Anda mungkin juga menyukai

- HARP 2.0 Freddie Open Access Relief UnlimitedDokumen4 halamanHARP 2.0 Freddie Open Access Relief UnlimitedAccessLendingBelum ada peringkat

- Important Bulletin Regarding Termite Reports On FHA LoansDokumen3 halamanImportant Bulletin Regarding Termite Reports On FHA LoansAccessLendingBelum ada peringkat

- USDA Edge Fixed ProductDokumen7 halamanUSDA Edge Fixed ProductAccessLendingBelum ada peringkat

- Elite HARP Open Access ReliefDokumen4 halamanElite HARP Open Access ReliefAccessLendingBelum ada peringkat

- Bankruptcy, Foreclosure, Pre-Foreclosure, and Shorts Sales GuideDokumen2 halamanBankruptcy, Foreclosure, Pre-Foreclosure, and Shorts Sales GuideAccessLendingBelum ada peringkat

- The 3 8% TaxDokumen11 halamanThe 3 8% Taxsanwest60Belum ada peringkat

- HUD Announcement: Single Family Mortgage Insurance: Annual and Up-Front Mortgage Insurance Premium - ChangesDokumen5 halamanHUD Announcement: Single Family Mortgage Insurance: Annual and Up-Front Mortgage Insurance Premium - ChangesAccessLendingBelum ada peringkat

- CAPITAL MARKETS Fannie and Freddie Pricing ChangesDokumen1 halamanCAPITAL MARKETS Fannie and Freddie Pricing ChangesAccessLendingBelum ada peringkat

- 2012 VA County Loan LimitsDokumen4 halaman2012 VA County Loan LimitsAccessLendingBelum ada peringkat

- Fannie Mae Desktop Originator/Underwriter Release Notes UpdateDokumen3 halamanFannie Mae Desktop Originator/Underwriter Release Notes UpdateAccessLendingBelum ada peringkat

- FEDERAL HOUSING FINANCE AGENCY News Release: 10/24/11Dokumen8 halamanFEDERAL HOUSING FINANCE AGENCY News Release: 10/24/11AccessLendingBelum ada peringkat

- Hud FHADokumen12 halamanHud FHAAccessLendingBelum ada peringkat

- Comparison of FHA Expiring and New County LimitsDokumen11 halamanComparison of FHA Expiring and New County LimitsAccessLendingBelum ada peringkat

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- Lat Soal Time Value of MoneyDokumen3 halamanLat Soal Time Value of MoneyHendra G. AngjayaBelum ada peringkat

- Case Digest in NILDokumen33 halamanCase Digest in NILChristopher G. HalninBelum ada peringkat

- Horizontal Vertical AnalysisDokumen4 halamanHorizontal Vertical AnalysisAhmedBelum ada peringkat

- Cis Ets GueyeDokumen3 halamanCis Ets GueyeLaert RuttembergBelum ada peringkat

- Maintaining Automatic Teller Machine (ATM) Services PDFDokumen41 halamanMaintaining Automatic Teller Machine (ATM) Services PDFnigus83% (6)

- CH 07Dokumen104 halamanCH 07della dfapBelum ada peringkat

- FNB Aspire AccountDokumen44 halamanFNB Aspire Accountjessicaheyns5Belum ada peringkat

- Finance Current Affairs March RevisionDokumen47 halamanFinance Current Affairs March RevisionRte FrthBelum ada peringkat

- ch07 SM Carlon 5eDokumen39 halamanch07 SM Carlon 5eKyle100% (1)

- General JournalDokumen2 halamanGeneral JournalJacob SnyderBelum ada peringkat

- RDInstallment Report 01!06!2023Dokumen1 halamanRDInstallment Report 01!06!2023PRADEEP KUMARBelum ada peringkat

- When Are CountryWide Notes Endorsed and Excerpt of Deposition Transcript of SjolanderDokumen18 halamanWhen Are CountryWide Notes Endorsed and Excerpt of Deposition Transcript of Sjolander83jjmack100% (8)

- Unit 4: Credit Creation ProcessDokumen12 halamanUnit 4: Credit Creation ProcessSankalp DubeyBelum ada peringkat

- Fundamentals of Accountancy, Business and Management 2: Senior High SchoolDokumen19 halamanFundamentals of Accountancy, Business and Management 2: Senior High SchoolMarvelous Julia StamariaBelum ada peringkat

- Types of BanksDokumen10 halamanTypes of Bankssaeed BarzaghlyBelum ada peringkat

- HBL Management SystemDokumen6 halamanHBL Management Systemali chahilBelum ada peringkat

- Pu Workers Bank DetailsDokumen2 halamanPu Workers Bank DetailsJagadish JagsBelum ada peringkat

- Financial Services: Ca Final - Financial Reporting Tayal InstituteDokumen11 halamanFinancial Services: Ca Final - Financial Reporting Tayal InstituteJatinkatrodiyaBelum ada peringkat

- SKBDN Dan Curah HujanDokumen4 halamanSKBDN Dan Curah HujanEdy CahyonoBelum ada peringkat

- PART-B Question No 7Dokumen3 halamanPART-B Question No 73acsgrp 3acsgrpBelum ada peringkat

- Sample Answer & Affirmative Defenses Against Fannie MaeDokumen6 halamanSample Answer & Affirmative Defenses Against Fannie MaeChristine HecklerBelum ada peringkat

- Department of Education: Republic of The PhilippinesDokumen8 halamanDepartment of Education: Republic of The PhilippinesJeweljoy PudaBelum ada peringkat

- Ab5431 20220105 Combined Margin StatementDokumen1 halamanAb5431 20220105 Combined Margin Statementthotada durga prasadBelum ada peringkat

- For Payment From July 2005 OnwardsDokumen1 halamanFor Payment From July 2005 Onwardsvijay123*75% (4)

- Resume ImranDokumen2 halamanResume Imranfahadffareed100% (2)

- Reserve Bank of IndiaDokumen84 halamanReserve Bank of IndiaSunil ColacoBelum ada peringkat

- Imsb T6Dokumen5 halamanImsb T6Lyc Chun100% (2)

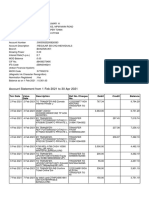

- Account Statement From 1 Feb 2021 To 30 Apr 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDokumen11 halamanAccount Statement From 1 Feb 2021 To 30 Apr 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceUday AbhiBelum ada peringkat

- Class 10-11Dokumen38 halamanClass 10-11Asif HussainBelum ada peringkat

- Chapter 08Dokumen46 halamanChapter 08Ivo_NichtBelum ada peringkat