On-Demand Multicast Slot Allocation Scheme For Active Optical Access Network Using PLZT High-Speed Optical SwitchesDokumen9 halamanOn-Demand Multicast Slot Allocation Scheme For Active Optical Access Network Using PLZT High-Speed Optical SwitchesCyberJournals MultidisciplinaryBelum ada peringkat

- Investigation On The Performance of Linear Antenna Array Synthesis Using Genetic AlgorithmDokumen7 halamanInvestigation On The Performance of Linear Antenna Array Synthesis Using Genetic AlgorithmCyberJournals MultidisciplinaryBelum ada peringkat

- Cycle Analysis in Expanded QC LDPC CodesDokumen6 halamanCycle Analysis in Expanded QC LDPC CodesCyberJournals MultidisciplinaryBelum ada peringkat

- A Feature Extraction Method and Recognition Algorithm For Detection Unknown Worm and Variations Based On Static FeaturesDokumen7 halamanA Feature Extraction Method and Recognition Algorithm For Detection Unknown Worm and Variations Based On Static FeaturesCyberJournals MultidisciplinaryBelum ada peringkat

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5783)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (72)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (119)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- Evaluating The Performance of Private Financing and Traditional ProcurementDokumen21 halamanEvaluating The Performance of Private Financing and Traditional ProcurementBruce DoyaoenBelum ada peringkat

- CicDokumen25 halamanCicjunjie buliganBelum ada peringkat

- Roles Available in Microsoft Dynamics Great Plains 10.0Dokumen67 halamanRoles Available in Microsoft Dynamics Great Plains 10.0Gopal RenganathanBelum ada peringkat

- PayPal Transaction History Feb-Mar 2015Dokumen1 halamanPayPal Transaction History Feb-Mar 2015dnbinhBelum ada peringkat

- Role of MICRO Finance in Financial InclusionDokumen16 halamanRole of MICRO Finance in Financial InclusionBharath Pavanje75% (4)

- MSU-IIT Cooperative ArticlesDokumen5 halamanMSU-IIT Cooperative ArticlesMariver LlorenteBelum ada peringkat

- BSP Circular No 580 77 PDFDokumen5 halamanBSP Circular No 580 77 PDFneil peirceBelum ada peringkat

- Financial AccountingDokumen10 halamanFinancial AccountingNumber ButBelum ada peringkat

- DPA5053 Company Law: Prepared byDokumen12 halamanDPA5053 Company Law: Prepared byPavitra MohanBelum ada peringkat

- ( (Most of The Discussion Is About Default, Will Not Include in The Digest Na) )Dokumen8 halaman( (Most of The Discussion Is About Default, Will Not Include in The Digest Na) )Mark Evan GarciaBelum ada peringkat

- Bank Mandiri's Commitment to Sustainable DevelopmentDokumen254 halamanBank Mandiri's Commitment to Sustainable Developmentlucky.amirullahBelum ada peringkat

- Bank RobberyDokumen4 halamanBank RobberyJanet Tal-udanBelum ada peringkat

- Boynton SM CH 17Dokumen34 halamanBoynton SM CH 17jeankopler100% (1)

- ListDokumen6 halamanListRoshelleBelum ada peringkat

- Strategic Paper Chap 1 7Dokumen40 halamanStrategic Paper Chap 1 7Lauren RefugioBelum ada peringkat

- Project Report On Health Law: Limitations On Liabilities and MediclaimDokumen17 halamanProject Report On Health Law: Limitations On Liabilities and MediclaimDeepesh SinghBelum ada peringkat

- 5-Year Projected Income Statement: Arnel's CanteenDokumen5 halaman5-Year Projected Income Statement: Arnel's CanteenKathleen Queen BermudoBelum ada peringkat

- Banking NotesDokumen4 halamanBanking Notesshanti priyaBelum ada peringkat

- UBL Internship ReportDokumen124 halamanUBL Internship ReportTaha MadniBelum ada peringkat

- Amazon Settlement ReportDokumen77 halamanAmazon Settlement ReportHarsh PatelBelum ada peringkat

- Unsupervised Outlier Detection Improves Financial Statement AuditsDokumen86 halamanUnsupervised Outlier Detection Improves Financial Statement AuditsJorge Raphael Rodriguez MamaniBelum ada peringkat

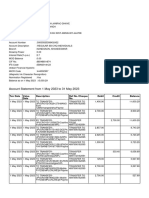

- Account Statement From 1 May 2023 To 31 May 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDokumen10 halamanAccount Statement From 1 May 2023 To 31 May 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit Balanceavinashdeshmukh7027Belum ada peringkat

- GmailDokumen4 halamanGmailmoBelum ada peringkat

- San Fernando Rural Bank, Inc. V. Pampanga Omnibus Development Corporation and Dominic G. Aquino FactsDokumen2 halamanSan Fernando Rural Bank, Inc. V. Pampanga Omnibus Development Corporation and Dominic G. Aquino FactsRamon Khalil Erum IVBelum ada peringkat

- Evaluating Consumer Loans - 3rd Unit NotesDokumen18 halamanEvaluating Consumer Loans - 3rd Unit NotesDr VIRUPAKSHA GOUD GBelum ada peringkat

- Lotto Payment Release Order Form 1Dokumen1 halamanLotto Payment Release Order Form 1baloo020379100% (2)

- DigiPay v1Dokumen18 halamanDigiPay v1KAVEEN PRASANNAMOORTHYBelum ada peringkat

- Profit Loss Statement TemplateDokumen1 halamanProfit Loss Statement TemplategfcbcBelum ada peringkat

- Special power attorney documentDokumen3 halamanSpecial power attorney documentJessa Damian100% (1)

- Apply for UNILAG Transcripts and RecordsDokumen7 halamanApply for UNILAG Transcripts and RecordsUdoh Mopolo-Ultra Emmanuel100% (1)